As you have understood so far, by taking on a foreign broker and investing from Switzerland, you benefit from a great deal of preferential treatment fiscally speaking.

But you still pay taxes in Switzerland, despite what all the countries around us believe ;)

And in particular taxes on dividends received [1].

As a reminder, a dividend is cash that you, as a Swiss investor, receive from the company you own as a thank you for lending them capital (i.e. the money you have invested in them).

Each company decides on its dividend payment schedule (annually, quarterly, etc.).

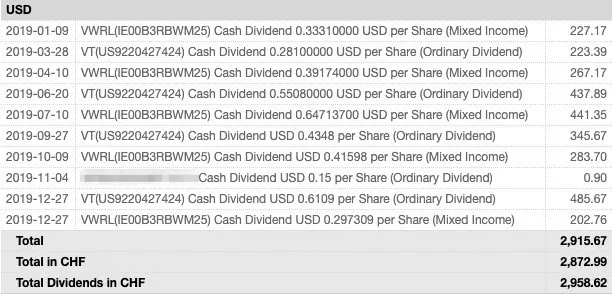

And concretely, when I say “cash you receive”, I mean literally CHF that you see paid into your brokerage account.

With pictures, it is often more explicit:

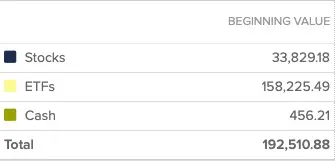

In any brokerage account, you have a line for cash (where your dividends are paid), and one or more lines with the securities you own (here 'Shares' and 'ETF')

The principle is simple: any dividend you receive must be declared gross (without deducting withholding taxes — this is the subject of our next chapter), and is taxed as income.

Let’s take an example: imagine you own 150 Roche shares that pay you CHF 2.5 in dividends. That gives you 150 x 2.5 = CHF 375, so you declare this CHF 375 as income.

The same applies to foreign shares from the US, Japan, Ireland or any other country.

Any dividend received must be declared in Switzerland.

You must declare all dividends received when you fill out your tax return. This process is also detailed in my various Swiss guides on how to fill out your tax return correctly:

- Tutorial ZHprivateTax Tax Return (Part 3)

- Tutorial TaxMe-Online Bern Tax Return (Part 2)

- Tutorial eTAX AARGAU Tax Return (Part 3)

- Tutorial GeTax Tax Return (Part 2)

- Tutorial VSTax Tax Return (Part 2)

- Tutorial FriTax Tax Return (Part 2)

- Tutorial VaudTax Tax Return (Part 2)

- Tutorial E-Tax SG St. Gallen Tax Return (Part 1)

- Tutorial eSteuern.LU Tax Return (Part 2)

- Tutorial eTax Solothurn Tax Return (Part 2)

- Tutorial eTax.SZ Tax Return (Part 2)

- Tutorial eFisc Thurgau Tax Return (Part 3)

- Tutorial eTax.zug Tax Return (Part 2)

There is, however, a subtlety to understand between cumulative dividends and distributive dividends. This is discussed below.

[1] Focusing your portfolio on dividend-paying stocks is generally irrelevant, it becomes even less relevant when you understand that Switzerland is more advantageous with capital gains than with dividends.

Accumulative or distributive dividends, which is the best regarding taxes?

“Uh, Marc, we said no jargon!”

Ah yes, it’s true, I always forget, sorry!

Simply put, when an ETF pays you dividends, it can do it in two different ways:

- They distribute them to you, i.e. they literally pay you cash on your investment account (see the first screenshot of this page). This ETF is therefore said to be “distributive” (often shortened to “dist”)

- The other option is that the ETF automatically reinvests the dividends in itself. This ETF is said to be “accumulative” (often shortened to “acc”)

How to check if an ETF is accumulative or distributive

I’m often asked the following question: “How do I know if an ETF is accumulative or distributive?”

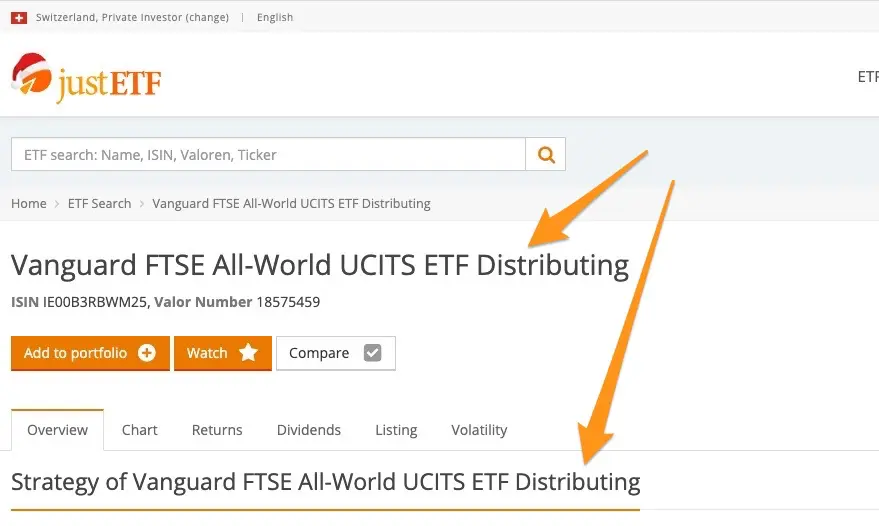

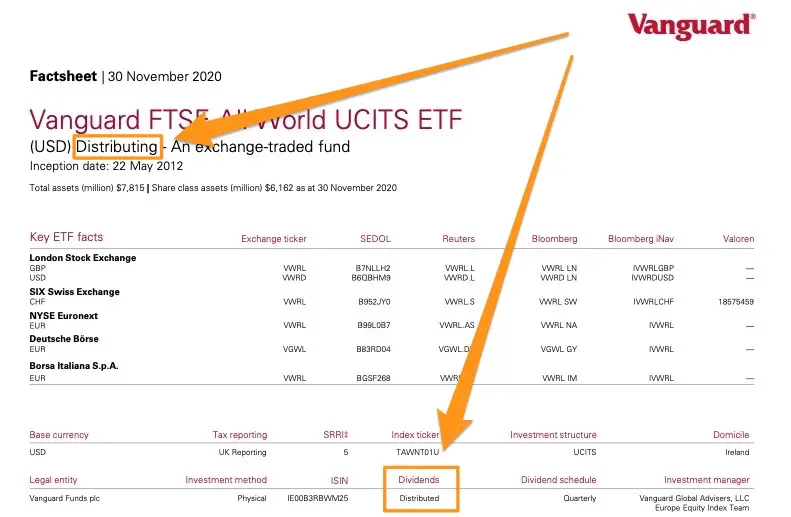

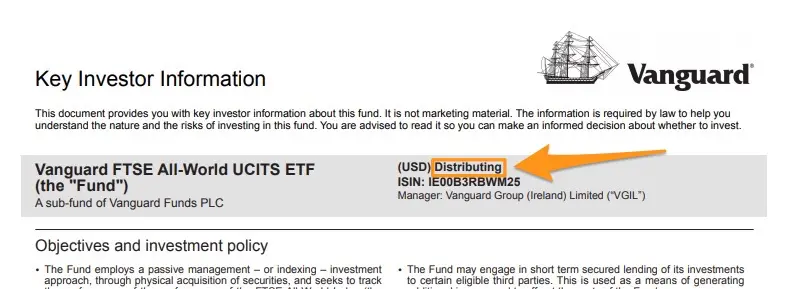

The answer is simply indicated in the name of the ETF directly (see screenshot justetf.com below), or in the ETF factsheet (see below), or in the Key Investor Information Sheet (aka KIID, see below):

The word 'Distributing' on the JustETF.com's ETFs search engine indicates that this VWRL ETF is distributive

This information can also be found in the ETF factsheet provided by the issuer of the ETF, here Vanguard for its distributive VWRL ETF

Finally, you can also tell whether an ETF is accumulative or distributive by looking at the Key Investor Information Sheet (aka KIID)

Practical differences: which dividend type is easier to handle?

From a purely practical point of view, an accumulative ETF is more convenient (for the lazy ones that we are ;)) because it avoids you having to manually reinvest yourself by buying ETF shares thanks to the dividends received in cash on your brokerage account.

On the other hand, when you are FIRE (Financial Independence, Retire Early), a distributive ETF can be more practical because it allows you to finance your lifestyle without always having to bother reselling a few ETFs — i.e. you simply transfer the cash received to your Swiss bank account and that’s it.

Returns comparison: does dividend type really matter?

Then, from a pure yield point of view, there is no difference. So if I have the choice between two ETFs, one accumulative and one distributive, then I follow my ETF selection process described in this article (in short, the cheapest in fees and the most liquid in transaction volume and fund size).

The most tax-efficient ETF for Swiss investors

But let’s get back to the subject of taxation, since that’s what we’re interested in in this guide.

When I started investing, I had read and believed (wrongly!) on forums that accumulative ETFs were better than distributive ETFs in Switzerland because the former (accumulative, therefore) were not taxed. In fact, the legend was going around that since the dividends were not paid out, the Swiss tax authorities didn’t see anything, and that I was saving taxes.

It was a good idea for me to talk about it on the blog, because some readers quickly informed me that I was wrong! (I love the blog for that, I’m learning a lot)

So, in terms of taxation, the real answer to the question “Accumulative or distributive ETF?” is that it has no impact on taxes. Because you have to declare both.

But the devil is in the details. Because there is an important point to know which makes, in the end, distributive ETFs more favorable for a Swiss investor in certain cases.

I would like to thank here @nugget, a veteran of the MP Forum, for his excellent research on tax optimization. Especially with this post wiki in the forum.

Because I’m not a tax or numbers genius, far from it. And without the exchanges in our Swiss FIRE community, I would know 1'000 times less than everything I have learned so far. So let us give back to Caesar what belongs to Caesar as the saying goes.

As mentioned in the forum, this article from the NZZ, via a mention of the Zurich-based financial consulting firm Hinder Asset Management, states the following:

ETFs that accumulate sometimes do not show income and capital gains separately, which can result in capital gains being taxed. The taxable income of ETFs can be found on the website of the Federal Tax Administration.

In plain language, when you file your tax return and you want to know how much dividend you have to declare, you can either go and see what you have received on your online broker’s interface, or, more cautious because officially validated by the FTA, you can go and see on the ICTax website of the FTA (for “Income and Capital Taxes”).

Two cases are possible:

- You have a distributive ETF

- This ETF is listed on ICTax, so you have peace of mind and will only pay tax on the dividends received (and not on capital gains)

- This ETF is not listed on ICTax, so you have to find your dividend info via your online broker. And the tax authorities may ask you for a proof of this (this has never happened to me personally). It's really easy to find this information, so it's not a problem

- You have an accumulative ETF

- This ETF is listed on ICTax, so you have peace of mind and will only pay tax on the dividends received (and not on capital gains)

- This ETF is not listed on ICTax, so this is more problematic, because in general, **Swiss tax authorities tax you on dividends AND capital gains** (open question on my side and needing proof: does IB not provide this level of detail that allows you to avoid taxation on your capital gain?)

It is this last point that makes the Swiss investment community say that it is therefore more interesting to opt for a distributive ETF from a tax point of view.

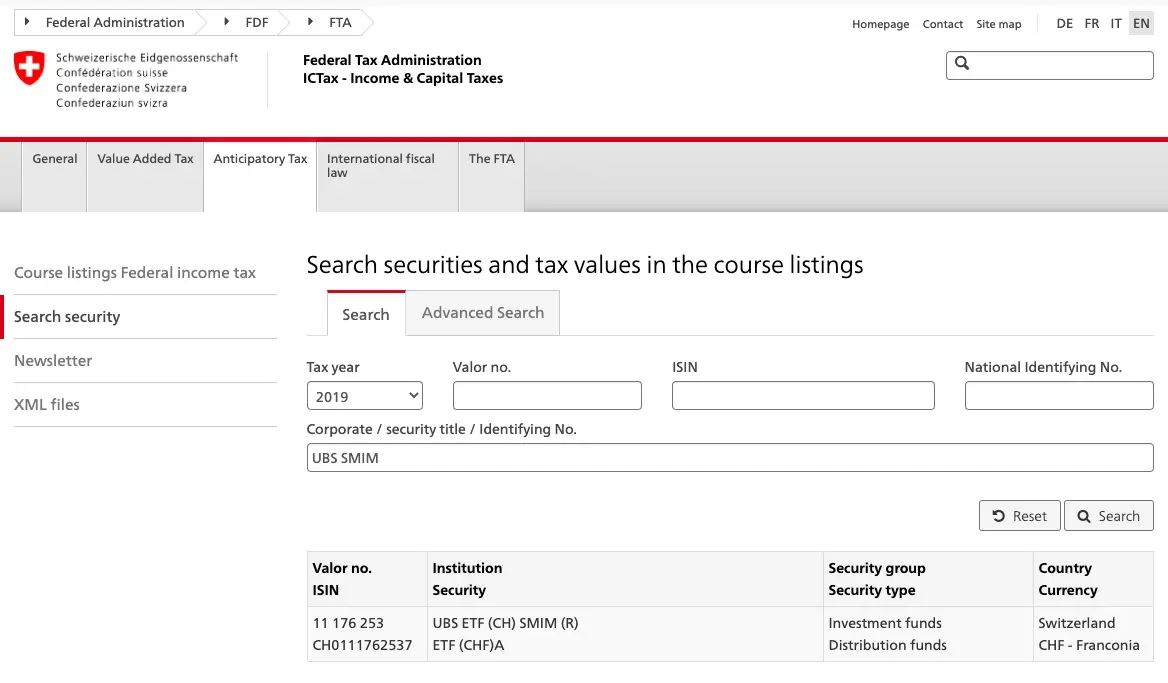

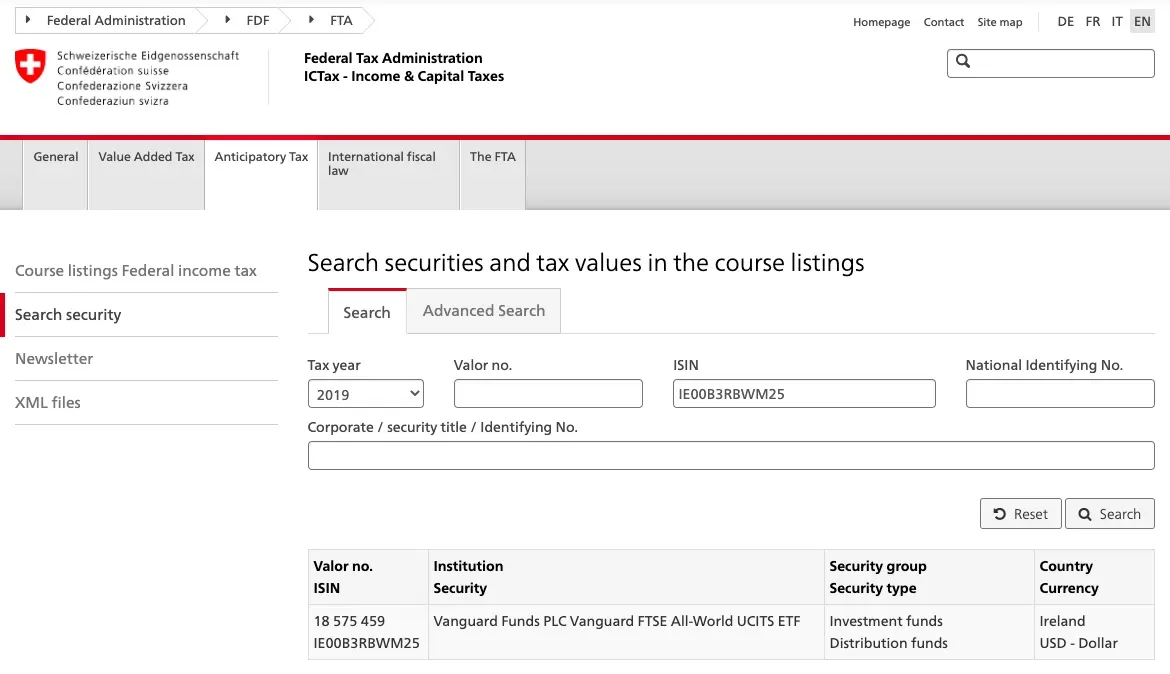

So that you can see what I’m talking about when I mention the ICTax website, here’s how it allows you to find the amount of dividends you have to declare with examples:

UBS SMIM ETF

The Swiss ETF UBS SMIM that I like is on the one hand distributive, and on the other hand listed on ICTax, so we are safe for taxes:

The Swiss ETF UBS SMIM that I like is on the one hand distributive, and on the other hand listed on ICTax, so we are safe for taxes

VWRL ETF (which I recommend to buy if you use DEGIRO)

The Irish ETF VWRL is on the one hand distributive, and on the other hand listed on ICTax, so we are also safe for taxes:

The Irish ETF VWRL is on the one hand distributive, and on the other hand listed on ICTax, so we are also safe for taxes

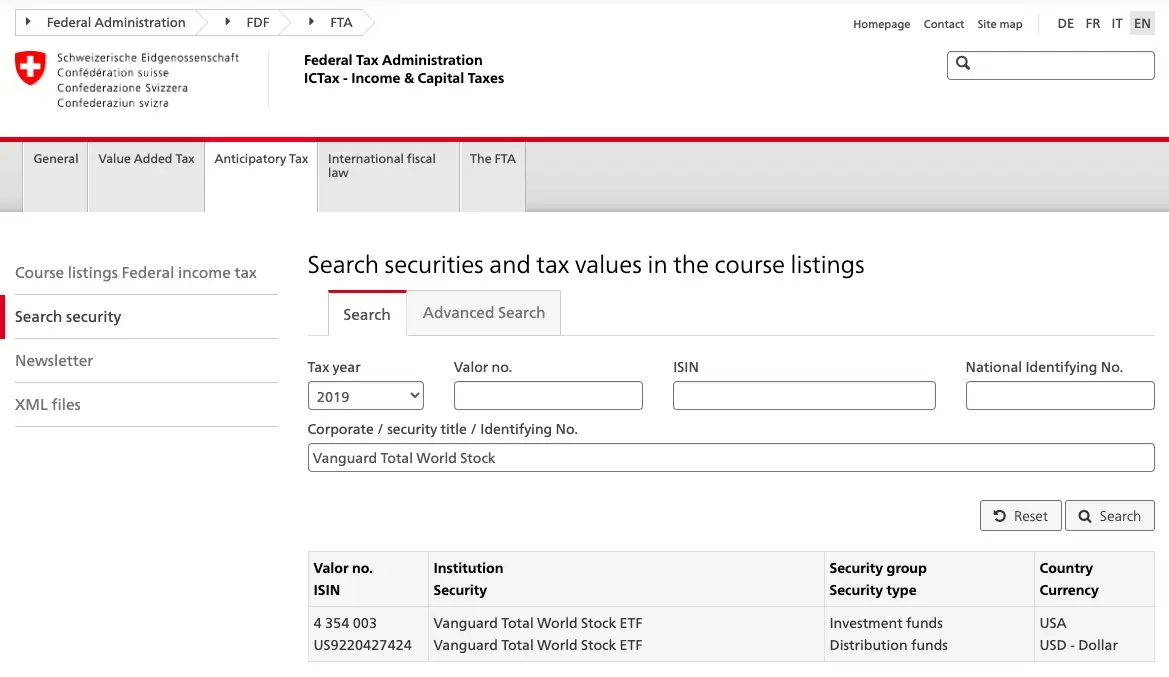

VT ETF (my favorite, which I buy regularly through Interactive Brokers)

My favorite VT ETF (because of its simplicity) is distributive AND listed on ICTax, so everything is fine:

My favorite VT ETF (because of its simplicity) is distributive AND listed on ICTax, so everything is fine :)

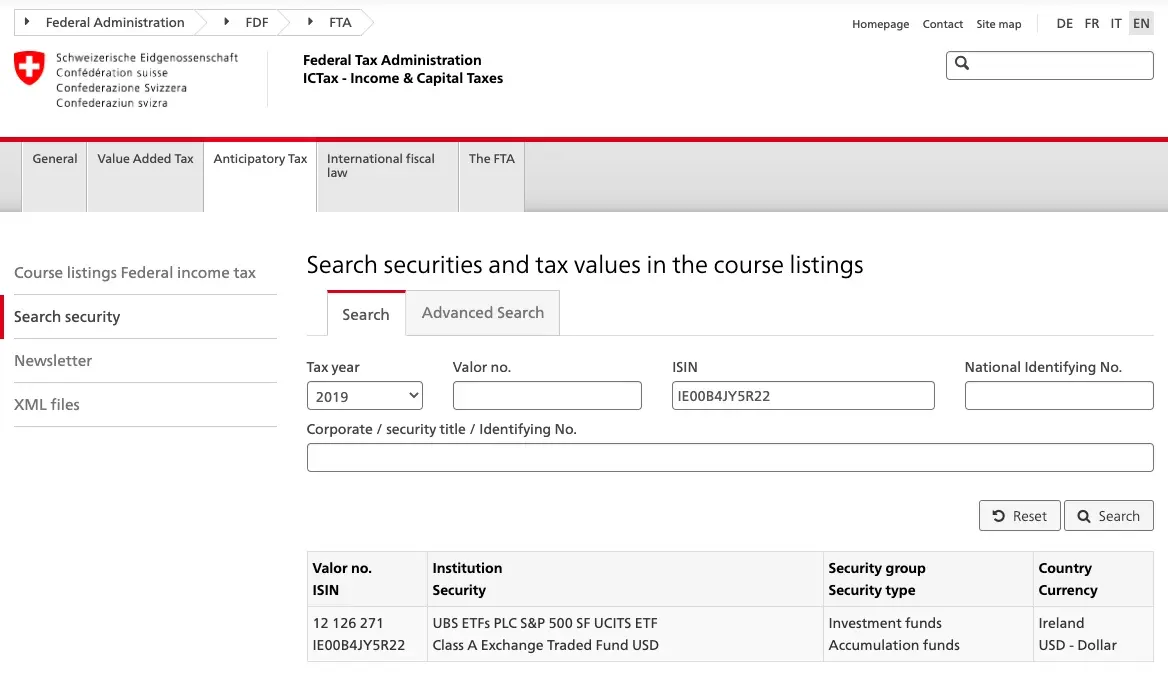

UBS S&P500 ETF (which I never bought, just for the example)

The UBS S&P500 ETF is accumulative. So be careful! But, as it is listed on ICTax, you don’t have to worry about your taxes, you won’t be taxed on any capital gain:

The UBS S&P500 ETF is accumulative. So be careful! But, as it is listed on ICTax, you don't have to worry about your taxes, you won't be taxed on any capital gain

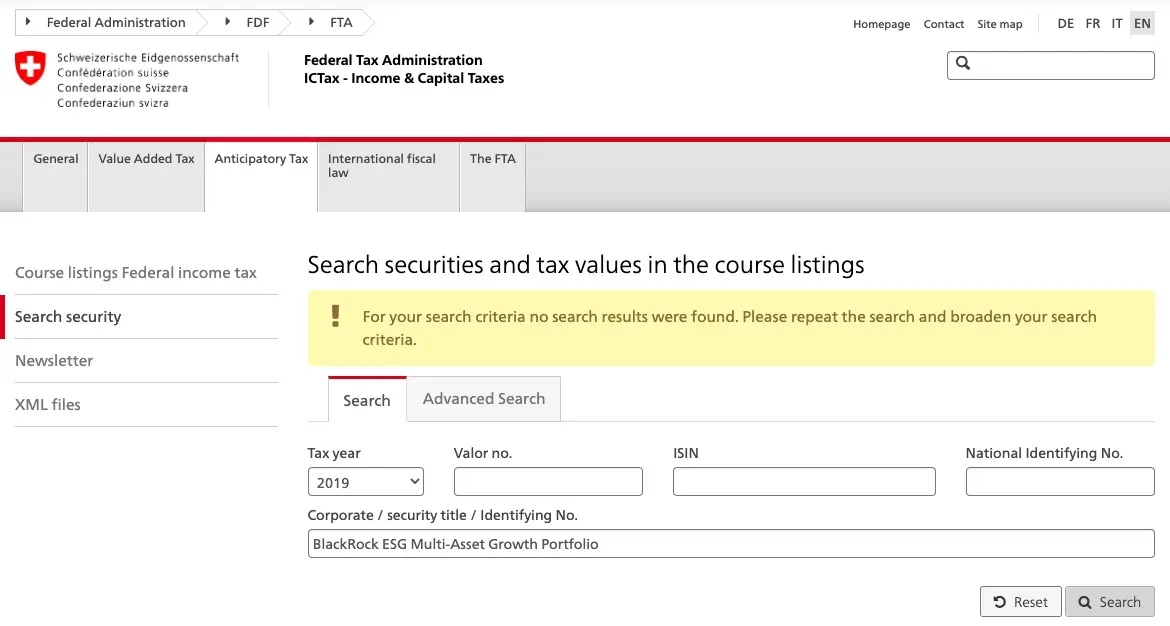

BlackRock ESG Multi-Asset Growth Portfolio ETF (which I never bought, it’s just for the example)

This Blackrock ETF is accumulative AND is not listed on ICTax. It is therefore not optimal in terms of Swiss taxation because you have a good chance of being taxed on the capital gain in addition to dividends by the Swiss tax authorities:

Cet ETF de Blackrock est accumulatif ET n'est pas listé sur ICTax. Il n'est donc pas optimal en terme d'imposition suisse car tu as de fortes chances de te faire imposer sur le gain en capital en plus de dividendes par le fisc suisse

Small note on ICTax and the reactivity of the Swiss tax authorities

We are fortunate to have an administration that holds up well in Switzerland. Yes we are, I assure you. Sometimes we moan against them, but when I listen to the expats talking to me about their administration, I can tell you that we are really well served.

In short, all this to say that if you have an ETF or any other title that is not listed on ICTax, then you can ask them to add it. And they do! And from what I’ve read on the different sites and forums, they do it quickly (like not tens of months of waiting).

Summary: accumulative or distributive ETFs for a Swiss investor

I hope that all these examples will have driven home the point, and that you have now understood which is the best choice fiscally speaking between an accumulative and a distributive ETF.

To sum up, favor a distributive ETF because it’s easier to declare to the tax authorities, you’ll lose less money in taxes no matter what happens than an accumulative ETF, and it will be more useful when you’re FIRE (because you’ll be able to use the cash you receive directly to finance your lifestyle, instead of having to resell securities).

As you can see, so far it is actually quite easy to understand how taxes work for a Swiss investor.

Where it gets more complicated is when you get into the subject of withholding taxes. Again, the recipe is complex, but not complicated once you know what to do. This is what we will see together in the next chapter.