Olivier, a reader from Geneva, wrote to me recently:

I have a pillar 3b with Helvetia, tied to a life insurance policy (CHF 250'000).

The problem is that fees are pretty high: out of the CHF 4'800 I pay every year, about CHF 1'300 go to management fees / insurance premium.

Which leaves a fairly small share actually invested…

And this question keeps coming back to me. Olivier, Diego, Emma, Alix: they all ask me the same thing in different words. “3b or no 3b?”

Even though I don’t live in Geneva or Fribourg, and pillar 3b doesn’t concern me (not tax-deductible in my canton), I couldn’t leave the 3b-tied-to-life-insurance scam unanswered any longer!

So I broke down the topic in full detail. Feel free to forward this article to your insurance advisor who keeps pushing you to sign ;)

Pillar 3b or not? The short answer

No, it’s NEVER worth opening a pillar 3b, which is always tied to life insurance.

Here’s why:

- Pillar 3b is only tax-deductible in Geneva and Fribourg (other cantons have a “theoretical deduction” shared with health insurance premiums, but the cap is already maxed out by those very premiums)

- Across every offer on the market, pillar 3b is tied to life insurance, where your contributions pay for the broker’s Porsche rather than growing your wealth

- The only 3b products available offer lower returns (1 to 2%), compared to pillar 3a with finpension or VIAC. And the fees on 3b products are sky-high

- The “tax deduction” you gain is far smaller than what you’d earn investing the same money in the stock market

What exactly is pillar 3b?

Pillar 3b is made up of your personal savings: cash on hand, savings accounts, life insurance contracts, and other investments.

Yes, you read that right: whether it’s your Interactive Brokers account or the best savings account, both fall within the legal definition of pillar 3b.

This is what the Swiss Confederation calls unrestricted private pension provision. In plain English, it’s all the money you set aside to complement pillar 1 and pillar 2 when you retire.

Difference between pillar 3a and pillar 3b

Pillar 3a, also called restricted private pension, can’t be touched before retirement, except under specific conditions (for example: buying your primary residence). That’s why we say 3a is restricted: it’s locked until your retirement (official at 65, not your early retirement when you hit FI!)

On the flip side, you can do whatever you want, whenever you want, with your pillar 3b. Including pulling it out to fund a 6-month sabbatical. Good thing, since it’s literally your private savings! That’s why we say pillar 3b is unrestricted: it’s not tied to the Swiss retirement system once you turn 65.

| Pillar 3a | Pillar 3b | |

|---|---|---|

| Tax deduction | Everywhere in Switzerland | Cantons of Geneva and Fribourg only |

| Annual cap | CHF 7'258 (employee) | No contribution cap |

| Withdrawal | Locked until retirement | Free whenever you want |

| Vehicle | Bank, stock-market investment (VIAC, finpension), or life insurance | Life insurance only (to qualify for the tax deduction) |

Notice something in this table: on the 3a side, you have choice of vehicle (bank, insurance, fintech). On the 3b side, you’re supposed to have the same choice. Yet in practice, you’ll always be offered a life insurance policy.

Why? Because the term “pillar 3b” is a semantic scam.

How insurers hijacked the term “pillar 3b”

It’s wild, but this “pillar 3b” nomenclature seems to have been created solely to complicate the Swiss three-pillar retirement system, and, ultimately, line the pockets of people who peddle dubious marketing products, pushing life insurance onto people who just want to grow their savings…

Let me explain: pillar 3b itself is not tax-deductible.

On the Federal Social Insurance Office (FSIO) website, it says: “There are no tax deductions [for pillar 3b].”

Same on the Confederation’s official portal ch.ch: “Pillar 3b generally offers no annual tax benefits.”

Except that some cantons, Geneva and Fribourg to name them, do allow tax deductions for life insurance policies.

And life insurance is something you freely choose to take or not. So it fits the definition of pillar 3b.

And here’s where the confusion kicks in: people conflate pillar 3b (savings, stock-market investments, cash in your wallet) with “a life insurance that by default sits under the pillar 3b category”. Well, I say “people”, but I should really say “insurers do everything to make people conflate […], to rip them off better!”

Because, and this is the whole problem, the tax deduction that Geneva and Fribourg grant for pillar 3b only applies to life insurance products.

Olivier's reaction to his insurer's pillar 3b brochure: 27% of his contributions go to fees before a single franc is even invested!

In the canton of Geneva:

Art. 31 let. d LIPP (rsGE D 3 08): there’s never any mention of “pillar 3b” directly, only “life insurance premiums”.

Same for pillar 3b in Fribourg:

Art. 34, para. 1, letter g LICD: it mentions “payments, contributions and life insurance premiums”, but never talks about pillar 3b as such.

In which cantons is pillar 3b tax-deductible?

The theory: EVERY canton “allows” the 3b deduction in Switzerland

If you stick to the letter of the law, every canton allows you to deduct 3b life insurance premiums. For instance:

- Zurich (§ 31 Abs. 1 lit. g StG ZH): you can deduct “payments, premiums and contributions for life insurance”

- Vaud (Art. 37, para. 1, letter g LI): you can deduct “insurance premiums and contributions”

- And it’s the same story in every other canton

So on paper, you might think: “Great, I can deduct my pillar 3b in every Swiss canton!”

The reality: a tax basket already maxed out by LAMal

Except that, everywhere apart from Geneva and Fribourg, life insurance premiums share the same deduction cap with other insurance types: LAMal (mandatory health insurance), accident insurance, etc.

And since LAMal premiums have exploded over the last twenty years, much faster than those caps, this shared basket is today fully taken up by LAMal alone in most cantons.

Let’s look at this with two concrete examples.

Pillar 3b deduction example in canton Zurich

Let’s start with canton Zurich:

| Amount (CHF/year) | |

|---|---|

| Deduction cap, § 31 Abs. 1 lit. g StG (single, with pillar 2) | 2'900 |

| Average 2026 LAMal premium (all ages, canton Zurich) | - 4'620 |

| Theoretical room left to deduct a 3b life insurance premium | - 1'720 |

In Zurich, the average LAMal premium on its own exceeds the deduction cap. Not only is there zero room to deduct a 3b premium, but CHF 1'720 of LAMal premiums themselves remain non-deductible for this taxpayer.

Pillar 3b deduction example in canton Vaud

| Amount (CHF/year) | |

|---|---|

| Deduction cap, art. 37 para. 1 let. g LI (single, with pillar 2) | 5'000 |

| Average 2026 LAMal premium (all ages, canton Vaud) | - 4'365 |

| Theoretical room left to deduct a 3b life insurance premium | + 635 |

Heads up: these CHF 635 are only a theoretical margin, for an “average” taxpayer profile. But it takes very little: a low deductible (CHF 300 instead of CHF 2'500, your premium jumps significantly) or a supplementary LCA insurance (alternative medicine, dental, etc.), and the basket hits the cap. You can no longer deduct a single franc for pillar 3b.

In practice, the vast majority of Vaud taxpayers can’t deduct anything for their pillar 3b.

And what about pillar 3b deduction elsewhere in Switzerland?

Zurich is actually the general case: everywhere in Switzerland, LAMal reaches (or exceeds) the deduction-basket cap before a single franc of 3b life insurance can squeeze in.

Only Geneva and Fribourg provide a dedicated deduction for life insurance premiums, separate from the LAMal cap:

- Geneva (art. 31 let. d LIPP): explicit deduction of “life insurance premiums”

- Fribourg (art. 34 para. 1 let. g LICD): explicit deduction of “payments, contributions and life insurance premiums”

In other words: if you don’t live in one of these two cantons, the “pillar 3b tax deduction” is a mirage sold to you to get you to sign an overpriced life insurance policy.

To be fair to insurers in those other cantons: none of them push these products. They all know that outside of Geneva and Fribourg, the tax deduction doesn’t exist.

But as we’ll see next, even with those deductions, a product as bad as savings tied to life insurance is useless for growing your wealth…

The opportunity cost of pillar 3b, in numbers

Let’s get back to Olivier’s case from the opening. He pays CHF 4'800/year into his Helvetia pillar 3b, of which CHF 1'300 goes straight to fees (27% upfront!). That leaves him with CHF 3'500 actually invested every year.

Let’s project this over 30 years, and compare two scenarios.

Scenario 1: Olivier keeps his Helvetia pillar 3b

- Payment: CHF 4'800/year

- Fees taken: CHF 1'300/year (“management” + life insurance premium)

- Actually invested: CHF 3'500/year

- Average net return of CHF-denominated life insurance: ~1.5%/year (typical performance of “guaranteed” funds with protected capital)

- Final capital after 30 years: ~CHF 131'000

On top of that, you add the annual tax savings. Olivier is single and has a pillar 2 in Geneva, so he can deduct up to ~CHF 2'232/year in life insurance premiums. At a marginal tax rate of 28%, that amounts to about CHF 625/year in tax savings.

If he reinvests those CHF 625 every year into a world ETF at 7%: ~CHF 59'000 extra after 30 years.

Scenario 1 total: ~CHF 190'000

Scenario 2: Olivier cancels his 3b and splits the CHF 4'800/year between Interactive Brokers and a pure term life insurance policy

- Total payment: CHF 4'800/year

- Separate pure term life insurance (equivalent to the death coverage of the 3b): CHF 350/year

- IBKR trading fees: ~CHF 24/year

- TER fees of the VT ETF: ~0.06%/year (negligible)

- Actually invested on IBKR: ~CHF 4'425/year

- Average gross return of a world-equity ETF: ~7%/year

- No tax deduction (IBKR falls under the “pillar 3b” category, but is not deductible)

- Final capital after 30 years: ~CHF 418'000

Scenario 2 total: ~CHF 418'000

The verdict: ~CHF 228'000 left on the table

| Scenario 1: 3b Helvetia | Scenario 2: IBKR with world ETF | |

|---|---|---|

| Annual payment | CHF 4'800 | CHF 4'800 |

| Product fees | CHF 1'300/year (27%) | ~0.06%/year (VT ETF TER) + CHF 24/year in trading fees |

| Pure term life insurance | Included (implicit death benefit) | CHF 350/year |

| Net annual return | ~1.5% | ~7% |

| Tax deduction | ~CHF 625/year saved | CHF 0 |

| Capital after 30 years | ~CHF 190'000 | ~CHF 418'000 |

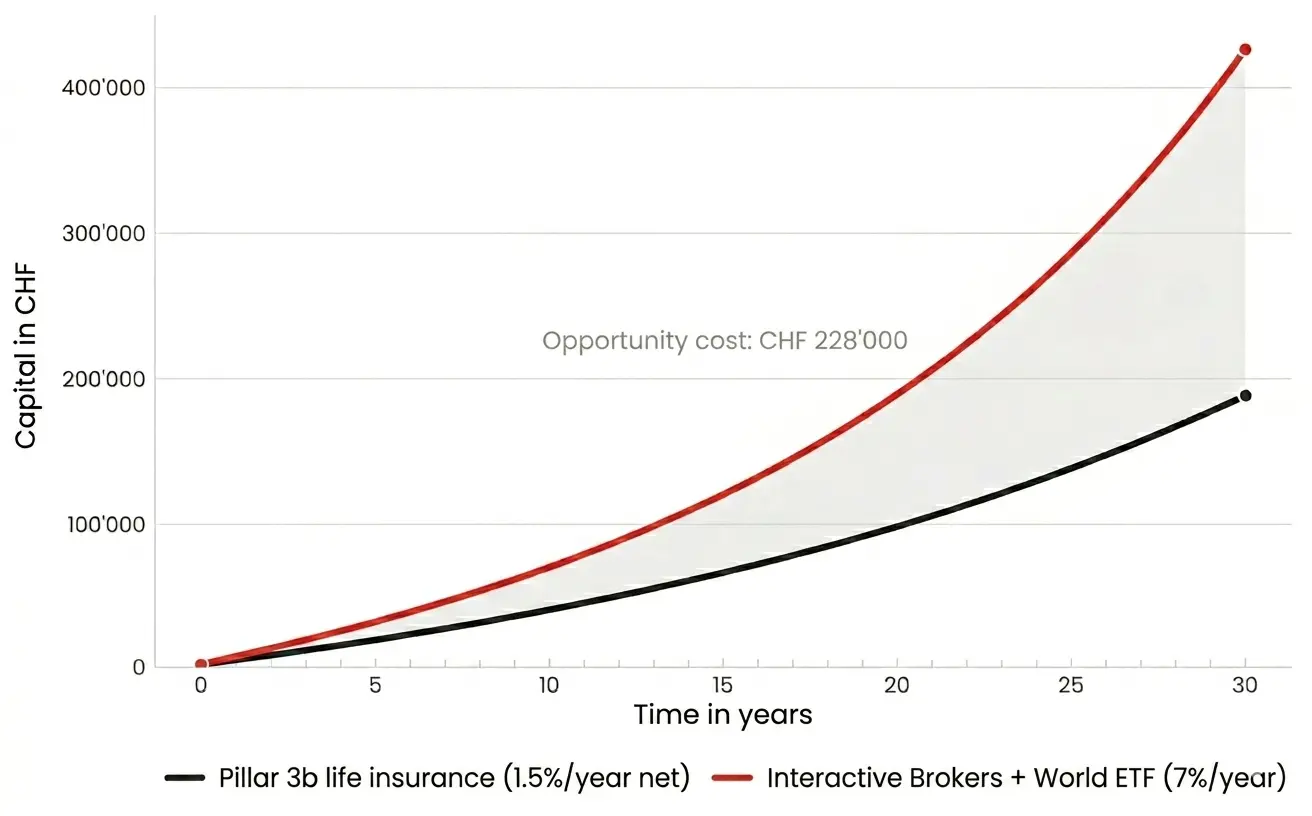

And here’s what that looks like visually:

Opportunity cost over 30 years: sticking with a pillar 3b tied to a life insurance (~CHF 190'000 final) vs investing the same contribution at Interactive Brokers into a world ETF (~CHF 418'000). The grey area represents the CHF 228'000 left on the table.

Pillar 3b costs Olivier ~CHF 228'000 over 30 years compared to a simple world ETF bought on IBKR.

And mind you, I’ve been generous with the 3b in this calculation, using 1.5% net return for the life insurance policy, when many Helvetia, Swiss Life or Zurich contracts deliver less…

So even being optimistic on pillar 3b, the result is crystal clear: the “tax deduction” your insurer sells you never makes up for the fees + the mediocre return of the product.

What if my insurance “advisor” is very convincing…?

Let’s go through some important reminders:

- An insurance advisor or broker earns a commission (starting year 1!) on 3b life insurance products: typically 2 to 4% of the total contract premiums

- On a 3b contract at CHF 4'800/year over 30 years (i.e. CHF 144'000 contributed), the commission can reach CHF 3'000 to 6'000, paid upfront in the first few years!

- That’s why these products get pushed hard, even when they’re bad for the client

To see if your advisor is still so convincing, run a simple test: ask them to give you the net return (after ALL fees) over 20 years, and compare with a global ETF. If they refuse or dodge, you’ve got your answer ;)

You can also ask for the year-by-year surrender value table: it’s legally mandatory, and it shows exactly how much you lose if you cancel before term.

Pillar 3b: the bottom line

Pillar 3b as such isn’t a bad product: it’s just the name the law gives to all your unrestricted savings. The problem is what gets sold under that name.

The numbers are clear: NEVER sign a “3b” life insurance contract. Not in Geneva, not in Fribourg, not anywhere else. Even if your advisor pulls out a tax table with green arrows. The cantonal deduction (when it exists) NEVER makes up for the product fees.

And if you’ve already signed: every extra year you hold onto your 3b costs you ~CHF 7'600 in lost future wealth (CHF 228'000 / 30 years). The best time to cancel is today. I also recommend reading this article: Close your 3rd pillar life insurance without further delay.

And if you want to optimize your pension and your taxes, focus all your attention on what actually makes sense for you, by maxing out your pillar 3a with VIAC or finpension every year.

Pillar 3b FAQ

What’s the difference between pillar 3a and 3b?

Pillar 3a is deductible everywhere in Switzerland but locked until retirement, with an annual cap (CHF 7'258 in 2026). Pillar 3b is unrestricted (withdraw whenever you want) but only deductible in Geneva and Fribourg AND only as a life insurance.

Can you combine pillar 3a and 3b?

Yes. They’re complementary and independent. The 3a cap doesn’t limit 3b, and vice versa.

What’s the pillar 3b cap in 2026?

There’s no legal contribution cap. However, the tax deduction cap for a life insurance is:

Geneva

- Single: CHF 2'345

- Self-employed without pillar 2: CHF

- With an extra deduction per additional child (not enough to make it a good deal regardless)

Fribourg

- Single: CHF 750

- Married: CHF 1'500

- With an extra deduction per additional child (not enough to make it a good deal regardless)

And you can absolutely contribute (read: save) beyond that. It just won’t be tax-deductible anymore.

Is pillar 3b worth it for an expat or cross-border commuter?

No. If you’re not taxed in Switzerland, you don’t deduct anything, and the tax argument (which is flawed anyway!) collapses. A DIY ETF investment with Interactive Brokers will be way more effective.

Can you open a pillar 3b with VIAC or finpension?

Technically, the robo-advisor solutions from finpension and VIAC fall under the “pillar 3b” category. But you can’t deduct them from taxes, since they aren’t life insurance contracts.

As for pure life insurance products, VIAC does offer one, which you can therefore deduct in the cantons of Geneva and Fribourg (if you actually need it, of course).

But VIAC and finpension don’t offer other shady “pillar 3b tied to a life insurance” packages. Thankfully! And the reason is simple: they don’t want to build financial scams with life insurance under the pretext of saving you taxes. They even explain this in detail, as seen in this finpension article: Taxes on pillar 3b: what about contributions and withdrawals?

Bank vs insurance pillar 3b: what’s the difference?

Bank 3b is a simple savings account (no fees, low return), and it’s never tax-deductible. That’s also why no bank offers such a product. Insurance 3b includes death or disability coverage, with fees of 20 to 30% of premiums. Run away!

But at least pillar 3b withdrawals aren’t taxed, unlike pillar 3a?

Yes, that’s true: the capital from a 3b life insurance is generally exempt from income tax at withdrawal. Whereas 3a capital is taxed at a reduced rate, around 5 to 10% depending on the canton.

Except once you run the numbers: on a 3a capital of ~CHF 130'000 at withdrawal, the tax is around CHF 7'500 to 11'000 in Geneva for example.

That’s ~3 to 5% of the CHF 228'000 delta calculated above. In other words, you save CHF 10'000 in taxes at withdrawal… for leaving CHF 228'000 on the table over 30 years. Thanks but… no thanks!

Even worse: throughout the entire contract, the surrender value of your 3b is subject to wealth tax every year (unlike 3a, which is exempt). This further erodes your theoretical tax gain.

Is pillar 3b more flexible than a brokerage account?

On paper yes, in practice no.

First: a brokerage account (like with Interactive Brokers, or Saxo) is just as flexible. You sell your ETFs in 2 clicks and your cash is in your bank account within a few business days. No notice period, no penalty, no “surrender value”.

Second: a 3b life insurance contract has a surrender value lower than the premiums paid for the first 10 to 15 years of the contract. If you exit after 5 years, you often recover only 50 to 70% of what you contributed. Safe to say the “flexibility” of the 3b mostly exists on the marketing brochure.

In practice, a world ETF bought through your online brokerage is therefore more flexible than a 3b, with zero exit penalty.

My insurer is offering me a pillar 3b, should I sign?

No, not before simulating the opportunity cost versus a stock-market investment. An insurance broker is paid on commission for this product: they’re not neutral. Run for the hills!