VIAC Invest 2026 referral code

Use promo code "InvMust" when you register on the VIAC app (valid for new VIAC customers only).

You'll get free management of CHF 2'000 of assets in your investment account, and this is valid for life! (And you will also help to support the blog, thanks!)

Here we are again, talking about VIAC…

VIAC who launched the best 3a pillar in 2017. And the same VIAC who launched (according to my Mustachian criteria) the best mortgage in Switzerland in 2022.

I’ve been a client of the two products since the beginning.

That’s why I always keep a close eye on whatever new product VIAC introduces.

VIAC Invest in a nutshell

In short, here’s my review of VIAC Invest, starting with its strengths:

What I like about VIAC Invest

- The lowest management fees in Switzerland (0.25%, i.e. ~0.46% in total with the product costs for the Global 100% stocks strategy), with stamp duty and currency exchange fees included

- A minimum investment of CHF 1 to get started, ideal for taking your first step into the stock market

- A fee-free cash option for the part not invested in stocks (rare among Swiss robo-advisors)

- A 100% global stocks strategy available, exactly what you need to build your wealth over the long term

What could VIAC Invest improve in the future?

- The tax optimization of US dividends: VIAC uses Swiss funds which lose ~30% to US withholding tax (not recoverable via the DA-1 form), against 15% for the Irish ETFs of their closest competitor finpension Invest (and potentially down to 0% via the DA-1 form, though that last step isn’t validated by the tax authorities yet). This is the point that puts it in 2nd place in my ranking.

- Remove the subscription and redemption fees on its in-house funds (~0.07% when buying, ~0.14% when selling for the 100% stocks strategy)

MP’s recommendation

VIAC Invest is the second best robo-advisor in Switzerland, just behind finpension Invest which wins on net return thanks to its US dividend tax optimization. If you want to maximize your net return, I recommend finpension Invest. And if you want to keep all your accounts in the same place as your VIAC 3a (and your mortgage), VIAC Invest remains an excellent choice you won’t be disappointed with.

Too many readers still don’t invest all their savings

Out of fear of not “doing it right”, or simply “lack of stock market knowledge”, many readers tell me that they still don’t invest their savings in the stock market to make their wealth grow.

So I’ve written an article (link here: The ladder of the stock market investor) to provide support for this not so simple journey.

Up to now, I’ve listed four products in the “robo-advisor” category, which enables you to do everything on autopilot.

Now there’s a newcomer shaking up this category: VIAC Invest.

What is VIAC Invest?

VIAC Invest is the same automated investment platform used by your VIAC 3a pillar, except that in this case, it’s for investing your savings.

As with VIAC 3a, you can choose one of VIAC’s strategies, or build your own investment portfolio yourself.

Here is the key information about VIAC’s investment solution:

- Minimum investment amount: CHF 1

- Ideal for taking the first step

- VIAC Invest management fees:

- 0.25%

- To which you need to add the product costs of between 0.21% and 0.24% (for a Global investment focus, depending on your strategy)

- Which gives us total fees of about 0.46% to 0.49%

- That makes it one of the cheapest robo-advisors in Switzerland fee-wise (almost tied with finpension Invest)

The alternatives to VIAC Invest, and how they compare

Here’s the comparison of the costs of the main Swiss robo-advisors (VIAC Invest, finpension Invest, findependent, True Wealth, Selma and Inyova):

| Provider | Management fees | Other fees (charged separately) | Product costs (TER) | Total costs | Min. investment |

|---|---|---|---|---|---|

| VIAC | 0.25% | Subscription/redemption ~0.07%/0.14% | 0.21-0.24% | 0.46-0.49% | CHF 1 |

| finpension | 0.39% | Stamp duty up to 0.15% | 0.08-0.10% | 0.47-0.49% | CHF 1 |

| findependent | 0.40% | Stamp duty up to 0.15% + forex 0.50% | 0.17-0.20% | ~0.57-0.60% | CHF 500 |

| True Wealth | 0.50% | Stamp duty up to 0.15% + forex 0.10% | 0.12-0.21% | ~0.62-0.71% | CHF 8'500 |

| Selma | 0.68% | Stamp duty up to 0.15% + forex 0.25% | ~0.22% | ~0.90% | CHF 2'000 |

| Inyova | 1.20% | Stamp duty up to 0.15% | Included | ~1.20% | CHF 2'000 |

Total costs = management fees + product costs (TER); the “other fees” are one-off costs (when buying or exchanging currencies). For VIAC and finpension: Global strategy with ~100% stocks, as of June 2026.

Management fees decrease with your invested wealth: findependent down to 0.29% (from CHF 1 million), True Wealth 0.25% (above CHF 500'000), Selma down to 0.42% (from CHF 500'000), Inyova from 0.60%. Inyova invests in individual securities directly (TER included in its fee), with an ongoing migration to an in-house ETF (TER of 0.95%, launched in December 2025) worth keeping an eye on.

But watch out: the lowest fees don’t mean the best net return (see the detailed explanation further down).

What type of Mustachian is VIAC Invest aimed at?

As a Mustachian, I expect that you’ve built up enough stock market knowledge in order to invest by yourself and save hundreds, even thousands of CHF in fees, by only paying 0.1-0.2% on the money you have invested.

But to get to that stage, you first need to take the plunge.

That’s where the super easy-to-use robo-advisor of VIAC Invest comes in.

Because as much as it’s better to pay the lowest fees (doing it by yourself with your own online broker), it’s 100x worse to do nothing and let your savings get eaten away by inflation in an old bank account with one of our big fat Swiss banks (oh no, shame, now there’s only one left haha!)

Conclusion

A big thank you to the VIAC team for this product. Our values and mindset are perfectly aligned. Their robo-advisor was excellent from day one, and remains a very solid second option today, just behind finpension Invest (which takes the lead thanks to the tax optimization of US dividends). And they keep innovating day after day. Bravo to them!

The VIAC promo code below entitles you to free management of CHF 2'000 in assets on your VIAC investment account (valid for new VIAC customers only), and it's valid for life!

===> InvMust <===

VIAC Invest FAQ

Which strategies are available on VIAC Invest?

As with VIAC 3a, there are 3 investment focus areas: Global, Switzerland, and Sustainable.

And for each of these focus areas, you have the following strategies:

- 20% equities, the rest in bonds

- 40% equities, the rest in bonds

- 60% equities, the rest in bonds

- 80% equities, the rest in bonds

- 100% equities (what I would choose myself, if I was investing today with VIAC Invest, with the “Global” focus)

Also, for the bond portion, you can decide to leave it in cash only if you wish. This cash portion currently no longer earns any interest (0.00% as of June 2026, down from 0.60% at launch). On the other hand, there are no fees to pay on it, as fees are only payable on assets invested in securities.

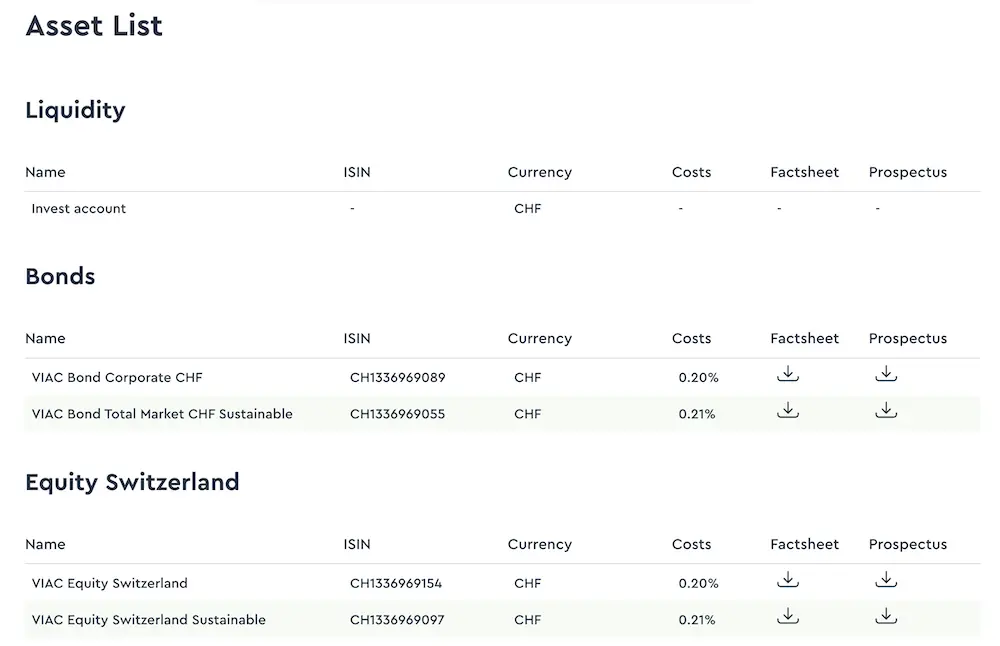

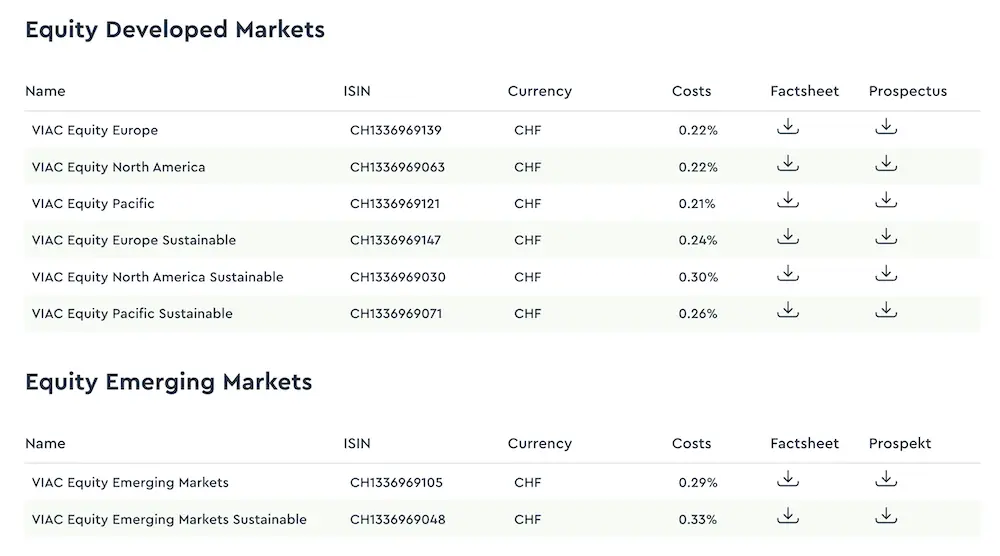

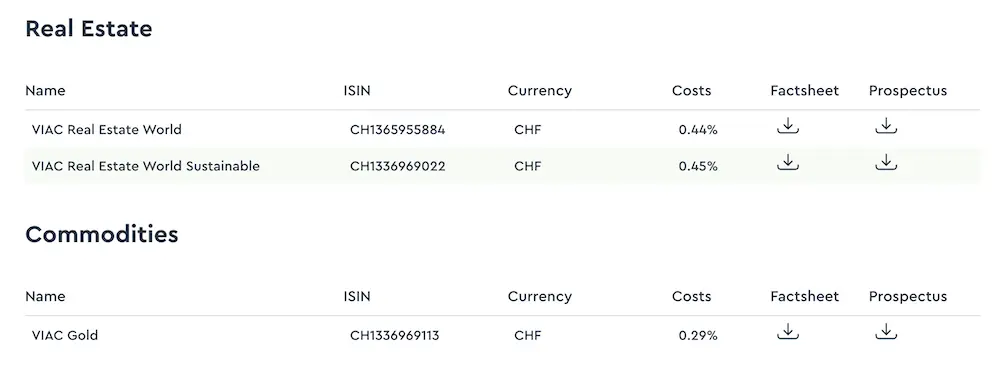

Which assets are available for a personalized investment strategy?

Here is the list of assets available in VIAC Invest:

How many VIAC Invest portfolios can I open?

You can open up to 10 stock market portfolios with VIAC Invest.

How do I withdraw money from VIAC Invest?

You can withdraw your money from VIAC to your usual bank account.

And VIAC also offers a way of setting up a standing order to withdraw your money through regular transactions. So you can imagine placing your vested benefits assets there, which is advantageous compared to income from a pension fund, as your assets with VIAC Invest would be transferred to your beneficiaries in the event of death.

Is VIAC Invest tax optimized?

This is VIAC Invest’s weak point against finpension Invest.

VIAC uses Swiss funds for US stocks. As a result, US dividends suffer a withholding tax of close to 30% (part of the fund is domiciled in Ireland, which softens the blow a little), and crucially, you can’t claim it back via the DA-1 form.

finpension, on the other hand, uses Irish ETFs: the withholding drops to 15% (automatically), and may even be recoverable via the DA-1 form to get down to 0%. On a global stocks portfolio, that represents up to ~0.30% of extra net return per year, though this DA-1 reclaim on finpension’s reporting isn’t validated by the cantonal tax authorities yet (a court case is pending; finpension is confident but can’t guarantee it).

So yes, despite its unbeatable fees, VIAC is not the robo-advisor with the best net return: what counts is the after-tax performance, and that’s where finpension Invest takes the lead.

To be fair to VIAC: the gross performance of their funds has historically stayed very close to that of the Irish ETFs, and they could optimize this point in the future.

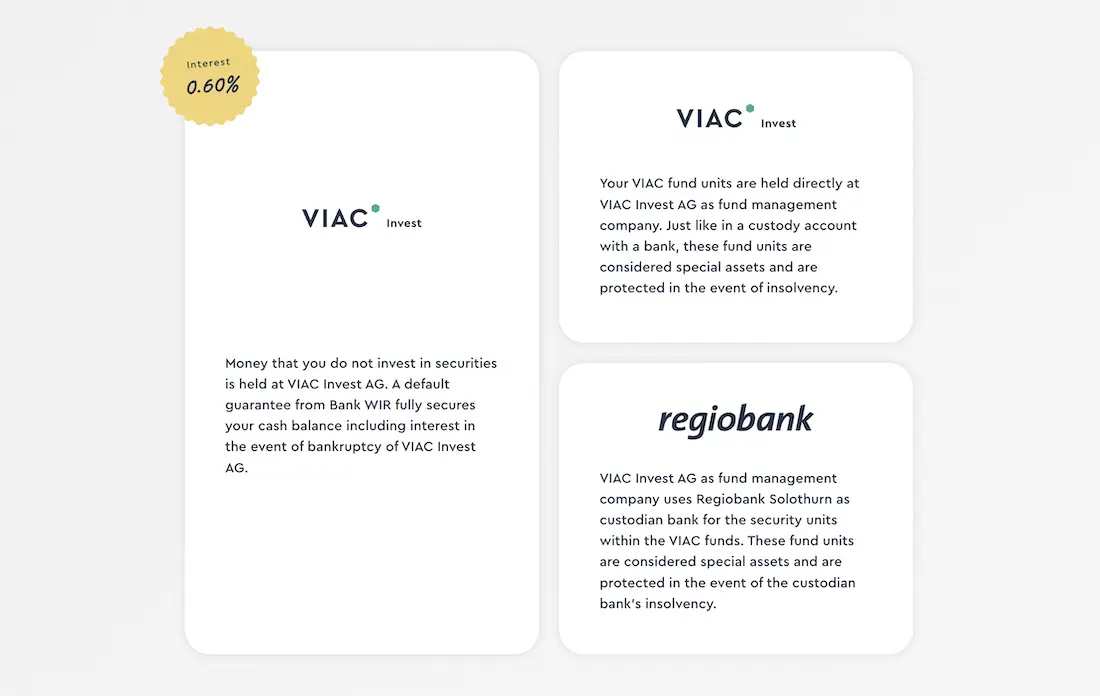

Where is the money held that I invest with VIAC Invest?

To set it out clearly, VIAC has created the company VIAC Invest AG.

When you put money (your hard-earned CHF) into VIAC Invest AG, this money is fully covered (including interest) by Bank WIR in the event that VIAC Invest AG goes bankrupt.

Then, when you buy securities in the stock market via VIAC Invest, it’s still VIAC Invest AG that acts as the fund management company. Your money placed in this fund is considered as a special asset, and is protected in the event of VIAC Invest AG becoming insolvent.

Lastly, the money is held in the fund virtually. In reality, it’s Regiobank Solothurn which acts as the custodian bank for the security units in VIAC funds. Likewise, these units are like a separate asset and are protected in the event that the custodian bank becomes insolvent.

VIAC Invest or finpension Invest?

VIAC Invest and finpension Invest have nearly identical fees (Global 100: ~0.46% at VIAC, ~0.47% at finpension as of June 2026). The real difference comes down to taxes: finpension uses Irish ETFs which optimize the US withholding tax (up to ~0.30% of performance per year via the DA-1 form, though that reclaim isn’t validated by the cantonal tax authorities yet), while VIAC uses Swiss funds, less optimized on this point. So I rank finpension Invest slightly ahead in 2026, even though VIAC keeps the fee-free cash option and avoids the stamp duty through its in-house funds (which carry higher spread costs instead, so the net result is comparable). You can find my detailed review of finpension Invest here.

VIAC Invest or neon Invest?

Such a comparison isn’t valid, because neon Invest is not a robo-advisor, it’s a trading platform. With neon Invest, you buy your ETFs and stocks yourself, without automated management like VIAC Invest.

neon does have a similar option called “portfolio templates”, but as they explain themselves: there’s no regulatory risk profiling feature, no automatic rebalancing, nor any other automated management. It’s a “ready-made ETF list” you can use, but that you then have to manage yourself.

So rather than this comparison, the real question is another one: where do you stand on the ladder of the stock market investor?

If you want a 100% autopilot investment solution, then finpension Invest is the best option available in Switzerland today. And if you feel ready to manage your investments yourself, then you’ll find cheaper online trading platforms than neon Invest (see my article: Best broker in Switzerland (comparison 2026)).

VIAC Invest or willBe Invest?

willBe Invest has total fees of 0.79%, compared with ~0.46-0.49% for VIAC Invest or finpension Invest.

Also, willBe favors a “sustainability” portfolio, which on the one hand is never totally aligned with one’s own values, and which above all doesn’t have that much impact (apart from on the investor’s conscience).