The closer you get to financial independence, the more practical questions pile up. And one of them keeps coming back: do I still have to pay OASI contributions if I stop working?

Short answer: yes, you keep paying OASI contributions even without a salary. And depending on your wealth, it can add up to several thousand francs per year.

Good news: you have two ways to handle this, and one of them is significantly cheaper than the other.

This is actually one of the questions I’ve been asking myself as I approach my own financial independence. I started digging into the topic while talking to Patrik, my co-founder of FI Planner, who was going through this himself. I took the opportunity to see how it would apply to my own situation, while cross-checking everything with FI Planner to understand the mechanics and make the optimal choice from a tax perspective.

Why you still have to pay OASI contributions after leaving your job

In Switzerland, every resident between 20 and 65 is required to contribute to the OASI (to be precise: starting January 1st after turning 20). No exceptions.

What changes when you stop working is the calculation basis. You go from “gainfully employed” to “person not in gainful employment.” And with that, the way OASI calculates what you owe changes completely.

Why does this matter? Because every year without contributions (or with insufficient contributions) creates a gap. And this happens more often than you’d think: a stay abroad, forgetting to register as non-employed after a resignation, or a period of studies without contributions. Every gap reduces your future OASI pension. To receive a full pension at 65, you need 44 complete contribution years (for men, 43 for women, but being aligned to 44 under the OASI 21 reform).

If you stop at 40, you still have 25 years to cover as a non-employed person. That’s not trivial.

Two scenarios after FIRE: with or without a salary

When you stop working before 65, the OASI puts you in one of two categories. And the amount you pay changes drastically depending on which one you fall into.

Scenario 1: You have no gainful employment at all

This is the classic FIRE (“Financial Independence, Retire Early”) scenario: no salary, no mandate, nothing. The OASI then calculates your contributions based on this formula:

Determining net worth = Net worth + (annual pensions × 20)

The “annual pensions” include any pension you receive: OASI, DI, foreign pensions, or even your spouse’s if they’re already retired. But if you’re FIRE at 40, you’re typically not receiving any of these yet. Your annual pensions are zero.

Determining net worth = Net worth + (0 × 20) = Net worth

For a married couple, each spouse contributes based on half of the combined total. In practice: the OASI adds up both spouses’ wealth, then divides by two. Each spouse pays on their half. Example: CHF 2'000'000 in combined wealth = each spouse contributes as if they had CHF 1'000'000.

To calculate your net worth, the OASI adds up:

- savings accounts

- stock market investments (shares, bonds, funds, ETFs)

- real estate (note: the OASI uses the federal apportionment value, not the cantonal tax value. Some cantons massively undervalue real estate, and the correction can range from 110% to over 300% depending on the canton)

- surrender values of life insurance policies

What doesn’t count towards your wealth:

- your 2nd pillar / vested benefits

- assets held within your LLC/Ltd (but the tax value of your shares does count toward your taxable wealth, more on that below)

Important for Swiss FIRE people: your passive income (dividends, rental income from personally owned property) is not subject to OASI contributions and does not count as gainful employment. You remain “non-employed” even if you earn CHF 50'000/year in rental income. Only your wealth is used in the calculation.

The rate is roughly 0.2 to 0.3% of your determinant wealth.

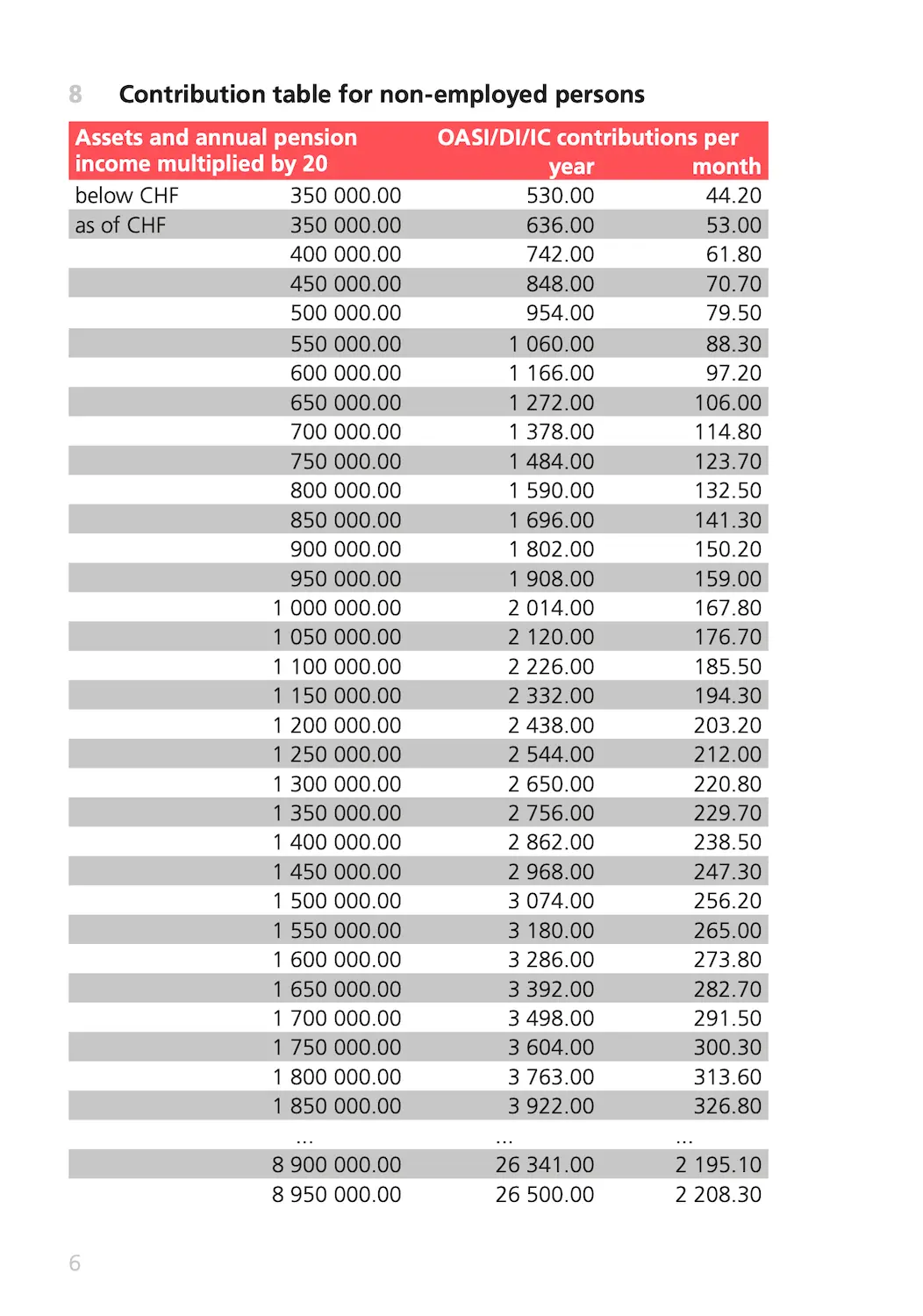

Here are the actual numbers:

| Determining net worth | Annual contribution |

|---|---|

| < CHF 350'000 | CHF 530 (minimum) |

| CHF 500'000 | CHF 954 |

| CHF 1'000'000 | CHF 2'014 |

| CHF 1'500'000 | CHF 3'074 |

| CHF 2'000'000 | CHF 4'134 |

| CHF 3'000'000 | CHF 6'254 |

Source: OASI Factsheet 2.03, as of January 1, 2026

OASI 2026 contribution schedule: contributions for persons not in gainful employment based on wealth (Factsheet 2.03)

The minimum contribution is CHF 530/year. The maximum is CHF 26'500/year (reached at CHF 8'950'000 in determinant wealth).

A little note that won’t exactly make your day: “The compensation offices charge, in addition to the contributions, an administration fee of up to 5% of the contributions.”

Scenario 2: You have a small job or pay yourself a small salary through your company

If you maintain gainful employment recognized by the OASI, you contribute based on your salary. Not on your wealth.

This is often much cheaper.

But be careful: the OASI doesn’t accept just any activity. To be considered “gainfully employed” for OASI purposes, two conditions must be met:

- The activity must be carried out on a sustained basis at a minimum of 50%, and for 9 months or more per year

- Your salary-based contributions (employee + employer share) must be at least half of what you would pay as a non-employed person

If these conditions aren’t met, your compensation office does a comparative calculation and may charge you the non-employed rate. But your salary-based contributions are deducted from the amount, so you don’t pay double, just the difference.

In any case, the absolute minimum remains CHF 530/year, which corresponds to an annual gross salary of CHF 5'000.

Here’s a concrete example:

- You have wealth of CHF 2'000'000

- With no employment at all, you pay: CHF 4'134/year (see the schedule above)

- To be recognized as “gainfully employed” by the OASI, your salary-based contributions (your share + your employer’s, i.e. your Ltd) must reach at least half of that:

- CHF 4'134 / 2 = CHF 2'067 minimum in contributions

- The combined OASI/DI/EO employee rate (both shares combined) = 10.6%

- So minimum gross salary needed: CHF 2'067 / 10.6% = ~CHF 19'500/year (or ~CHF 1'625/month)

What you pay in each scenario:

| Situation | Annual contribution |

|---|---|

| Non-employed (wealth CHF 2M) | CHF 4'134 |

| Salary CHF 19'500 via your Ltd | ~CHF 2'067 |

| Savings | ~CHF 2'067/year |

If you’re FIRE with significant wealth and you find a qualifying small job, you cut your OASI bill in half.

That’s not nothing, since those CHF 2'067 invested in the stock market over 10 years would give you a tidy CHF 30'565. That said, the question remains whether your freedom is worth it, depending on what you plan to do once you’re financially independent.

What these contributions give you (or don’t give you)

Alright, you pay your contributions every year, that’s great, but what do you actually get in return?

What you get

1. An old-age pension at 65

This is the big one. With a complete contribution period (44 years for men, 43 for women), the monthly pension ranges from CHF 1'260 (minimum) to CHF 2'520 (maximum). If you’re married, the two combined pensions are capped at 150%, or CHF 3'780/month max.

The exact amount depends on your average determinant annual income over your entire career. The more you earned (and contributed), the higher your pension, up to the maximum limit. Good news: the OASI pension is indexed to a blended rate (wages + prices), so it tracks inflation. That’s not the case for 2nd pillar pensions.

New in 2026: a 13th OASI pension is paid in December, equal to 1/12 of your annual pension (first payment: December 2026).

2. Disability insurance (DI)

As long as you contribute to the OASI, you also contribute to disability insurance (DI). If you become disabled before 65, you’re entitled to a DI pension calculated on the same basis as the old-age pension (CHF 1'260 to 2'520/month).

It’s not a lot, but it’s a minimum safety net.

3. Survivor pensions for your family

If you pass away, your spouse and children may receive a survivor’s pension (widow/widower: CHF 1'008 to 2'016/month, orphans: CHF 504 to 1'008/month).

The key point for Swiss FIRE people

Watch out for this subtlety: your OASI pension depends on two things.

- The number of contribution years: each missing year reduces your pension by about 2.3%. This is the pension scale (44 = full pension).

- Your average determinant annual income: this is the average of all your income subject to contributions over your entire career. It determines whether you receive the minimum or maximum pension.

What this means in practice is that if you worked 20 years with a good salary, then pay the minimum (CHF 530/year) for 25 years, your pension will be somewhere between the minimum and maximum. The years at CHF 530 will pull your average down.

But the most important thing: paying at least the minimum every year guarantees zero gaps. And zero gaps = pension on the 44-year scale (= full pension). Your pension might not be at the maximum, but you won’t have any additional reduction from missing years.

What these OASI contributions do NOT give you

This is where it gets important if you’re FI (= Financially Independent). The OASI is the bare minimum. When you stop working, you also lose (meaning none of this is covered by the OASI, employed or not):

- The 2nd pillar: no more BVG/LPP pension contributions, no more death and disability coverage through your pension fund. Your balance stays in a vested benefits account, it no longer grows through employer contributions, but it can keep working for you if you invest it properly.

- Accident insurance (LAA): as an employee, you were covered. As a non-employed person, you must include accident coverage in your LAMal (basic health insurance). Make sure to do this within 31 days of your last day of employment.

- Daily sickness allowance: no more employer = no more salary if you get sick. If you want coverage, you’ll have to pay for it yourself.

- Unemployment insurance (ALV): if you resign voluntarily, you’re not entitled to benefits. Worth noting: if you go through a period of unemployment (layoff), the unemployment office covers your OASI contributions, so you stay covered with no gaps.

These topics deserve their own article (coming soon). But here’s the bottom line: your OASI contributions as a non-employed person cover the 1st pillar and nothing else. The rest is up to you.

Wealth in a company: what the OASI doesn’t see

You may have read above that wealth held in your Ltd or LLC “doesn’t count” toward your personal wealth. That’s true, but it needs some nuance.

If you're looking for a Swiss company name that doesn't exist in the Swiss commercial register (Zefix), this one's still available ;)

Why your Ltd’s assets don’t count toward your OASI wealth

A Ltd or LLC is a separate legal entity. Its bank accounts, investments, and assets belong to the company. Not to you.

When the OASI calculates your non-employed contributions, it uses your personal wealth as reported by the tax authorities. And in your tax return, the company’s assets don’t appear directly.

What does appear is the tax value of your shares (or company stakes).

Tax value ≠ actual value

This is where it gets interesting. The tax value of unlisted securities (like shares in your own Ltd) is calculated by the tax authorities using the “practitioner method” (CSI Circular No. 28). In short:

- They take the substance value (≈ net assets of the company)

- They take the earnings value (≈ capitalized profits)

- They weight the two

For a typical operating company, here’s the formula: (2 × earnings value + 1 × substance value) / 3.

Result: if your company has CHF 1'500'000 in assets but generates little profit, the tax value of your shares will be significantly lower than CHF 1'500'000. And it’s this reduced value that counts toward your OASI determinant wealth.

Concrete example: personal wealth vs. company wealth

Let’s take two profiles with CHF 2'000'000 in total assets:

| Situation | OASI determinant wealth | Annual contribution |

|---|---|---|

| Everything in personal name | CHF 2'000'000 | CHF 4'134 |

| CHF 300'000 personal + Ltd (tax value CHF 1'100'000) | CHF 1'400'000 | ~CHF 2'862 |

| Difference | ~CHF 1'272/year |

The savings come from the gap between the company’s actual assets and the tax value of your shares. The more assets your company holds with few distributed profits, the bigger this gap.

The Mustachian combo: company + small salary

This is where both strategies stack. If on top of holding part of your wealth in your Ltd, you also pay yourself a small salary (scenario 2 above), you switch to “gainfully employed” status. And then your wealth, including the value of your shares, is no longer part of the calculation at all.

Using the same example:

- Personal wealth reduced thanks to the Ltd = lower “gainfully employed” threshold

- You pay yourself a salary from the Ltd = you only contribute on the salary

- The company’s wealth stays invisible to the OASI

This is the most advantageous combination for someone who is FI with an existing company.

Creating a Ltd just for the OASI: rarely worth it

Creating a Ltd just to optimize your OASI contributions is not a good idea. The fixed costs (accounting, auditing, capital tax, admin) quickly exceed the savings if you don’t already have a business that justifies the structure.

However, if you already have a company, keeping it open after becoming FI and paying yourself a small salary can be worth it. The math depends on your total wealth, the tax value of your shares, and the running costs of your company.

When to change your OASI status: before or after you resign?

Timing matters. Not for complex tax reasons, but to avoid ending up in an administrative no man’s land.

If you’re married and your spouse still works

Check this one first, because it’s potentially the simplest scenario.

If your spouse meets all three of these conditions, you are exempt from OASI contributions as a non-employed person:

- They work at least 50%

- For 9 months or more per calendar year

- Their OASI contributions reach at least CHF 1'060/year (= double the minimum)

CHF 1'060 in contributions corresponds to a gross salary of about CHF 10'000/year. If your spouse works even part-time, this is probably already the case.

In this scenario, you pay zero. And you still have zero gaps in your OASI account. This is by far the best option if it applies to your situation.

If you have a company (Ltd/LLC)

Prepare the ground before leaving your job:

- Check that your Ltd is registered as an employer with a compensation office. If it already is (because you were paying yourself a salary before), you’re good

- Determine the minimum salary you’ll pay yourself (see the calculation in scenario 2 above)

- Start paying yourself this salary from the month after your resignation, so there’s no gap between the two

The idea is to go directly from “employee at your employer” to “employee of your own Ltd.” Without interruption. That way, you’re never classified as non-employed and your compensation office doesn’t come after you based on your wealth.

If you have neither a working spouse nor a company

You’ll automatically be classified as a “person not in gainful employment.” Here’s what you need to do:

- Register with the compensation office in your canton (or your local OASI office). Do it quickly after your employment ends. If you wait too long, the office will find you through tax data and will charge you the outstanding contributions plus 5% interest per year. Best to avoid that ;)

- Pay at least the minimum contribution (CHF 530/year) to avoid gaps

- Include accident coverage in your LAMal within 31 days (reminder, already mentioned above)

Timing within the year

If you have a choice, resigning at the end of the calendar year makes things simpler. Your employer pays your OASI contributions on your salary through your last payslip. The new status starts on January 1st.

If you leave mid-year, your compensation office will do a comparative calculation for the remaining part of the year. It’s not a dealbreaker, but it creates a bit more admin.

My personal case (close to FI): how we plan to handle OASI contributions

I’m employed, married, two kids, and approaching financial independence in Switzerland. I also have a Ltd through which I manage the blog and my real estate investments. Here’s how I’m thinking about the OASI question for my own situation.

Phase 1: Mrs. MP keeps working

Our initial plan was to stop at the same time. That was the theory… Because Mrs. MP plans to keep working for another 1 to 2 years after I leave, until she’s psychologically ready. And yes, mental preparation is a real component of the FIRE plan, not just the numbers.

During this period, I’m covered. As long as she works at 50% or more, for at least 9 months per year, and her OASI contributions exceed CHF 1'060/year, I’m exempt from contributions as a non-employed person. I pay zero, and I have zero gaps.

But in parallel, knowing myself, I’ll be having fun with some real estate projects, and probably developing new blog-related projects during those two years (unless I’m hiking 7 days a week, who knows!). This income will go through my Ltd, which means I can pay myself a salary and be recognized as “gainfully employed” for OASI purposes.

Result: I’m doubly covered. By Mrs. MP’s work on one side, and by my own salary through the Ltd on the other.

Phase 2: Mrs. MP stops, but my Ltd is still running

When Mrs. MP is ready to stop, I’ll cover her. As long as I pay myself a sufficient salary through my Ltd (blog + real estate), I’m “gainfully employed” for OASI purposes. And a gainfully employed spouse who pays at least CHF 1'060/year in contributions exempts the other spouse.

In practice: my Ltd income covers both my own contributions AND Mrs. MP’s. We both pay zero in non-employed contributions, and we both have zero gaps.

This is the most likely scenario for us in the medium term.

Phase 3: The day we really unplug everything

If at some point we no longer generate enough income through the Ltd, and we really can’t be bothered to maintain any activity, we’ll both switch to non-employed status for OASI purposes.

As a married couple, each of us will contribute on half of the combined wealth, roughly CHF 1'300'000 per person. That gives us ~CHF 2'650/year per person, so ~CHF 5'300/year for the household.

It’s not negligible, but it’s also not an amount that breaks our FIRE plan. Put it in perspective with other fixed expenses (LAMal, taxes, etc.).

And what really reassures me is that all the fancy calculations for this phase are accounted for in FI Planner, and everything checks out :)

Honestly, this is the least likely scenario. I’d really have to spend my days hiking and let the blog and real estate go to waste. We’re not there yet.

My checklist before D-Day

- Confirm that Mrs. MP stays “gainfully employed” for OASI purposes during phase 1 (50%, 9 months, CHF 1'060/year minimum in contributions)

- Set up the salary through my Ltd to follow directly after my employment ends

- Verify that my Ltd income also covers Mrs. MP for phase 2 (CHF 1'060/year minimum in contributions)

- Request an OASI account statement to check for any existing gaps

- Include accident coverage in my LAMal within 31 days

- Budget the OASI contributions for the scenario where we really stop everything (phase 3)

FAQ: OASI and FIRE in Switzerland

Do I have to pay OASI contributions if I no longer work?

Yes. Every person living in Switzerland between 20 and 65 must contribute, even without income. As a non-employed person, your contributions are calculated based on your wealth. Minimum: CHF 530/year.

How much do I pay in OASI if I’m FIRE with CHF 2'000'000 in wealth?

As a non-employed person with CHF 2'000'000 in determinant wealth, you pay about CHF 4'134/year. If you’re married, the wealth is divided by two: each spouse contributes on CHF 1'000'000, or ~CHF 2'014/year per person.

Does my 2nd pillar count as wealth for the OASI?

No. Your 2nd pillar balance (pension fund or vested benefits) is not included in the OASI determinant wealth calculation. Only your taxable personal wealth counts (accounts, stock market investments, real estate, surrender values of life insurance policies).

How can I reduce my OASI contributions after FIRE?

The most effective method: maintain a small gainful employment (part-time job or salary through your own Ltd/LLC). You then contribute on your salary instead of your wealth. With CHF 2M in wealth, this can cut your bill in half. If you’re married and your spouse still works, you may even be fully exempt.

My spouse works part-time. Does that cover me?

Yes, if three conditions are met: your spouse works at least 50%, for 9 months or more per year, and their OASI contributions reach at least CHF 1'060/year (double the minimum). In that case, you’re exempt and have no gaps.

Does the wealth in my Ltd count for the OASI?

Not directly. The company’s assets belong to the company, not to you. However, the tax value of your shares (calculated using the practitioner method) is included in your taxable personal wealth. This value is often lower than the company’s actual assets.

What happens if I have OASI contribution gaps?

Each missing year reduces your pension by about 2.3%. You can fill gaps, but only within 5 years. After that deadline, it’s too late. That’s why you should pay at least CHF 530/year every year, even if you’re FIRE.

Can I take my OASI pension early or defer it?

Yes. Since the OASI 21 reform, you can receive your pension flexibly between ages 63 and 70. Taking it early reduces your pension (“actuarial reduction” in fancy jargon), deferring it increases it. The exact calculation depends on the number of months of anticipation or deferral.

Conclusion: OASI contributions when you become FIRE

Here are the concrete OASI contribution amounts for a wealth of CHF 2'000'000 (the most relevant case for someone who is FIRE in Switzerland):

| Situation after FIRE | Annual OASI contribution |

|---|---|

| Non-employed, single | CHF 4'134 |

| Non-employed, married (each on CHF 1M) | CHF 2'014 per person |

| Spouse gainfully employed (≥ 50%, ≥ 9 months, ≥ CHF 1'060 in contributions) | CHF 0 |

| Small salary via your Ltd (~CHF 19'500/year gross) | ~CHF 2'067 |

| Small salary via your Ltd + wealth in the company | even less |

| Absolute minimum (regardless of scenario) | CHF 530 |

Three things to remember:

- Your spouse still works? You’re probably exempt. Check the three conditions (50%, 9 months, CHF 1'060).

- You have a company? A small salary switches you from “non-employed” to “gainfully employed”, and your wealth drops out of the calculation. This is often the best option.

- Neither? Pay at least CHF 530/year to avoid gaps. And request an OASI account statement to make sure you’re in the clear.

For the MP family, the plan has three stages: first, Mrs. MP keeps working part-time while I keep running my personal projects through my Ltd (we’re doubly covered). Then, when she stops, my Ltd income covers both our contributions. And if one day we really unplug everything, we’ll pay our ~CHF 5'300/year in non-employed contributions for the two of us. That’s manageable.

And you, what strategy are you planning for your OASI contributions once you’re FI?