finpension Invest referral code 2026

Use the promo code "MUSTBC" when you sign up on the finpension app.

You'll get a CHF 25 fee credit as a welcome bonus, provided you transfer or deposit at least CHF 1'000 within the first 12 months after creating your finpension account.

For now, the code can only be entered by new finpension sign-ups: if you already used it for your finpension third pillar, you can't enter it again for your finpension Invest account just yet. finpension is working on it, so reusing the code (for an extra CHF 25 fee credit, and to support the blog along the way, thanks!) should become possible during the summer. I'll update this article as soon as it's live.

I’ve received many questions about finpension Invest since its launch in May 2024.

It’s the same finpension that offers (according to my Mustachian criteria) one of the best pillar 3a accounts in Switzerland, tied with VIAC.

I’ve been a client of their third pillar myself for years.

So every time finpension launches a new product, it piques my curiosity ;-)

finpension Invest in a nutshell

In short, here’s my review of finpension Invest, starting with its strengths:

What I like about finpension Invest

- The best net return of all Swiss robo-advisors, thanks to its Irish ETFs that cut the US withholding tax in half (from 30% to 15%), with the option to reclaim the remaining 15% via the DA-1 form (up to ~0.30%/year extra, though this DA-1 part isn’t guaranteed yet, see below)

- Some of the lowest fees in Switzerland (~0.47% all-in for the Global 100 strategy, almost tied with VIAC Invest)

- A minimum investment of CHF 1 to get started, ideal for taking your first step into the stock market

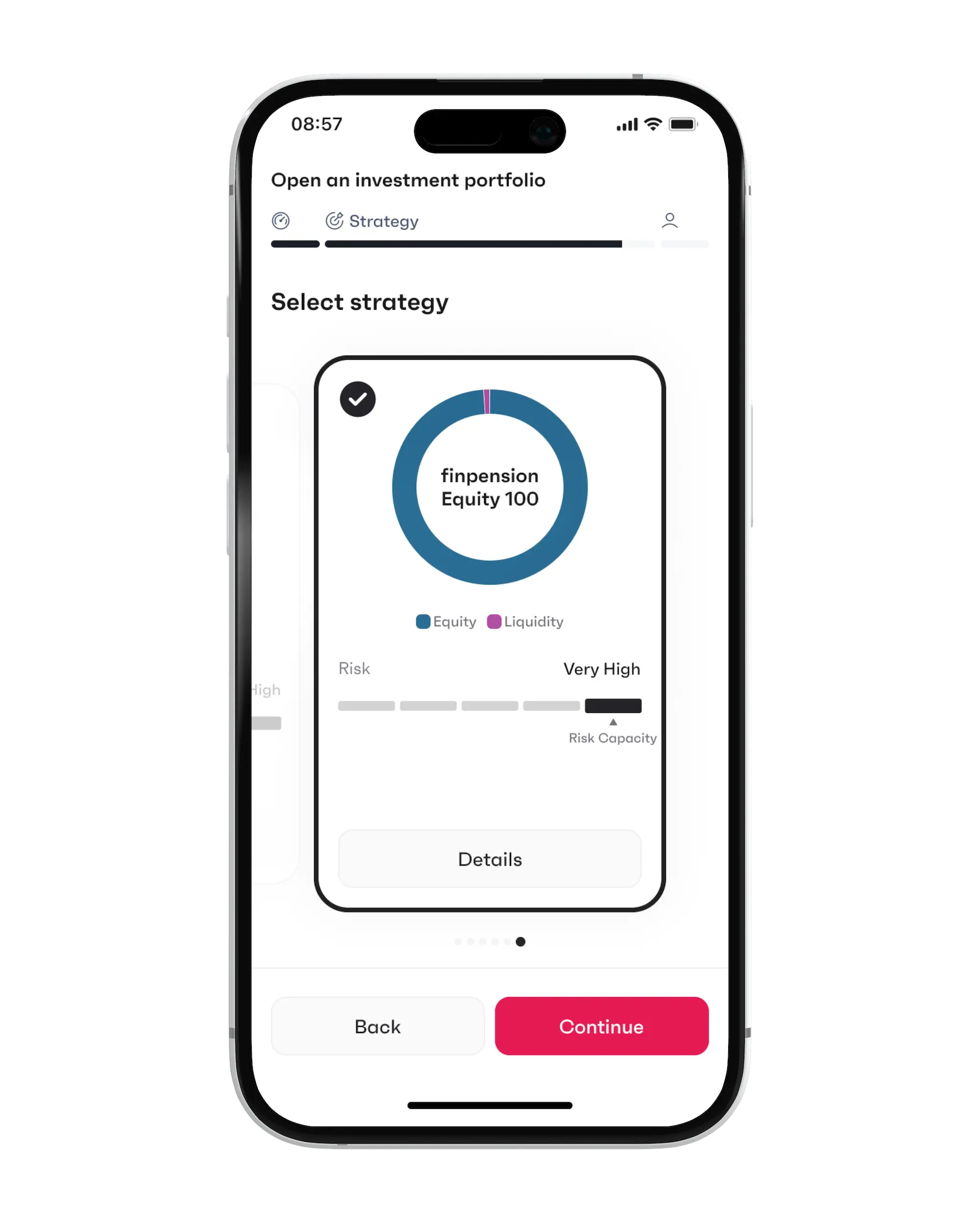

- A 100% global stocks strategy (finpension Equity 100), exactly what you need to build your wealth over the long term

What could finpension Invest improve in the future?

- Offer a cash option for the defensive part of your portfolio (as of today, only money market funds)

MP’s recommendation

If you want to invest your savings on autopilot (because you don’t feel ready for DIY investing yet), then finpension Invest with the finpension Equity 100 strategy (Global focus) is the best solution for you. It’s the Swiss robo-advisor that leaves the most net return in your pocket in 2026.

What is finpension Invest?

It’s the same automated investment platform as the one used by your finpension 3a, except this one is for investing your private savings (outside of your 3a or vested benefits assets).

Just like with finpension 3a, you can pick one of the default strategies offered by finpension, or build your own portfolio from the list of financial products finpension gives you access to.

As a reminder, finpension is a company based in Lucerne. As of March 2026, it managed over CHF 5 billion for around 60'000 clients, and it has been profitable since 2019. It’s also registered as a securities firm with FINMA (meaning it holds your securities itself, without relying on a third-party custodian bank).

At a glance, here are the key facts about finpension Invest:

- Minimum investment: CHF 1

- Perfect to get started

- finpension Invest management fees:

- 0.39% (0.30% custody fee + 0.09% wealth management fee)

- Bonus: the 0.30% custody fee is tax-deductible, which at a 20% marginal tax rate saves you about 0.06% more (after-tax view)

- Plus the fund costs (TER), around 0.08% to 0.10% on average

- That’s a total of about 0.47% to 0.49% per year, all-in (depending on your strategy)

- This makes it one of the cheapest robo-advisors in Switzerland fee-wise (almost tied with VIAC Invest).

- And finpension takes no margin on currency exchange operations, and charges no subscription or redemption fees (a Swiss stamp duty does apply on ETF transactions though: it’s a federal tax that can’t be bundled into the fee; VIAC’s in-house funds avoid it but carry higher spread costs instead, so the net result is comparable)

Rock-bottom fees are nice. But before comparing finpension Invest to the competition, we need to talk about the choice that will weigh much more on your final wealth: your investment strategy.

100% stocks while you build your wealth

This is probably where I differ from a purely encyclopedic robo-advisor comparison: I have a clear angle.

I aim for financial independence, and to get there, I invest intelligently: long term, buy and hold.

As long as you’re building your wealth, your best bet is to stay 100% in stocks. Instead of being afraid and taking refuge in bonds (which drag down your returns over 20-30 years), educate yourself about how the stock market works so you can stay the course during dips and crashes.

Once you’re financially independent (FI), you can add a share of bonds to smooth out the ride. But honestly, you don’t even have to.

So the Global 100 strategy (100% global stocks) is what interests me, at both finpension Invest and VIAC Invest. And that’s the basis on which I compare finpension Invest to the other robo-advisors in this article (to dig deeper: Why I’m switching from the Bogleheads strategy to 100% stocks).

The alternatives to finpension Invest, and how they compare

Let’s now compare the costs of the main Swiss robo-advisors (finpension Invest, VIAC Invest, findependent, True Wealth, Selma and Inyova):

| Provider | Management fees | Other fees (charged separately) | Product costs (TER) | Total costs | Min. investment |

|---|---|---|---|---|---|

| finpension | 0.39% | Stamp duty up to 0.15% | 0.08-0.10% | 0.47-0.49% | CHF 1 |

| VIAC | 0.25% | Subscription/redemption ~0.07%/0.14% | 0.21-0.24% | 0.46-0.49% | CHF 1 |

| findependent | 0.40% | Stamp duty up to 0.15% + forex 0.50% | 0.17-0.20% | ~0.57-0.60% | CHF 500 |

| True Wealth | 0.50% | Stamp duty up to 0.15% + forex 0.10% | 0.12-0.21% | ~0.62-0.71% | CHF 8'500 |

| Selma | 0.68% | Stamp duty up to 0.15% + forex 0.25% | ~0.22% | ~0.90% | CHF 2'000 |

| Inyova | 1.20% | Stamp duty up to 0.15% | Included | ~1.20% | CHF 2'000 |

Total costs = management fees + product costs (TER); the “other fees” are one-off costs (when buying or exchanging currencies). For finpension and VIAC: Global strategy with ~100% stocks, as of June 2026.

Management fees decrease with your invested wealth: findependent down to 0.29% (from CHF 1 million), True Wealth 0.25% (above CHF 500'000), Selma down to 0.42% (from CHF 500'000), Inyova from 0.60%. Inyova invests in individual securities directly (TER included in its fee), with an ongoing migration to an in-house ETF (TER of 0.95%, launched in December 2025) worth keeping an eye on.

Fee-wise, finpension Invest and VIAC Invest are fighting for first place:

- VIAC Invest Global 100: 0.46%

- finpension Invest Global 100: 0.47% (0.39% management fees + 0.08% TER)

Basically identical.

But… because there’s a “but”…

Why finpension Invest beats VIAC Invest

With nearly equal fees, you could think finpension Invest and VIAC Invest are basically the same thing.

Except you also need to factor in taxes. Because, as you know, taxes can eat into your returns too.

And here, once again, finpension goes one step further than everyone else. As usual.

In practice, finpension Invest does two things:

- They use Irish funds, which are optimal tax-wise

- And they made a deal with BlackRock regarding US dividends, to get you the documentation needed to claim back the US withholding tax via the famous DA-1 form

Specifically, finpension Invest uses iShares ETFs domiciled in Ireland for the US stocks of the S&P 500 (which make up 66% of the Global 100 strategy). In comparison, VIAC Invest uses its own Swiss funds.

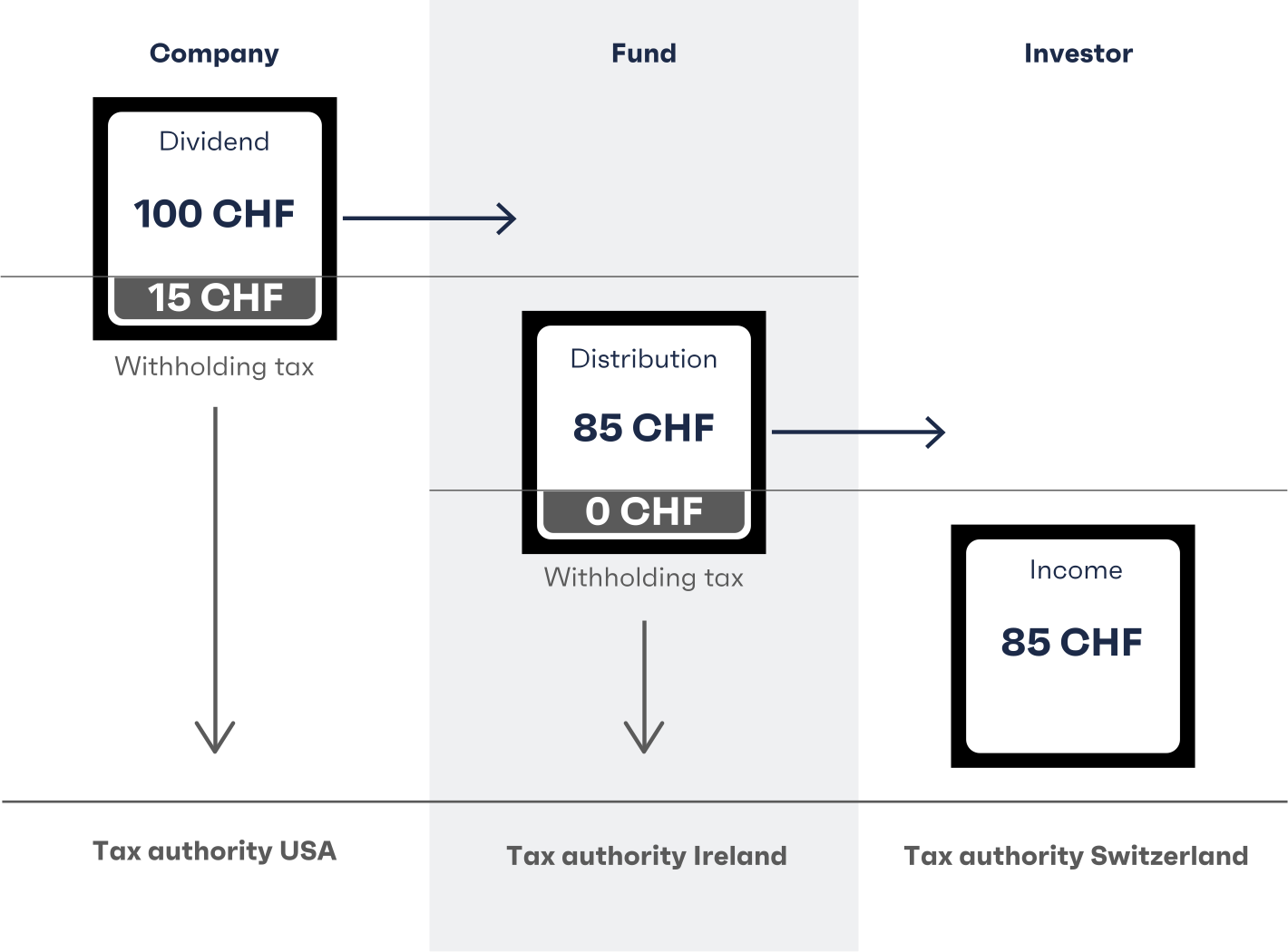

How a CHF 100 US dividend flows through an Irish-domiciled ETF: CHF 15 of withholding tax taken by the US tax administration, CHF 0 withheld at the Irish fund level, and CHF 85 paid out to the Swiss investor

Why is this a game changer? finpension explains it in detail on their website, and here’s the summary:

- By default, US dividends are subject to a 30% withholding tax.

- Thanks to the double taxation agreement between Ireland and the US, Irish ETFs already cut this withholding in half, from 30% to 15%.

- And finpension goes further: thanks to its deal with BlackRock, it provides you with the documentation to claim back the remaining 15% via the DA-1 form (lump-sum tax credit) in your tax return. That’s a performance advantage of about 0.30% per year (= 15% withholding × 2% dividend yield).

One important caveat on this DA-1 layer: this lump-sum tax credit on finpension’s reporting hasn’t been formally validated by the cantonal tax authorities yet. A court case is currently pending and the outcome is still open. finpension is convinced its reporting meets all the requirements, and that a rejection wouldn’t stand up to a judicial review, but it can’t offer any guarantee at this stage. So treat the ~0.30% DA-1 bonus as a likely, but not yet certain, upside. The first layer (Irish domicile, 30% to 15%) is automatic and unaffected by this.

On the other hand, VIAC Invest uses Swiss funds for US stocks. Part of those funds is domiciled in Ireland, but the rest suffers the full withholding, and crucially, you can’t claim it back via a DA-1 form. So VIAC remains structurally less optimized on this point.

On a Global 100 portfolio held over decades, this tax gap ends up weighing heavily through compounding.

And since net return is the only judge that matters, I rank finpension Invest slightly ahead for a Mustachian investing in 100% global stocks (Global 100) over the long term.

Note: if you insist on holding a share of bonds (a 60/40 or 40/60 profile), fees stay in the same range at both robo-advisors, but the tax advantage above weighs less in the balance, since you hold fewer US stocks.

What finpension Invest does that others don’t

Beyond fees and taxes, finpension Invest comes with some handy features, some of which are unique among Swiss robo-advisors (joint account and access to private markets):

- Joint accounts (since July 2025): handy for a couple, because if one of you passes away, the other keeps access to the portfolio. That’s pretty rare in Switzerland for a robo-advisor investment account.

- Automatic savings and withdrawal plans: you set up a standing order from your bank, and finpension invests everything automatically (within a week at most). And the other way around, you can schedule regular withdrawals (finpension’s withdrawal plan): you pick an amount (e.g. CHF 1'000/month) and a frequency (monthly, quarterly, or yearly), and finpension sells just enough shares and pays you out. This is particularly interesting for the decumulation phase once you’re FI.

- Access to private markets: you can invest in two institutional funds normally reserved for large portfolios. It’s unique among Swiss robo-advisors. I put this last on the list because it’s reserved for very high risk profiles, for a small “casino mode” part of your portfolio. Personally, I don’t use this feature, in order to stay as diversified as possible.

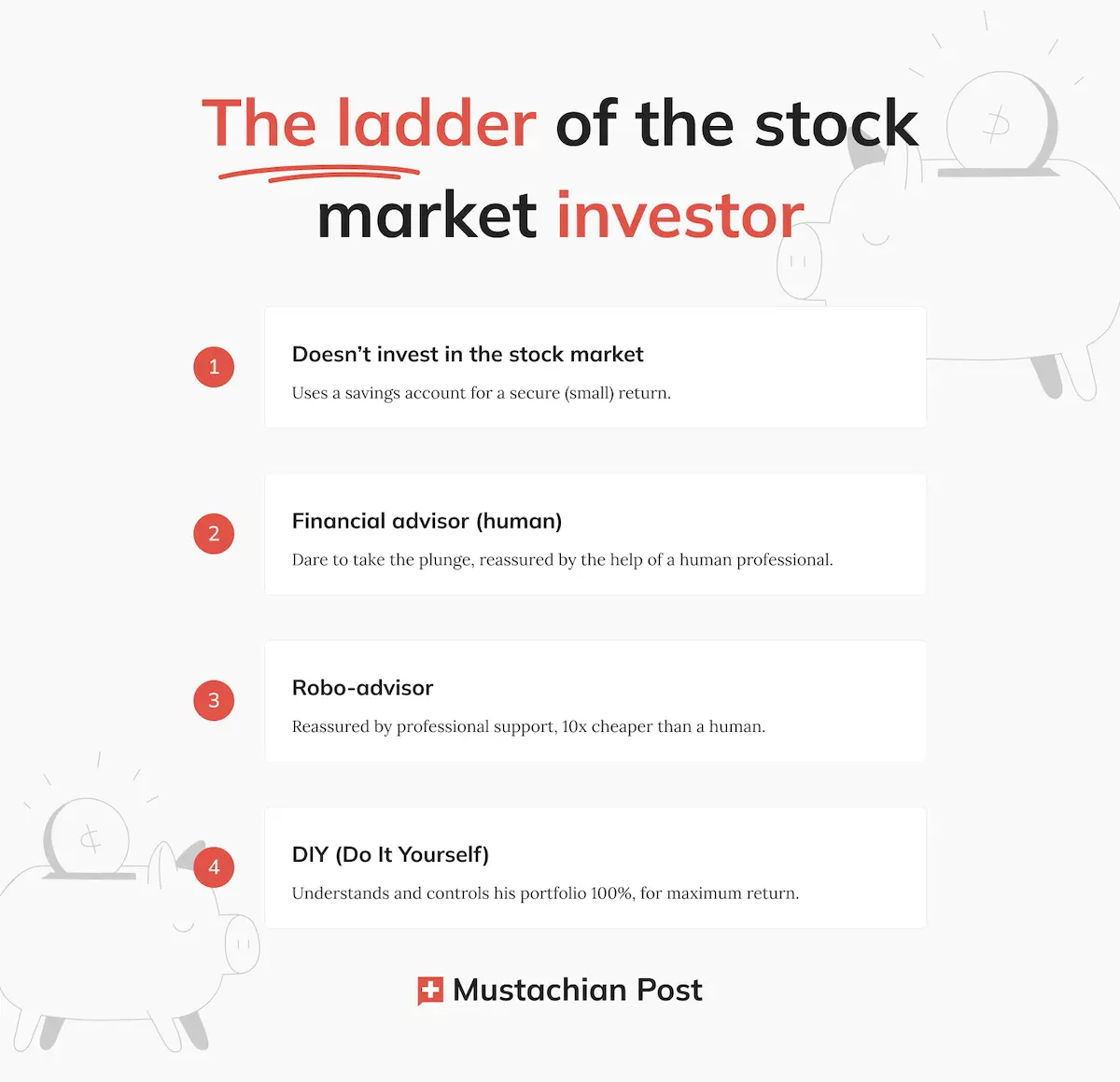

Which type of Mustachian is finpension Invest for?

I fully expect you to build up your stock market investor muscles enough to eventually invest DIY-style, and save thousands, even hundreds of thousands of CHF in fees (no joke, I did the math for you here: investing yourself vs robo-advisor).

But just like when you learn to swim, not everyone goes from the paddling pool to the Pacific Ocean on their first try. Well, some people don’t mind, hah!

But most readers tell me about their deep fear of the stock market… that they don’t know where to start… or that their parents lost a lot of money, so they have a mental block on this topic.

And that’s exactly where a robo-advisor like finpension Invest comes in: it’s the intermediate rung of the ladder of the stock market investor that lets you build confidence before going DIY.

The ladder of the stock market investor: from savings account to DIY, with robo-advisors like finpension Invest in between

Because as much as it’s better to pay the lowest fees in DIY mode, it’s 100x worse to do nothing and let your savings get eaten away by inflation in an old bank account at one of our good old traditional Swiss banks.

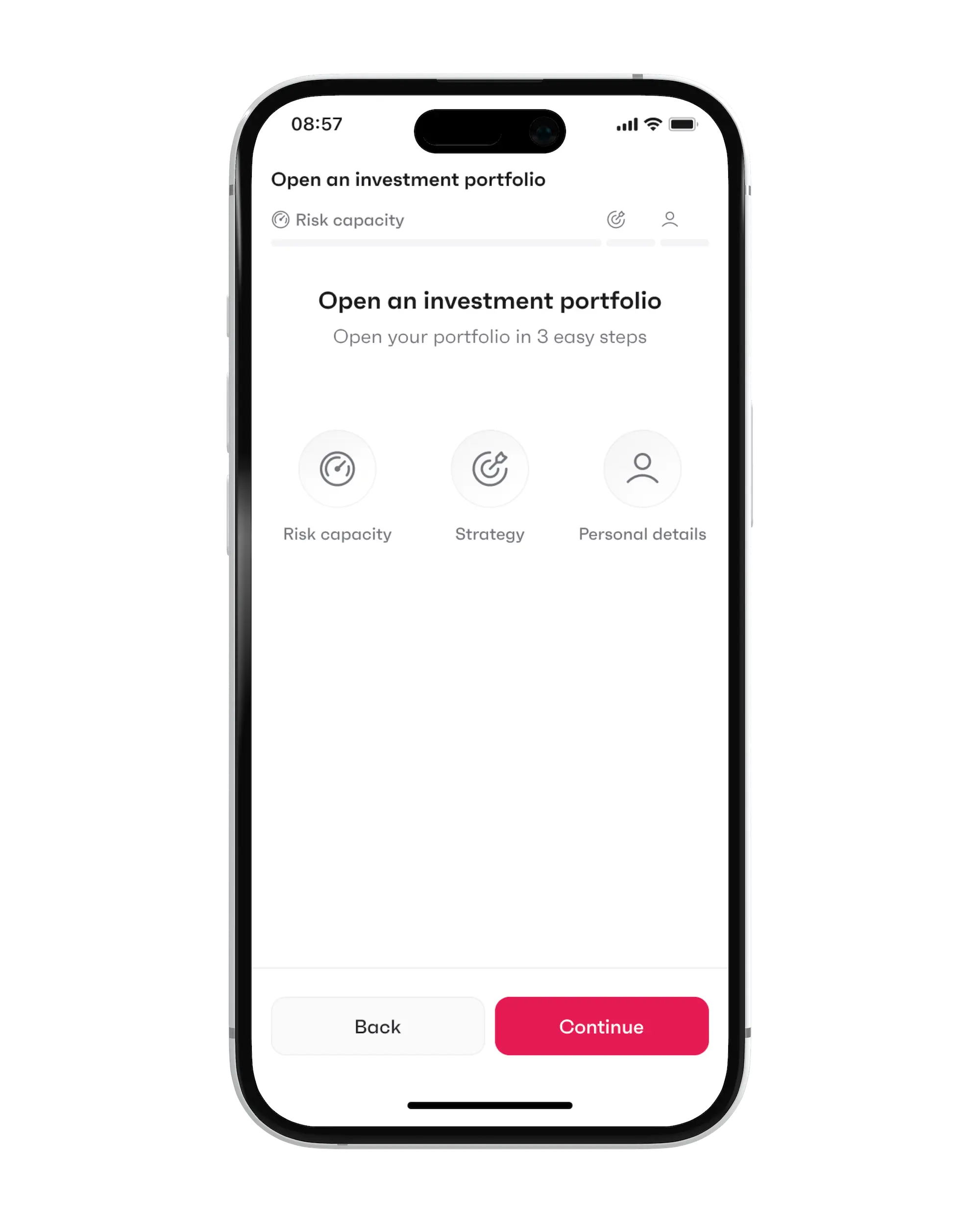

How to open a finpension Invest portfolio

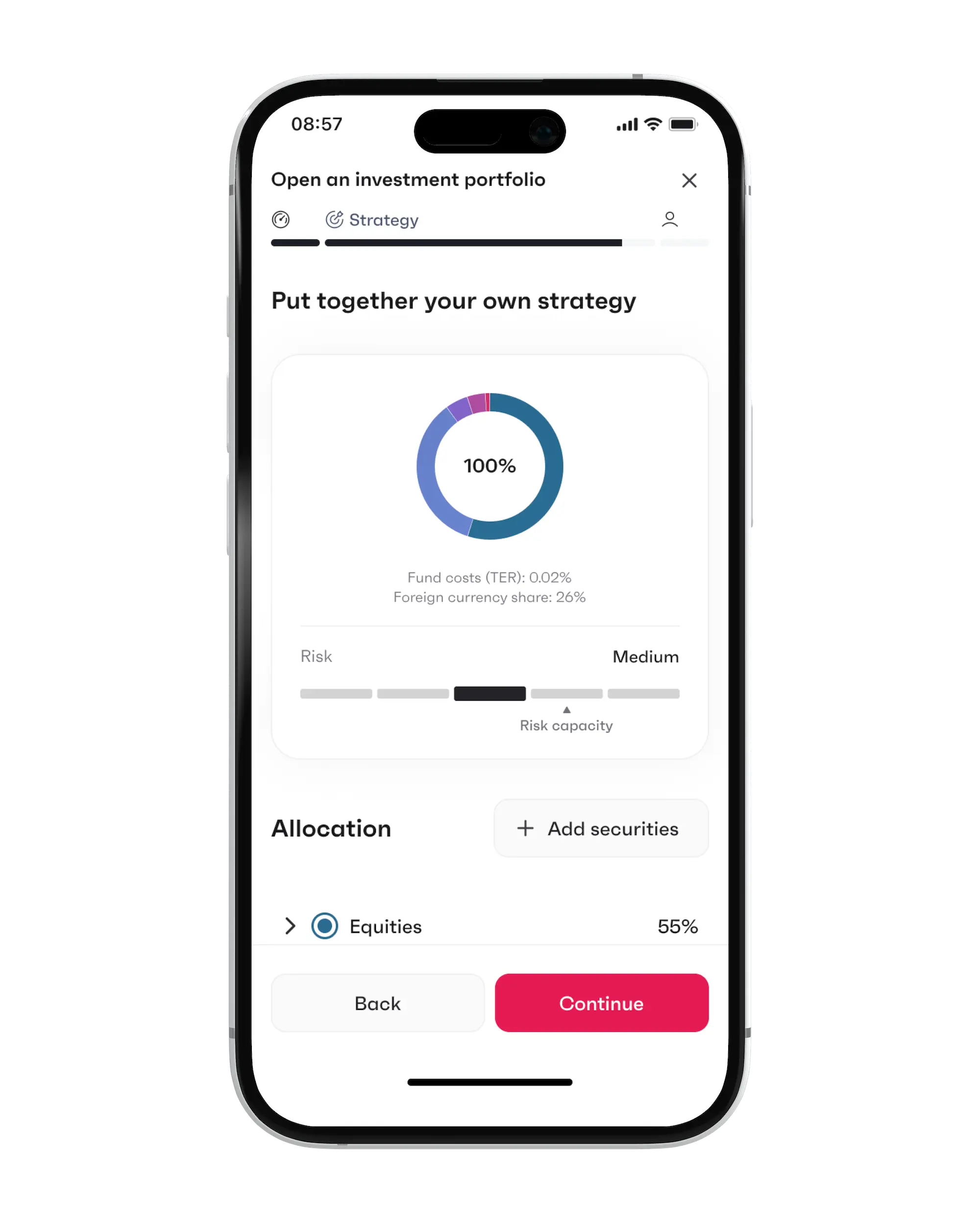

It’s pretty crazy how in 2026 you can open an investment portfolio in a few minutes, straight from your smartphone.

The whole process happens in the finpension app (or their web app), and boils down to 3 main steps:

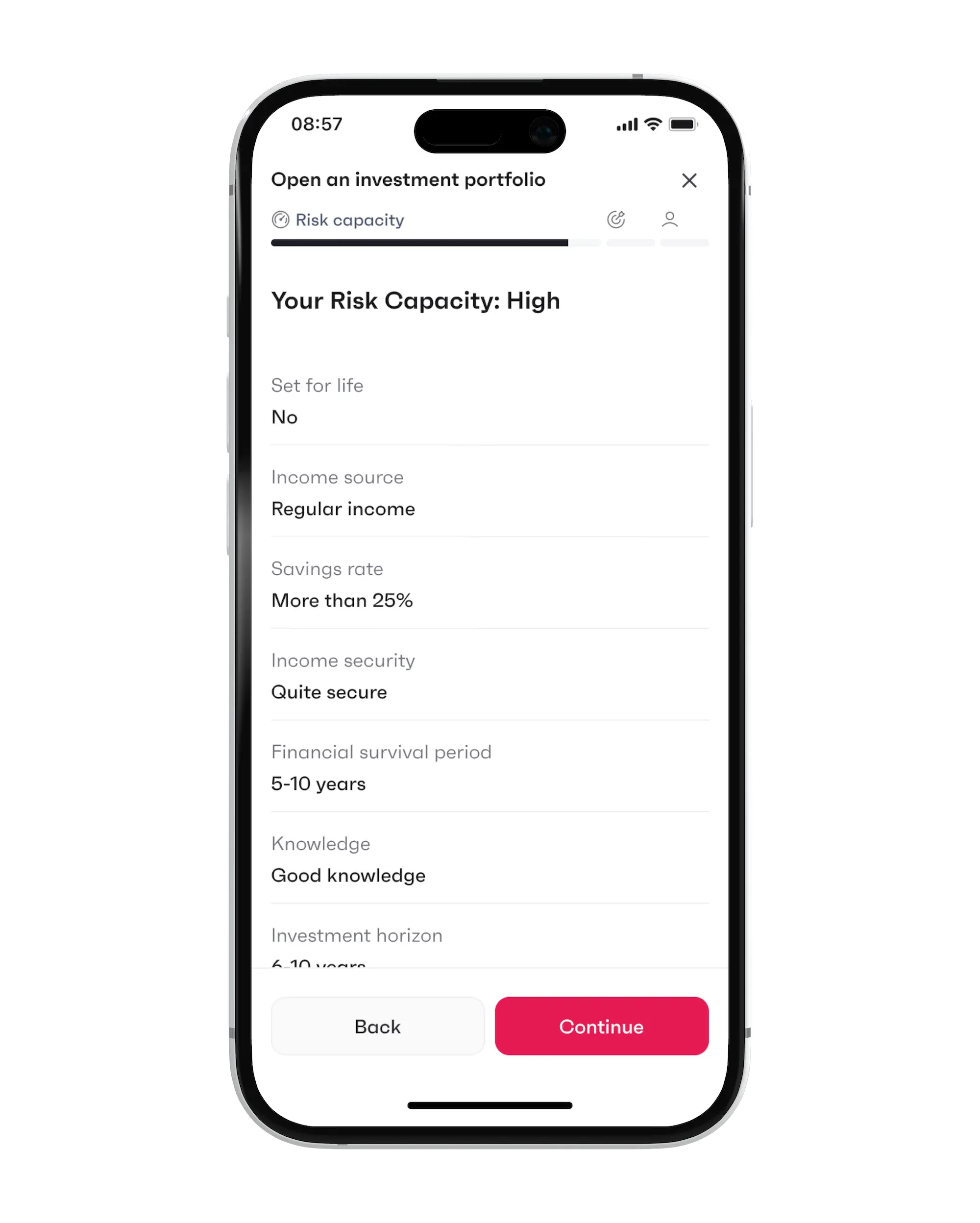

- Risk profile (a few questions to define your risk capacity)

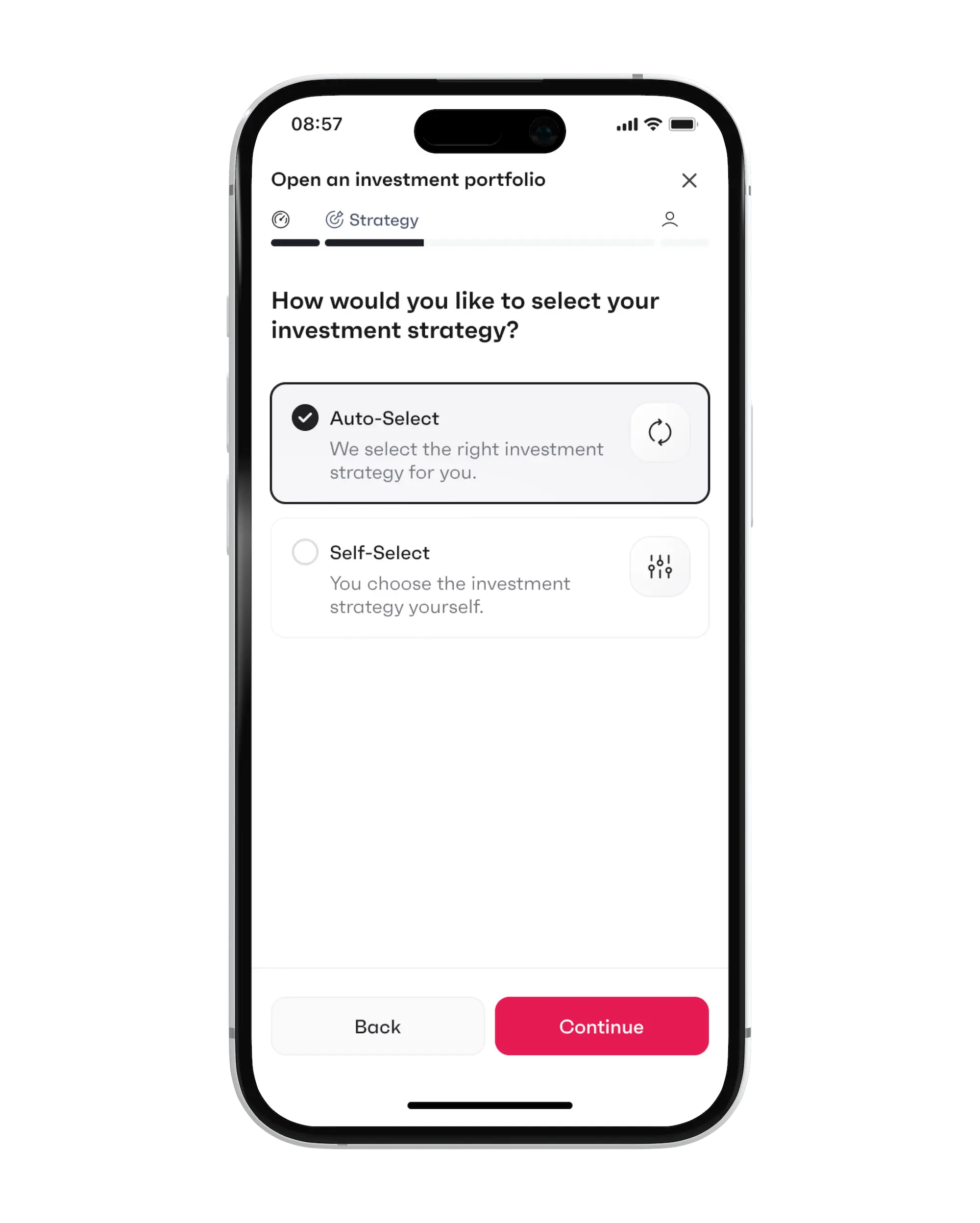

- Strategy (you pick your investment strategy, or you let finpension pick it for you)

- Personal details

I took a few screenshots below to give you an idea of the finpension Invest sign-up process.

Choose how to define your strategy: Auto-Select (finpension picks for you) or Self-Select (you pick yourself)

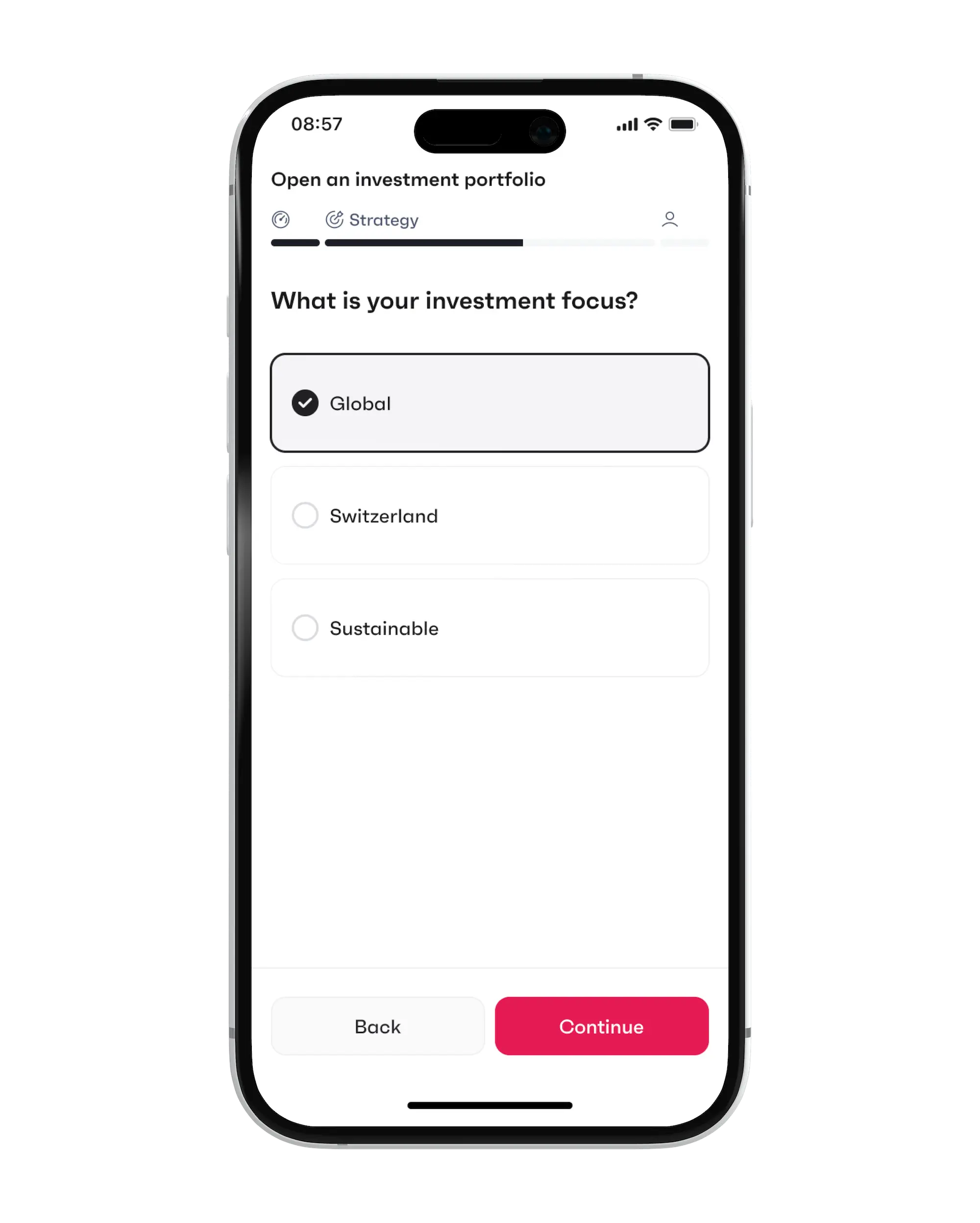

Choose your investment focus: Global, Switzerland or Sustainable (for us Mustachians, it's 'Global' to maximize the risk/return ratio)

And that’s it, all that’s left to do is make your first transfer to your finpension Invest portfolio.

Conclusion

finpension Invest is the best robo-advisor in Switzerland thanks to its low (and transparent!) fees, as well as its strategies designed for your net return (not theirs).

With nearly identical fees to VIAC Invest, finpension Invest takes the lead on your net return, and it comes down to two layers:

- The fund domicile (automatic gain, for everyone): finpension’s Irish ETFs only lose 15% of US withholding tax, against ~30% for VIAC’s Swiss funds. This advantage applies by default, without doing anything, whatever your canton or the size of your portfolio.

- The DA-1 form (bonus): you claim back the remaining 15% to get down to 0% lost, which brings the advantage to ~0.30% per year according to finpension. Two caveats though: it requires at least CHF 100 of recoverable withholding tax per year (below that, the tax administration won’t process the claim), and this reclaim on finpension’s reporting isn’t validated by the cantonal tax authorities yet (a court case is pending; finpension is confident it would hold up, but can’t guarantee it).

In other words: finpension wins by default thanks to the Irish fund domicile (automatic, guaranteed), and would win clearly if the DA-1 reclaim goes through (likely, but not yet validated by the tax authorities). That’s why I rank finpension Invest in first place today for a Mustachian investing in 100% global stocks over the long term (and who isn’t ready for DIY investing yet).

The finpension promo code below gives you a CHF 25 fee credit (provided you transfer or deposit at least CHF 1'000 within the first 12 months after creating your finpension account). For now, this code can only be entered by new finpension sign-ups; the option to reuse it for finpension Invest if you already used it for your 3a is coming during the summer.

===> MUSTBC <===

finpension Invest FAQ

Which strategies are available at finpension Invest?

Like with finpension 3a, there are 3 investment focuses: Global, Switzerland, and Sustainable.

And for each of these focuses, you can adjust the stock allocation, from the most cautious to the most aggressive, all the way up to the “finpension Equity 100” strategy (which is what I would pick myself, with the “Global” focus).

With Self-Select, you unlock even more options (a Europe focus, and the sustainable variants Broad Impact, Climate Impact, and Social Impact), plus the ability to build your portfolio from over 40 funds, or even access private markets.

As usual, you can actually only invest up to 99% in securities, because finpension always keeps 1% in cash to debit its fees.

Auto-Select or Self-Select: which one should you pick?

With Auto-Select, finpension picks the investment strategy matching your risk profile for you. You can also adjust this choice while sticking to the pre-built portfolios (Equity 20, Equity 60, etc.)

With Self-Select, you build your own portfolio at the level of the ETFs themselves.

To get started, Auto-Select is perfect. And the day you’re ready to go further (i.e. use Self-Select), it means you’re ready to go DIY (so you will probably never use the Self-Select mode).

How many finpension Invest portfolios can you open?

You can open up to 10 investment portfolios at finpension Invest, each with its own strategy.

Who can open a finpension Invest account?

finpension Invest is reserved for Swiss residents, at least 18 years old, who are not US taxpayers (US persons).

Can I create a finpension Invest portfolio for my kids?

Yes, you can use one (or several) portfolio(s) for each of your children. Note that the account stays in your name. And you will be able to transfer these assets to your kids once they reach legal age. So it’s a “virtual” solution for children.

As I already explained on the blog in my article “How to invest for your children”, I think it’s a great way of doing things. Because when you create an account directly in your child’s name (which isn’t possible with finpension Invest anyway), the financial institution can quickly become a pain the day you want to switch providers, because you no longer have control over the assets as they belong to your kids. And you have to prove all kinds of things to get it done. No thanks!

Is finpension Invest tax-optimized?

Yes, and that’s precisely its main advantage over VIAC Invest.

finpension Invest uses Irish ETFs: the withholding tax on US dividends drops from 30% to 15% (this part is automatic), and you can even claim back these 15% via the DA-1 form (lump-sum tax credit) to get down to 0% (from CHF 100 of recoverable withholding tax). This optimization is worth about 0.30% of performance per year. Heads up though: the DA-1 reclaim on finpension’s reporting isn’t yet validated by the cantonal tax authorities (a court case is pending; finpension is confident but can’t guarantee it). On the other hand, VIAC Invest uses Swiss funds, less optimized on this point and with no DA-1 form possible.

Over the long term, this detail improves your net return.

Can I let cash sit at finpension Invest?

No, unlike VIAC, finpension Invest doesn’t offer a 100% cash option (and by the way, VIAC no longer pays interest on that cash: 0.00% as of today). But you can park the defensive part of your portfolio in a money market fund, which comes down to the same thing in practice.

Where is the money I invest at finpension Invest held?

Since finpension is registered as a securities firm with FINMA, it holds your securities itself, without going through a third-party custodian bank.

Your uninvested cash is protected up to CHF 100'000. And your securities are segregated from finpension’s own assets: in case of bankruptcy, they would be transferred to another custodian bank, so they are protected.

How do I withdraw money from finpension Invest?

You can have your money paid out to your (previously verified) reference bank account. Transfers to third-party accounts are not allowed.

You can even schedule a withdrawal plan to receive a fixed amount every month (finpension then automatically sells just enough shares), handy to live off your capital once financially independent.

finpension Invest or VIAC Invest?

Both are excellent robo-advisors with nearly identical fees (as of June 2026, for Global 100: VIAC 0.46%, finpension 0.47%). In 2026, I rank finpension Invest slightly ahead thanks to its optimization of the US withholding tax (its Irish ETFs automatically halve it, plus a potential ~0.30%/year via the DA-1 form, a reclaim finpension is confident about but that the cantonal tax authorities haven’t validated yet). VIAC keeps a fee-free cash option, and avoids the stamp duty through its in-house funds (though those carry higher spread costs, so the net result is comparable).

finpension Invest or finpension 3a: are they the same thing?

No. finpension 3a is a third pillar (= retirement savings, with tax deductions; and that money is locked until retirement). finpension Invest, on the other hand, is for investing your free savings, with no lock-up. Ideally, you first max out your 3a to benefit from the tax savings, then invest the rest via finpension Invest or DIY-style.

finpension Invest or neon Invest?

Making that comparison is like comparing apples and oranges: neon Invest is not a robo-advisor, it’s a trading platform. You buy your ETFs and stocks yourself, with no automated management.

And what about the “portfolio templates” neon has launched since? neon says so themselves: no regulatory risk profile, no automatic rebalancing, no management. It’s a ready-made ETF “shopping list” that you then have to manage yourself.

So the real question is where you stand on the ladder of the stock market investor: if you want full autopilot, go with finpension Invest. If you’re ready to manage your own portfolio, then you will find cheaper online trading platforms than neon Invest (see my article: Best broker in Switzerland (comparison 2026)).

finpension Invest or Interactive Brokers (IBKR)?

Apples and oranges: finpension Invest is a robo-advisor (automated management), whereas buying VT (the famous “buy and hold”) on Interactive Brokers is DIY (you manage it yourself). So they’re complementary, not competitors.

On fees, VT on IBKR is unbeatable: it’s the top rung of the ladder of the stock market investor. But cheapest doesn’t mean best for you today: if you don’t dare manage your own portfolio yet (and hold steady through a crash), finpension Invest is the perfect intermediate step before going DIY.

And the day you take that step, you save thousands, even hundreds of thousands of CHF in fees over the long term (I did the math for you: investing yourself vs robo-advisor).