Mustachian Post (aka Marc Pittet) - FIRE through frugalism on Mustachian Post (aka Marc Pittet) - FIRE through frugalismhttps://www.mustachianpost.com/2025-04-25T06:51:04+00:00The bus stop2025-04-24T02:27:00+00:002025-04-24T02:27:00+00:00MPtag:www.mustachianpost.com,2025-04-24:/blog/the-bus-stop/A bus stop, a forest on the other side of the road… and a dream of freedom. My anchor to FIRE, between routine and independence.Today is going to be a tough day. There’s that difficult meeting I don’t want to attend. A part of my work I don’t enjoy. A task my boss asked me to do, and I don’t even see the point of it. That colleague I can’t stand, but still have to collaborate with… for two hours straight.

And there I am, at this bus stop. And just across the street, there’s a forest. A forest that seems to call me every morning.

And whenever I’m in such a situation, I imagine that day.

That day, I’ll still be at that stop, dressed like I’m heading to work, laptop bag in hand. But this time, I won’t get on the bus. I’ll watch it drive away, then cross the road, and walk toward the forest.

Just for a short one-hour walk. And maybe, before I even realize it, it’ll already be noon. Or 6pm. Who knows.

Realize what? That I did it! I’m financially independent.

I’ve played out that scene in my head so many times. Over and over again. That bus stop has become my crossroads. My turning point. Neo’s red pill.

One day, I’ll take the other path.

And until then, I use this anchor to stay the course toward my long-term goal. My FIRE. My freedom. My real life.

What’s your bus stop? The one that you pass by every day… and one day will watch you head off toward freedom?

]]>9 hypotheke.ch reviews for your Swiss mortgage2025-04-17T02:27:00+00:002025-04-17T02:27:00+00:00MPtag:www.mustachianpost.com,2025-04-17:/blog/hypotheke-review/Is the Hypotheke.ch service really worth it, rather than searching for a mortgage yourself? Here are 9 unfiltered reviews to help you decide!When I wrote my article on how to find the best mortgage, several of you mentioned the online solution Hypotheke.ch for comparing and taking out a mortgage online (with the best interest rates).

This prompted me to survey all the blog’s readers in order to find out if this was a recommendable solution.

Here are all the responses I received, as well as my conclusion at the end of the article — as well as a special Hypotheke.ch promo code for blog readers.

😃 Daniel D.

I’m of the opinion that the provider Hypotheke.ch is one of the best in Switzerland.

I always look at their homepage when I want to get an idea of the current offers. My subjective opinion is that this provider is one of the most independent in the sector. The majority of the other comparison sites are linked to a provider (insurance or bank).

I had a telephone call with one of the Hypotheke.ch team around 3 years ago (unfortunately I can’t remember his name, it might have been Mr Schubiger).

At the time, we were looking to remortgage with UBS.

We had an offer from UBS with a 0.6% margin for a Saron mortgage, so the Saron rate & then the bank margin of 0.6% on top.

I had briefly explained our financial situation over the telephone, the mortgage amount, etc. He immediately explained to me over the telephone that he believed that this was a very good offer and that I should accept the UBS offer. Which we did.

For me, this contact was very positive. We must have spent 20 minutes and more on the telephone, he listened to me quietly, asked me some questions and gave me his evaluation. It is highly likely that another provider would have immediately invited me to an appointment and then tried to “sell” me their service.

It is very likely that I’ll get back in contact with the provider if we want to remortgage in the future.

🙂 Jakub W.

I was looking for a mortgage in October/November 2024 and I decided to use MoneyPark and hypotheke.ch at the same time.

Overall, it was a good experience — communication was fast and professional, and they offered good rates from Migros Bank.

Unfortunately, I think they lacked a bit of flexibility and the capacity to manage more complex cases like mine — I already have a mortgage, and different banks interpret this in different ways (in terms of debt burden and income).

In the end, they weren’t able to get me a suitable offer and I went with MoneyPark and UBS.

😃 Lukas S.

I took out my mortgage with Hypotheke and I can confirm that it’s a very good service.

Here’s an overview of my experience:

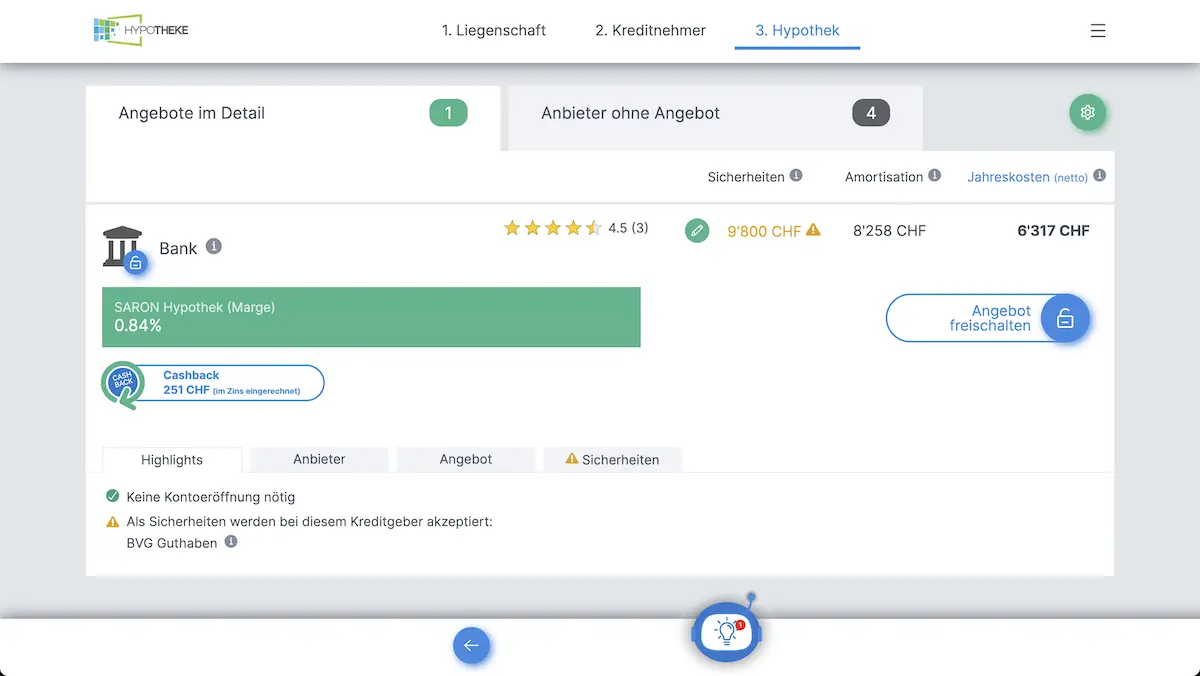

Conditions: SARON with a margin of 0,49%. It’s the best offer I could find on the internet, and they also offered me this rate without any issues.

Online process: The process is based on an entirely automated work flow in which several pieces of information must be provided. This does require some effort, but is in line with what is required by other brokers.

Support and completion: Once you’ve submitted most of the documents, they contact you and complete the formalities with you. The transfer from the old bank to the new one went smoothly without any issues.

In my case, everything went perfectly and I can definitely recommend them. I worked with MoneyPark for my in-laws’ mortgage a year earlier, which was also a very good experience. I’d say the two are as good as each other.

MP:“It’s interesting what you say about MoneyPark, as other readers have been a lot less positive since they were bought by Helvetia. MoneyPark or Hypotheke.ch, do you really view these two companies as comparable?”

The commercial model of Hypotheke.ch seems to be that they have agreements with companies who want to outsource searching for new customers. I ended up with Bank EKI, a cooperative bank which is very small, and which only has two branches. Hypotheke.ch appear to have an agreement with them to offer very good conditions in exchange for exclusivity over searching for customers for them.

Moneypark is different in this context. They have different partners, but seem to work on a non-exclusive basis. This was really good for my in-laws’ case, as the advisor looked for the best conditions based on their very specific situation. I think we were lucky with this, as the advisor we worked with was very customer-focused and probably sometimes even willing to make an additional effort above what was required of them from the company’s perspective. In short, I wouldn’t expect that to be the norm with Moneypark.

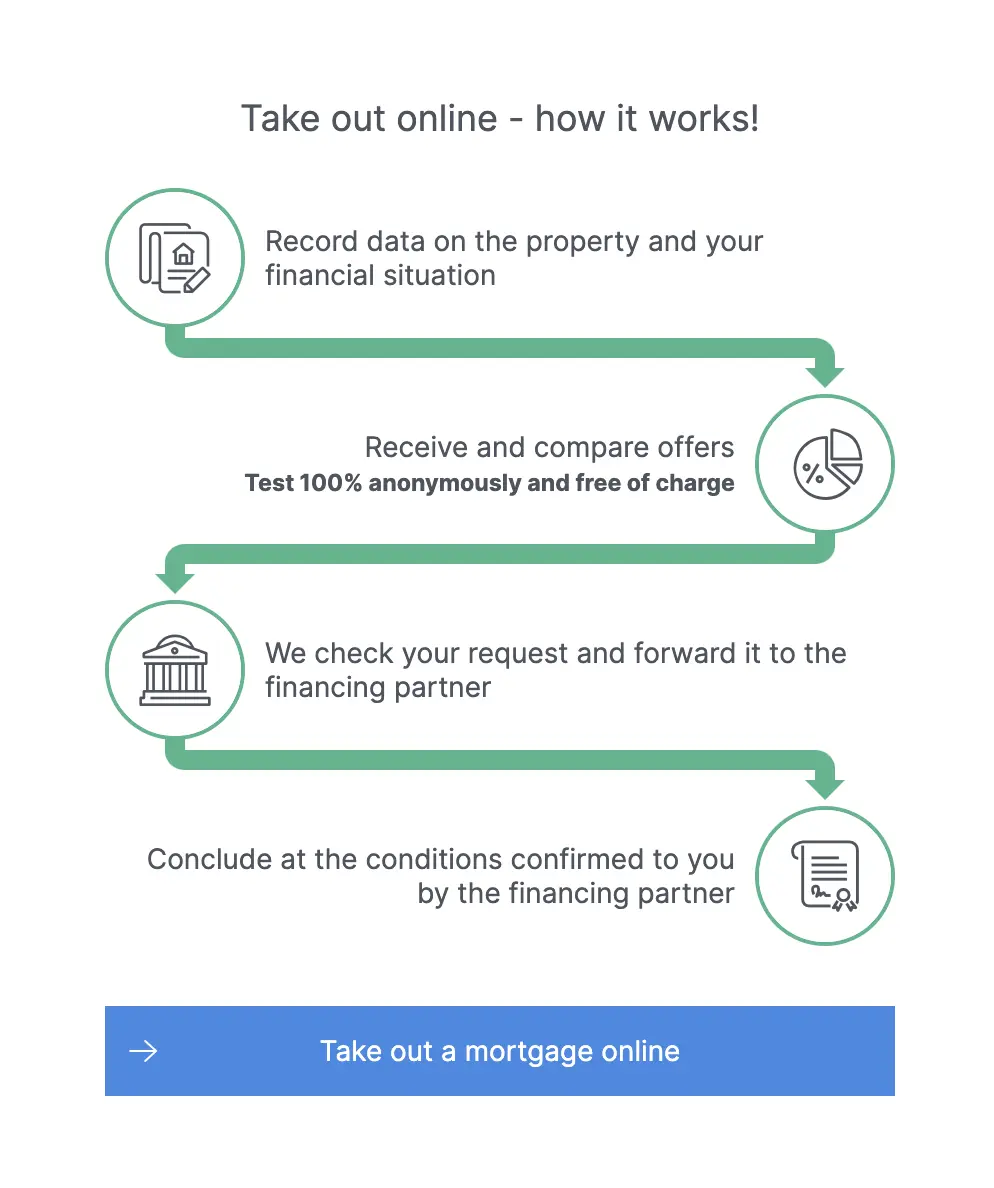

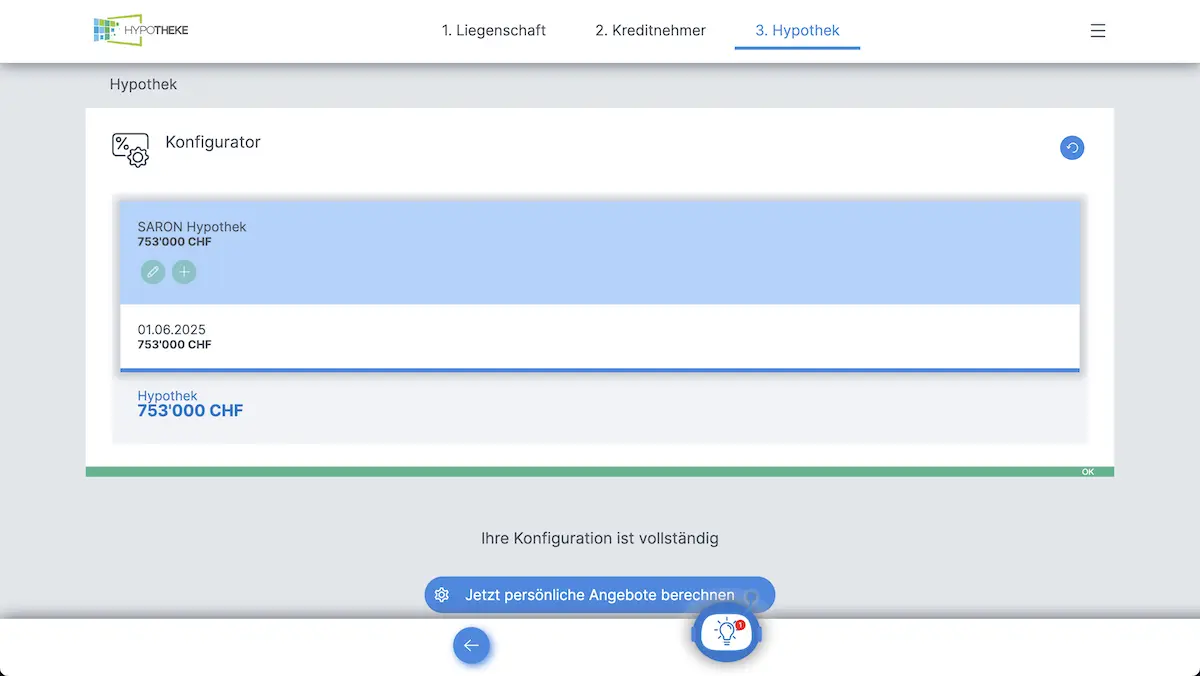

How the Hypotheke.ch service works in 3 simple steps

🤷♂️ SB

I’m sharing my notes with you from my contact with hypotheke.ch (Michael Bader), in May 2024:

They are fairly active in German-speaking Switzerland.

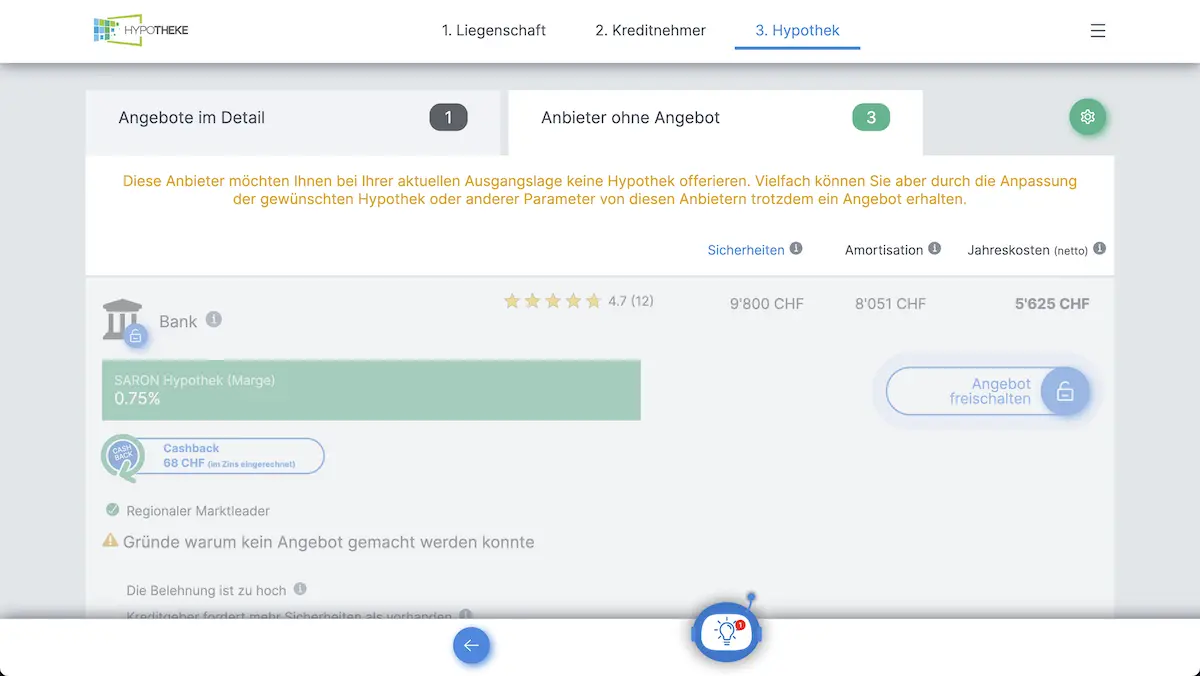

It’s not currently possible to get a mortgage offer for a rental investment building: but this should change in the coming weeks.

At best they could perhaps obtain -0.1% on SARON and -0.2% fixed.

By Mr Bader’s own admission, it’s not worth changing because the gain would only be around CHF 100 per month maximum for the debt of CHF 500'000.

In addition, the change isn’t free: you need loads of documents, some of which require you to pay a fee to obtain them.

I should point out that my situation is somewhat unique with firstly a villa of 3 apartments in Montreux, which had to be remortgaged before my main residence in Fribourg. Hypotheke.ch wasn’t particularly interested in financing the rental property in Montreux…

I also looked into using VZ, but what annoyed me with them is that there were also intermediaries (internal) and they required powers of attorney to be signed. As I don’t really like giving up control, particularly at this level, I didn’t pursue this route.

As a public worker, BCBE’s offering for Publica policyholders is much more beneficial for me. Offer applicable to members of the APC – BCBE.

😃 Petra G.

Yes, I took out a mortgage with hypotheke.ch, and I’m very satisfied with them!

I read a review of hypotheke.ch in the Tages-Anzeiger.

I needed to remortgage in 2021. I registered with hypotheke.ch, I looked at their offers and I accepted one: mortgage from SGPK (St.Galler Pensionskasse) over 10 years at 0.65%.

I’d never have found it by myself, as I didn’t know that pension funds also provided mortgages.

It's not very well known that pension funds provide mortgages

😃 André G.

I remortgaged with this platform.

I have nothing negative to say.

Twice with no problems and fast.

It’s also possible to call Hypotheke advisors to clarify any questions.

😃 Manuela H.

Yes, I had a good experience with hypotheke.ch (but I ended up going with another provider).

Hypotheke.ch is without doubt a very good provider. Depending on your situation, you can get better offers elsewhere as hypotheke.ch is entirely automated (and therefore is less able to adapt to your specific needs).

From what I understood, one of their founders was previously at VZ Vermögenszentrum, and, together with an IT-savvy cofounder, they’ve built a web platform capable of automatically generating mortgage loan offers.

Their business model consists of offering users an easy-to-use platform for uploading all the necessary documents, and providing them with an immediate response confirming whether they meet the requirements of one of the providers in their network based on the information provided. Their involvement is minimal, but if you contact them by telephone (they’re really nice), they can help you and know exactly what you need to change in order to meet the minimum criteria of an offer. They also have some pension funds in their network which are not included/available with other brokers.

However, if you have specific/additional collateral (for example: an apartment already owned with another mortgage tranche), they have limited room for maneuver to make changes or reflect that in one way or another in their offer. I get the impression that a customer advisor in a bank or insurance company has more room to adapt the offer to your needs in this specific case. Overall, I liked the hypoteke.ch team and I recommend them to my friends.

What I’m not sure about: the time when you search for a financial partner and the point at which you fix the mortgage rate can be very different (in my case, the difference was 6 months), and it was obviously advantageous for me to wait as long as possible to fix due to the expected decisions by the BNS. I’m not sure that they (or their partner) are very flexible when it comes to adjusting/lowering the rate up to the day of fixing.

What is sure is that Hypotheke.ch is definitely better than the big competitors (Moneypark now belongs to Helvetia), as they try to understand your situation and help you as best they can to obtain the best offer they can get for you.

In summary: they are undeniably good with competitive rates, an efficient online procedure and a great team. It’s only if you have specific requirements for bespoke solutions that there can be competitors to take into consideration.

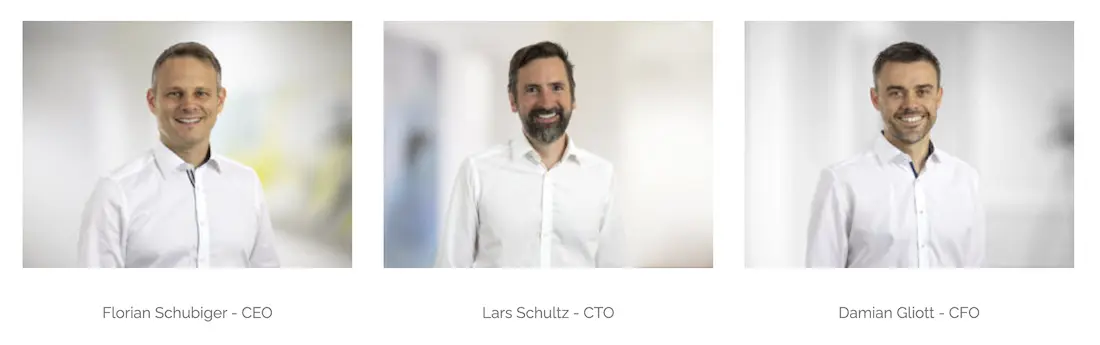

The founding team behind Hypotheke.ch

😃 John Galt

My bank (UBS) initially gave me a ridiculous rate despite me having been a good customer for 9 years!

I therefore used Hypotheke.ch and my friend has too over the past three months. I received very good support and offers which had no initial fees or obligations. Claudio was also able to negotiate the conditions after the first offer was approved, when my bank woke up and made a competitive offer in order to keep us — but the bank found by Hypotheke.ch made us an even better offer!

Verdict: I highly recommend Hypotheke.ch.

😃 Friedrich M.

I took out a mortgage through their intermediary at the end of last year, and I must say that I’m very satisfied with their service.

The central service worked very well.

How the Hypotheke.ch service works

It’s very quick and easy to get real mortgage proposals:

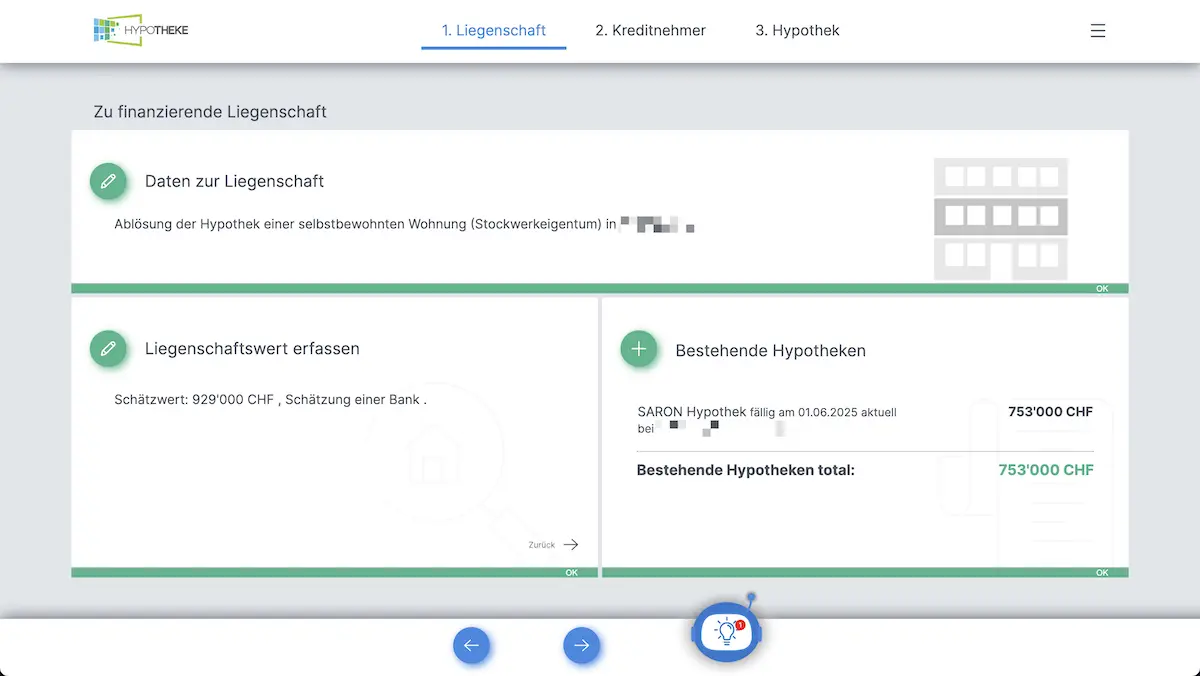

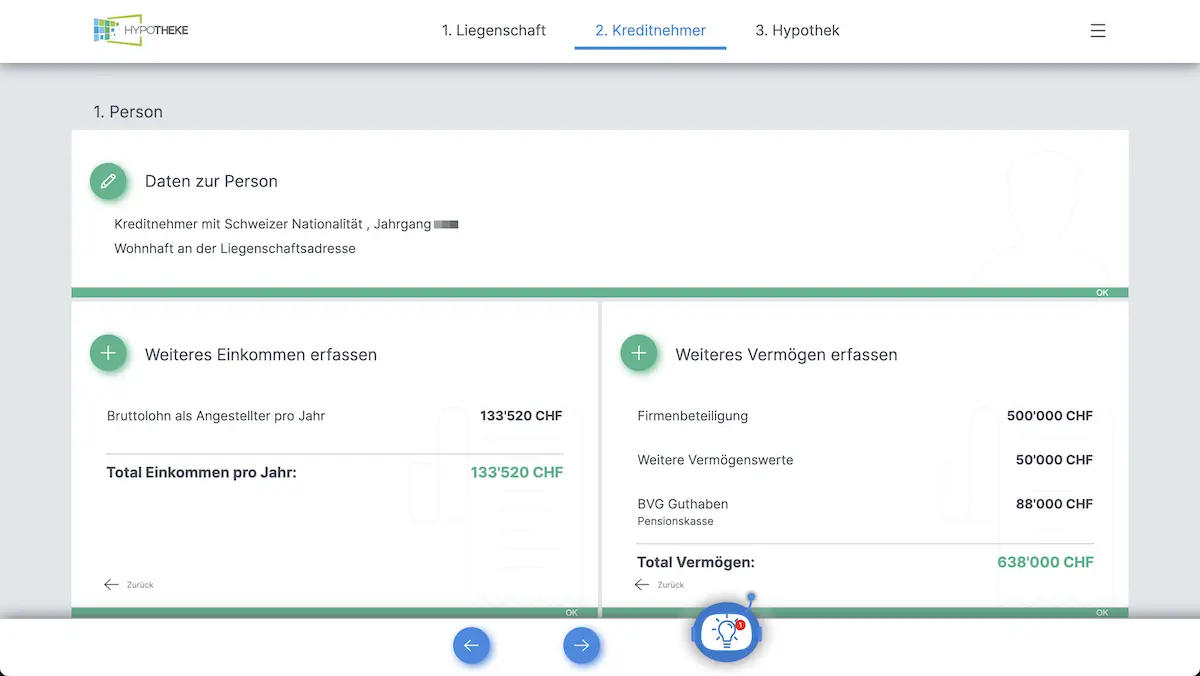

Fill in your personal information and details of your property in Switzerland

Input your income and the value of your assets in Switzerland

Configure how you want to structure your mortgage

In this tab, I've got the mortgage proposals that come through without changing my parameters

In this other tab, I've got mortgage proposals that will come through if I change certain parameters (I can also call Hypotheke.ch to ask them for help in real time)

The user experience is very straightforward and efficient. I’d prefer a design that’s a bit more modern but, in the end, for taking out a mortgage or remortgaging once every X years, that’s a minor detail.

MP conclusion regarding using Hypotheke.ch for your mortgage in Switzerland

Frankly, I’m amazed to have received so many positive, even very positive, opinions.

Let’s be honest: as a Mustachian, we’re demanding and meticulous when it comes to anything related to personal finance.

I hope that the Hypotheke.ch team will be able to manage its growth, while maintaining this level of customer service. But in fact, I believe that this mindset comes from the cofounders, who have a long-term vision (rather than short-term in wanting to sign contracts at any cost). I like that!

I also really liked it when Lars Schultz (their CTO and one of the three cofounders) told me when we were chatting about the English version of their site:

I personally like our service, as we can talk freely about (almost) everything with our customers, as we work hard to ensure that everyone (the customer, the mortgage broker, and us) gets treated fairly.

If I had to remortgage today, I’d request a proposal for a SARON mortgage from:

Hypotheke.ch special code: You can specify the code "MPHYPO" to the Hypotheke operator when you take out your mortgage. This will entitle you to an additional cashback of CHF 100. And the blog will also earn a small commission in the process, for which I thank you.

FAQ Hypotheke.ch

Is it possible to use a 100% stocks 3a pillar for indirect amortization?

The majority of non-bank lenders accept this type of collateral, i.e. pension funds, investment foundations and insurance companies.

However, they won’t take 100% of the value of this type of 3a pillar into consideration, due to the risk inherent in stocks portfolios. Therefore, if you have CHF 100'000 in your VIAC or finpension account, some lenders will only count it as 60 or 80'000 CHF for collateral.

How does Hypotheke.ch make money? What do I have to pay as a customer?

For a standard case, Hypotheke.ch customers don’t generally have to pay anything, as the broker’s commission usually covers all their expenses and fees.

In almost all the cases they’ve had up to now, the customer even receives cashback on top (in cash, paid directly into your bank account). This cashback is communicated transparently in their tool, even before the customer provides their email address.

The way they work is very simple: they calculate the fees for each case, based on the mortgage amount and the duration of the contract, in the same way as most mortgage brokers calculate their commission, except that their fees are a bit lower.

As their fees are always calculated in the same way, where the mortgage is taken out is irrelevant to them.

Then, the customer receives the difference between the commission and Hypotheke.ch’s fees in the form of cashback. If this ends up being nothing or if the fees are higher than the commission, the customer will have to pay the remaining fees, but they are usually practically zero.

The cashback or the remaining fees are always clearly indicated before the customer chooses an offer.

The only situation in which they request (partial) fees is if the customer withdraws after a clearly communicated stage, which is quite late in the process.

Why would banks and other institutions want to work with Hypotheke.ch?

The mortgage lenders on the platform also benefit from their unique process because, in general, they only submit an application to the one lender chosen by the customer.

This is contrary to the traditional process, which consists of submitting an application to several lenders with the intention of obtaining an offer from each of them, which only one of them will end up having accepted.

The application is checked and complete, ready to be signed off by the lender, as the Hypotheke.ch teams have already checked that the application fulfils the lender’s criteria.

They told me they have a very high conversion rate for applications submitted to their lenders, as they check the information given by their customers against the official documents provided in support.

Is Hypotheke.ch available in French?

Unfortunately, they don’t currently have the necessary resources to be able to offer their services in French.

It’s obviously on their to-do list, but up to now, they haven’t had the time to do it and as they’re a small company, they really need to concentrate on their core work.

But they are aiming to provide multilingual support during the coming year (2025). English should be fine on the telephone with their advisors, but their online content has not yet been fully translated.

Do I have access to all the offers without having to pay?

Their mortgage rates are calculated instantly for more than 30 mortgage brokers, so the customer is always able to choose the best offer, and everything, except the name of the mortgage broker, is available for the customer while remaining anonymous.

In order to communicate the names of the mortgage brokers linked to the offers, they request the customer to identify themselves by providing and confirming a mobile telephone number.

How long has the Hypotheke.ch service existed?

They started developing their app in 2016, and founded the company in January 2019.

]]>53 and Financially Free: let the dream begin2025-04-03T02:27:00+00:002025-04-03T02:27:00+00:00MPtag:www.mustachianpost.com,2025-04-03:/blog/53-and-financially-free/Becky was lucky to have a strong financial education by her father. But concrete action was what made her success, and enabled her to retire early by 53 in Switzerland.Concrete stories of Swiss folks who succeeded to early retire was one of the thing I missed when I started my financial independence journey back in 2013.

I’m glad to have persisted with the blog over the past 11 years, as I start to get more and more of them from readers.

The keyboard is yours Becky.

Hey Marc! I feel like I am still floating as if in a dream… but let me introduce myself before I share what happened.

(By the way, the header photo above was taken on the 1st day I was FIRE, at Lake Staz near Saint-Moritz!)

I’m Becky, and here is my background

I live in Switzerland on the shores of Lake Zurich. I grew up in the US, and spent about half my adult life so far there, then came to Switzerland 17 years ago (in 2008).

The original plan was to be in Switzerland for only 3 years! But the natural beauty and endless opportunities for outdoor adventures made it clear to me that this is a great place to stay.

Luckily, I was able to quickly find a job here at a global reinsurance company in Zurich to make it possible to stay. Even though it was right in the middle of a financial crisis (in 2009), they needed more people at the time with my background (risk management). My university degree is in mathematical statistics, and I trained in the US and worked as an actuary, which involves applying quantitative analysis and long-term projections to address financial questions – or as I like to say:

Using mathematical logic to solve finance-related puzzles.

Working as an actuary is quite a good career in many ways including financially, providing a stable income, plus the training was all financed by my employers, so I never had to be weighed down by financial loans for my additional studies.

It’s also a very interesting career, which is a nice combination of analysis and communication, as a big part of my job included providing training and other sessions to explain complicated technical items in an understandable way.

After 30 years of working as an actuary in the financial industry, I decided to leave the corporate world. It wasn’t an easy decision since I had a good job at a good company with great colleagues. But I decided I wanted more time to do the things I love with the people I choose to do them with, and to move into a phase of doing different kinds of projects.

I’m 53 years old (“Fifty-three and financially free” has a nice ring to it doesn’t it!) and live together with my partner who is Swiss.

He is 65 and recently retired.

We enjoy doing a multitude of activities together in the great outdoors, including hiking, biking, running, kayaking, snow sports, and climbing/via ferrata. We are active in a local choir where I play piano as accompanist and we both sing, and we are also active in the local community volunteer activities. He has six grandchildren, and as they get older we enjoy taking them on various adventures as well.

Our music choir where I play piano

My father lost his job… and taught me an invaluable lesson!

When I was in high school, my father lost his job and we thought we might have to move to a different city, which I was quite sad about since I was very active in the band and other music groups in my school.

Luckily, he got a job with a company that trained him to work with clients about investing, and he taught me then what he learned – including the general motto to “Pay yourself first”, i.e. set aside money for investing before spending it, and investing in diversified, low-cost index funds with long-term perspective.

I am very thankful that he taught me these important fundamentals when I was at such a young age!

When I started working, I immediately applied this saving and investing approach, and I also maximised all employer-provided benefits. In the U.S. there are typically no pension funds like in Switzerland, just mainly some tax-deferred savings plans where the employer would sometimes match a portion, and which we needed to invest our savings ourselves each time we changed jobs.

To invest it, I just followed the structure I learned from my father; that is, buy low-cost index funds with a high-risk tolerance since it’s for the long-term, and then leave it alone. I didn’t even look at my brokerage account balance – just kept adding to it whenever I could.

My money goal was always to be financially independent and not to have to rely on my parents or anyone else.

I just knew I wanted to have options.

I had a scholarship for my university studies, and I worked as a math tutor to earn spending money. I started working in a corporate job as soon as I could after university so that I could start saving and investing, with the main goal being that I could make my own decisions on how to spend my money even if my parents disagreed with my decisions. This was very empowering at the young age of 22!

It was basically engrained in my mind that I need to save for myself since the government will not be providing for me.

And if for some reason I lost my job like what happened to my father, I wanted to have options and not to have to make changes I wouldn’t want to make just for a new job.

I thought I might want to take a break from corporate work at some point, perhaps a sabbatical, or possibly to work part-time, or maybe even to change into a different kind of work that would interest me in a different way but might earn less. I didn’t really know what exactly my long-term goal was, I just knew I wanted to have options.

Travels and struggles to invest as a US citizen

Even though my goal was to maximise savings and investments, I also knew it’s important to enjoy life in the current moment, especially since we never know what might happen in the future.

Maybe we’re not healthy enough by the time we retire to even enjoy the money we’ve saved.

It doesn’t make sense to be so frugal that we save everything for some future time at the expense of any enjoyment now. A continual challenge is finding the right balance for saving vs living now.

I love being above the fog on a weekday hike ;)

Luckily, I never was a shopper or had expensive hobbies like collecting cars or something like that — I have a lot of hobbies which don’t cost a lot of money, including hiking, biking, or playing music.

There are so many amazing things one can do, especially here in Switzerland in the great outdoors, that don’t require a lot of money. (As MP says/writes so well, “The best things in life are free”!)

I’ve also done a lot of traveling all around the world and experienced a lot of things such as climbing Mt Kilimanjaro or hiking in Patagonia and Alaska… Even though it has reduced the amount of money I could save, I don’t regret it at all as the experiences are priceless.

[…] the long-term growth made up for a lot of the challenges.

For me, as an American living and working overseas, another struggle has been sorting through the financial requirements and limitations. When I wanted to invest, I had to send the money from what I earned from my job here in Switzerland to the U.S. to be allowed to invest in index funds for many years. Luckily there is a large choice of good low-cost investments there (such as Vanguard) so the long-term growth made up for a lot of the challenges.

Once I was able to invest in Switzerland 1, I had a lot to learn about the different investment options including brokerage firms, how to find the best available ETFs, and the different tax optimising strategies available here. Even though it has taken quite some time and energy, I really enjoy learning about these different topics. If I had learned about the MP site earlier, it could have possibly helped me go into FIRE even sooner!

And then the decision to actually become FIRE

The big trigger that led to me finally doing it – to become FIRE (or on fire as I like to say 😊) – was when my partner retired in March this year.

He’s 12 years older than me, so I knew it would happen at some point, but I didn’t expect the feeling it would create would have such a strong impact on me.

Before he retired, we were both working and had a similar daily rhythm. After his retirement, that all changed, when suddenly his time was free, and he could choose how to spend it. Of course this made me quite jealous! He would be planning a hike with friends on a nice sunny weekday, when the weather was perfect, while I had to go into the office for a day full of meetings. I realised I really wanted to have more freedom to determine how to spend my time as well.

What a freedom feeling! (Day 2 of FIRE — Hiking Bernina Tour trail above Lake Diavolezza in Engadin)

Also ever since the COVID years — a time when many of us were contemplating the meaning of life and work — I’d been wanting to try some different kinds of work that I felt were important to me. As is often the case, these alternative paths would not provide such a financial stability as I had enjoyed from the corporate work, but nonetheless I felt the inner push to take the leap and give it a try.

These feelings motivated me to fine-tune my analysis of my personal finances to better clarify how much I have and how much I need. I had heard of the 4% rule many times, but I had never really focused on it for myself until now – I had just focused on “save as much as possible” while still living a good life.

I updated and enhanced my spreadsheets and ran a few different scenarios.

I updated my budget and clarified my cashflow needs, including buffers for unknowns and future changes (just as I would do in my actuarial work 😊), and compared it to my total asset balance. And lo and behold, it confirmed I had reached (or exceeded) the 4% rule. What an exciting feeling!

It confirmed I had reached (or exceeded) the 4% rule!

This confirmed my decision to leave my corporate job, so that I could have more freedom and flexibility to do the things I want, as well as to pursue some different types of work that are important to me and make me feel I can make a difference. Even if the new work and activities do not earn nearly as much as my previous job, it is a good feeling to know my cashflow needs are covered by my investments.

Fine tuning my finances before taking the plunge

I have applied the Do It Yourself approach to investing, i.e. investing it myself via an online brokerage company into low-cost index funds or ETFs.

I did it this way since it saves money by avoiding high banker fees, plus I like doing these kinds of things myself. Honestly, at first, when I was in my early twenties, it was quite scary to make my first investments myself online, but each time it got easier. I have always made sure to maximise tax-efficient options when feasible such as the pillar 3a.

Setup your investments, then forget about them and go cross-country skiing! (photo taken near Einsiedeln)

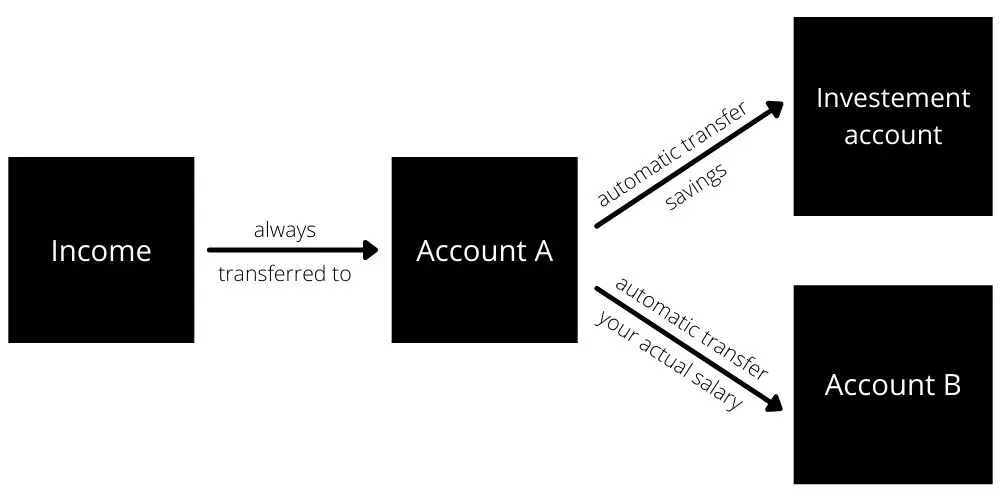

I have set up a “bucket system” 2 for myself so that I have cash bucket available for immediate and short-term needs, a medium-term investment bucket for mid-term needs, and most of it in the long-term investments.

As a rule, I do not look at my investment portfolio regularly. But I must admit after my first month of FIRE, I checked and totaled up my assets and compared them to the month before since I was curious 😊

The increase was very positive, so that was a good start! Of course, I know it will go up and down in the future and I am prepared for that.

I’m now 53, and financially free!

Life feels incredible!

I still wake up sometimes thinking it must be a dream. I love getting to decide how I spend my time each day, and in general I feel much calmer. I have so many activities which I like to do, so I still feel very busy – but in a positive way.

The topics are those close to my heart – e.g. music, volunteering, helping in the community, as well as simply spending time in nature or riding my bike over the beautiful Swiss hillsides.

Biking in the Swiss mountains 🏔️

I still need to use my daily planner and other online tools, even more than when I was working, to organise and plan all my activities and coordinate schedules.

If I feel I’m too busy, it’s my own fault since it means I planned too much! I still have to say “No” to some things and make priorities since time is not limitless. And sometimes, we just decide spontaneously to go hiking in the mountains or in Ticino where it’s more often sunny, so it’s nice to keep time open for that.

I was already quite active with many volunteer activities, and now I’m thankful to have more time to spend on them. One of my favorite volunteer activities includes regularly bringing groceries to and spending time with a 90-year-old lady who lives alone.

I’m happy to have more time for music and planning things for our choir.

For a local club/association, I lead workouts as well as hikes in the mountains.

To me, it’s always been important to get active in the local community, especially as a foreigner coming into Switzerland who didn’t know anyone at the beginning. It takes an investment of time and energy to get integrated here, but it’s been worth it to me.

I love going into our village and seeing people I know or that know me – it makes it feel like home.

Have you seen my new office scenery?! (photo taken near Schönenberg)

One of my next projects is cleaning out closets/de-cluttering our home so that eventually we may be able to rent it out when we go for longer periods of travelling. We are planning some longer trips such as to Asia and the Americas, but also to spend some time in places in Europe including e.g. Italy to learn and practice Italian. From the cleaning up project, it’s a nice feeling to donate things that we no longer need and make space for this next chapter of life.

A few of the activities I do earn some small amounts of money, including organising and leading hikes in the mountains for clients. I also recently did a training course with my partner for coaching, and we’ve had a few sessions with clients already.

I have also started providing some financial coaching to women friends, to share the knowledge and experience I’ve built up in this important and fun topic over the years. I am grateful to have learned the important fundamentals from my father when I was young, and I am happy to help others to be able to experience how good it feels to have your money work for you over time. It is certainly worth it.

As I highlight to them, it’s never too late to start investing – the important thing is to simply do it!

Advice for those who want to become FIRE

If retiring (very) early is your goal, I’d recommend “transitioning” to FIRE if possible. That’s what I did, switching from a 100% to a 60% role in my company two years before I left.

It was a great way to “test” my freedom and use this time to optimize my portfolio, as well as to work on developing my “side activities” to move forward after the departure.

Conclusion

From a money perspective, my total amount of money is above (but not excessively) 25 times my annual expenses, so just above the 4% rule.

I feel fine with this for a few reasons including:

I’m earning some extra money from my side-gigs which are now officially my self-employment income

For everyone, I anyway think it’s important to keep doing things that earn a bit of money for a sense of contribution to society. Best is when it’s not required for living (as enough comes from the investments), but feels like extra pocket money

AHV and Social Security (US) are not included in this net worth computation

Apartment equity not included in my calculation neither, plus we’re planning to rent out our apartment when we travel for long periods

Expenses are so far lower than I previously projected, since I enjoy being a minimalist, more and more as time goes by!

I find it’s actually easier to spend less money than I was spending previously, because I’m doing things that are free (in the great outdoors) and make me feel calm and happy, which results in less “impulse” spending or buying things that I might have previously as a reward since I was working hard.

What do you do on Tuesday afternoons? (Hüttnersee in the canton of Zürich)

Now, more than four months after starting my FIRE experience, I can confidently say that I do not regret at all the decision to go for it. I sleep extremely better than I did beforehand! And even though my total accounts balance has gone up and down since end of October due to the market changes during that time, overall it is higher than when I started FIRE even after expenses, so it is a good start!

Notes from MP about Becky’s story

The important of financial education for kids

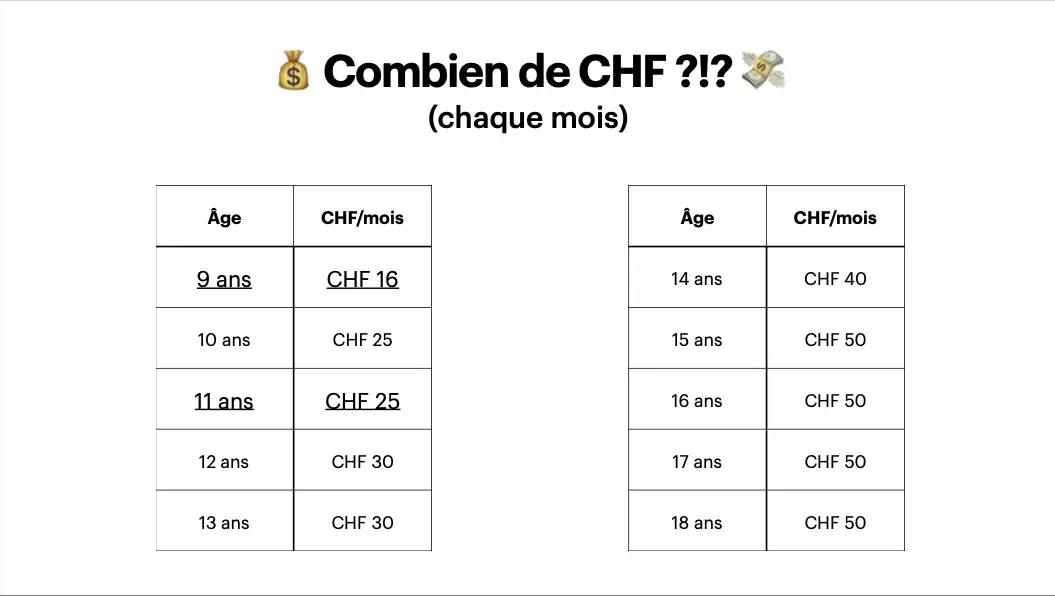

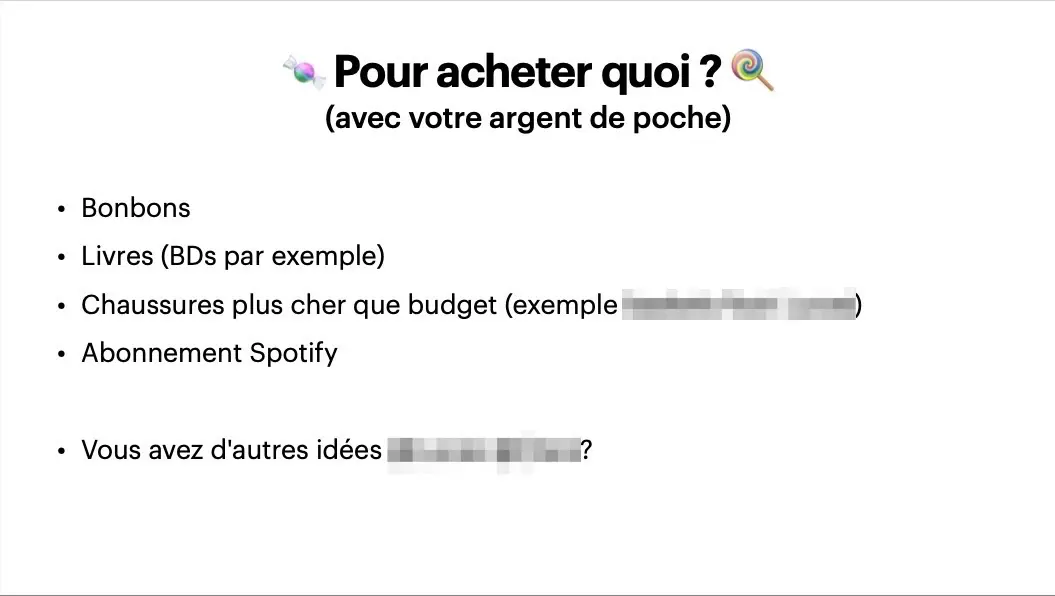

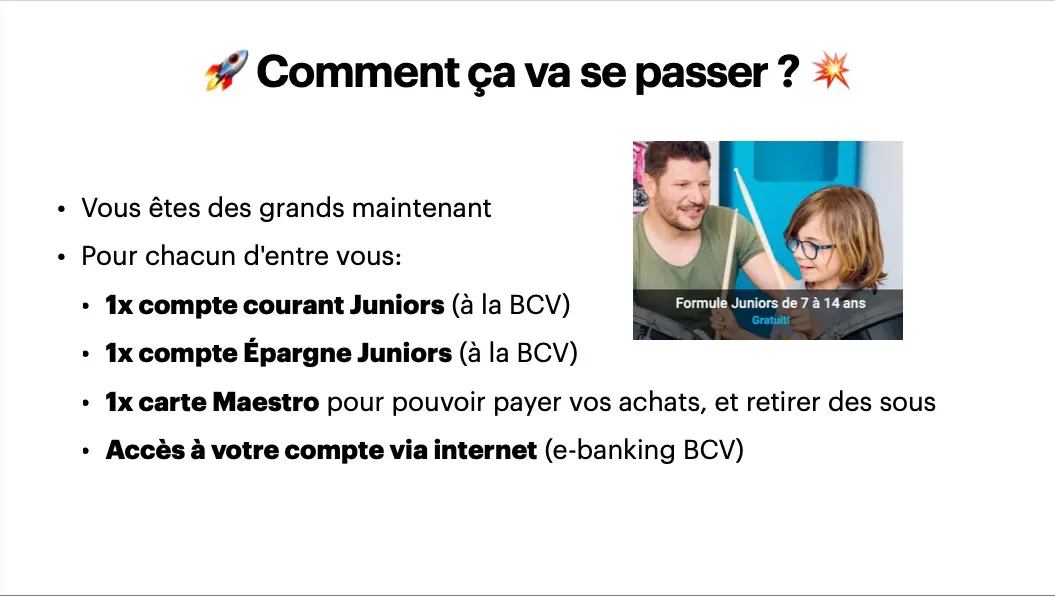

As I read the story of Becky’s early life, I couldn’t help but think to myself: “This confirms to me that we’re doing the right thing by teaching our children the basics of personal finances and investment with Mrs. MP.”

Even though it’s up to them to decide whether or not to continue on the path they’ve been taught, without this education they’d be less well equipped for their adult lives.

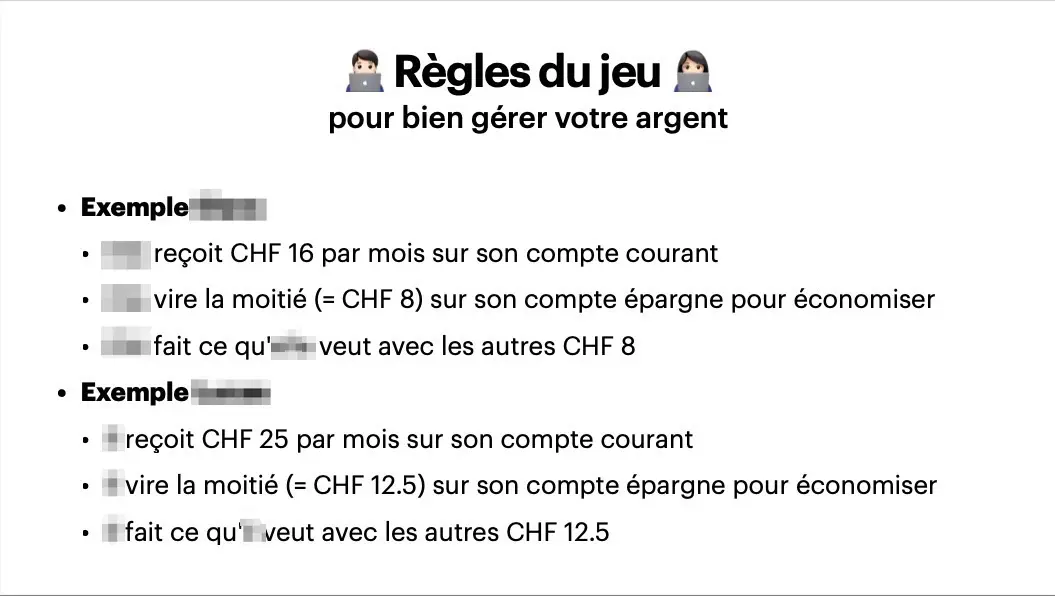

There are two rules I’m looking forward to watching when they grow up:

Any money received is divided in two: 50% goes into savings, and they do what they like with the other 50%

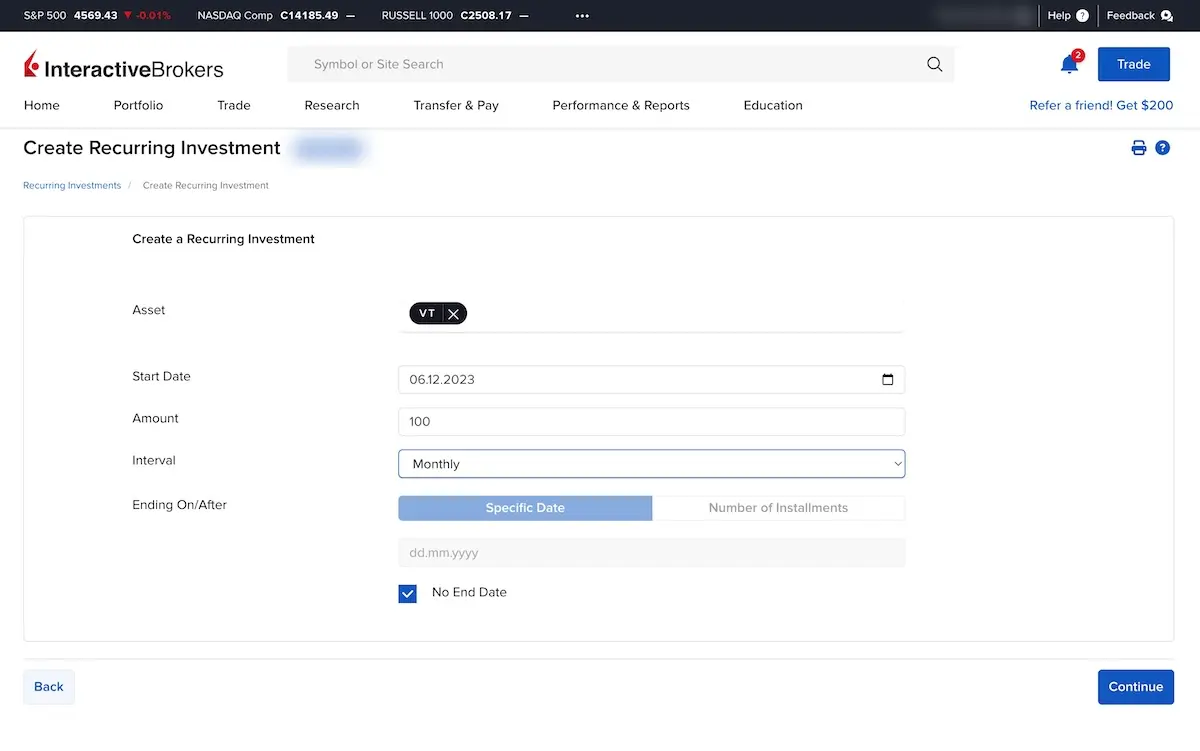

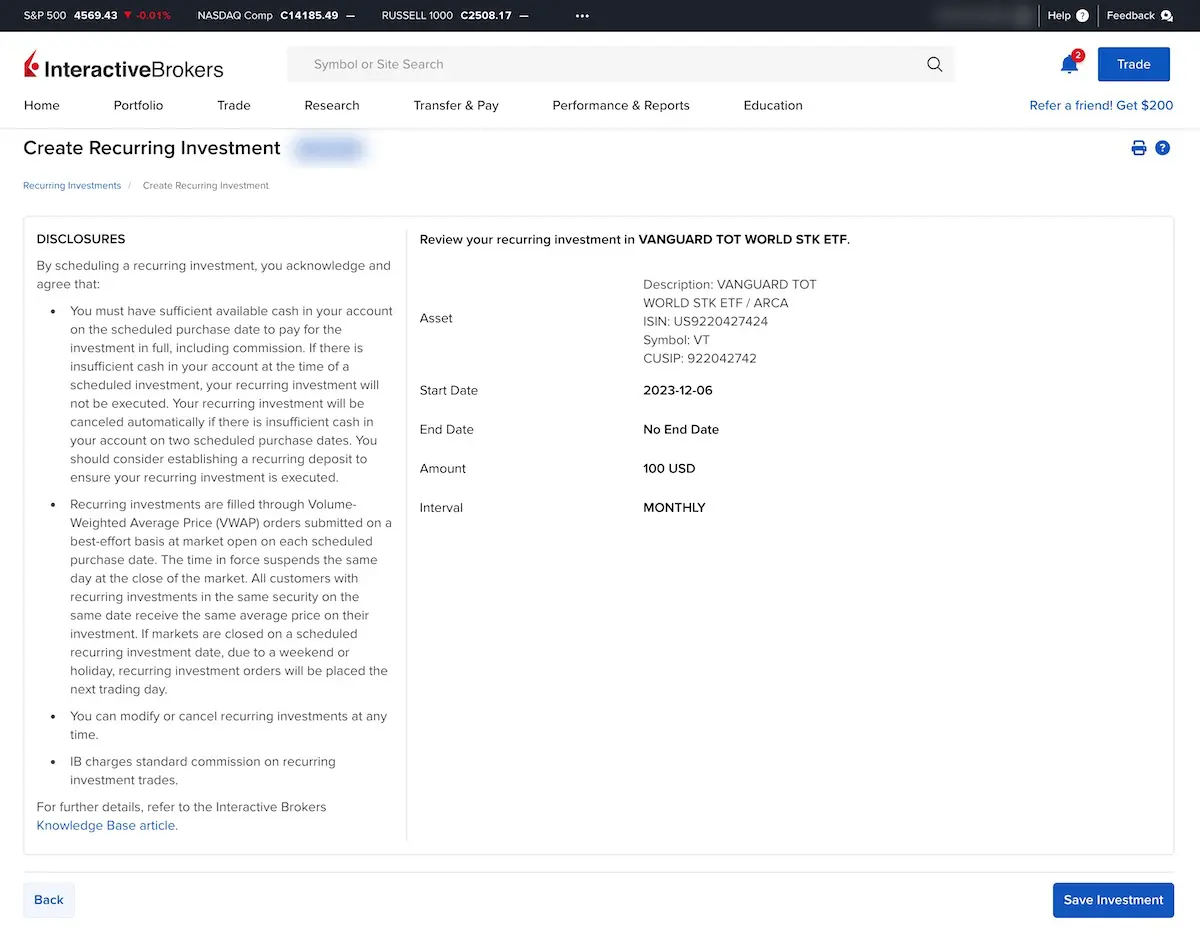

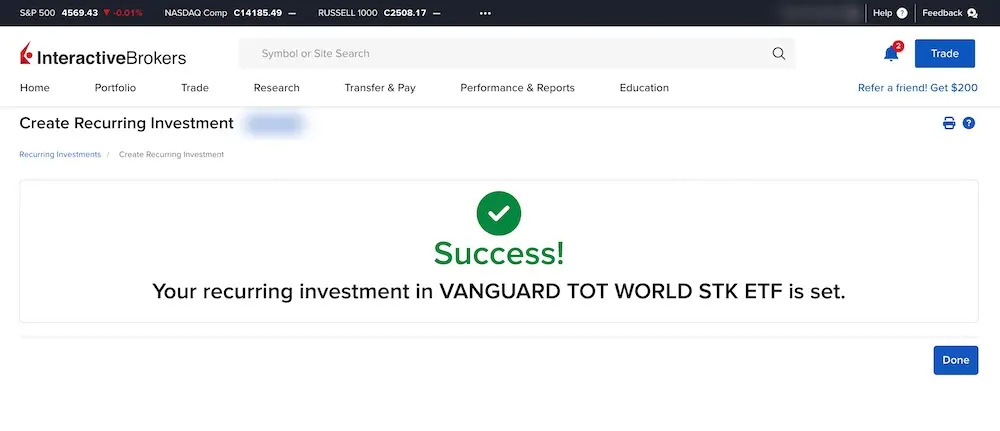

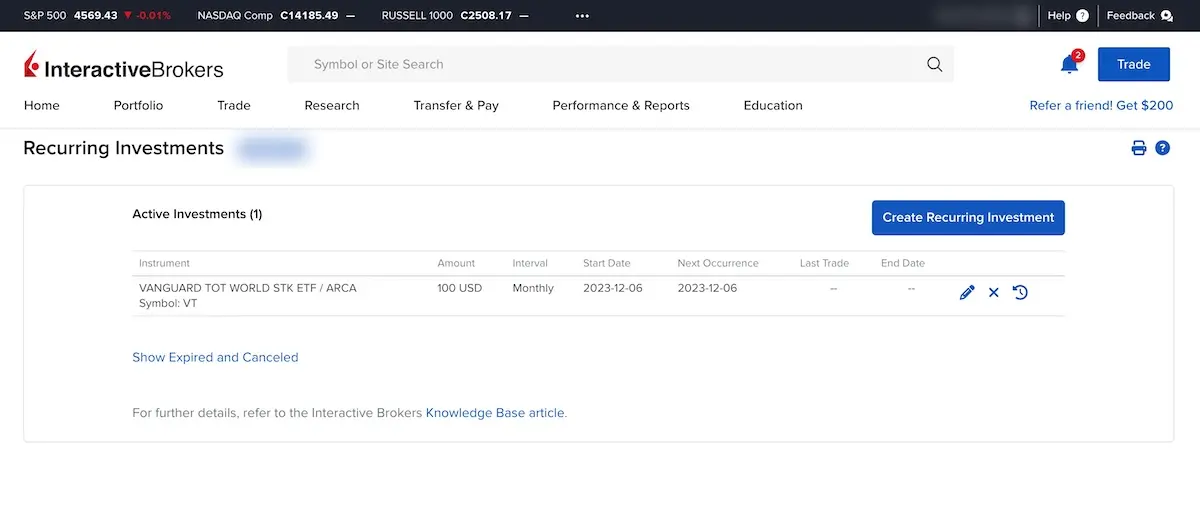

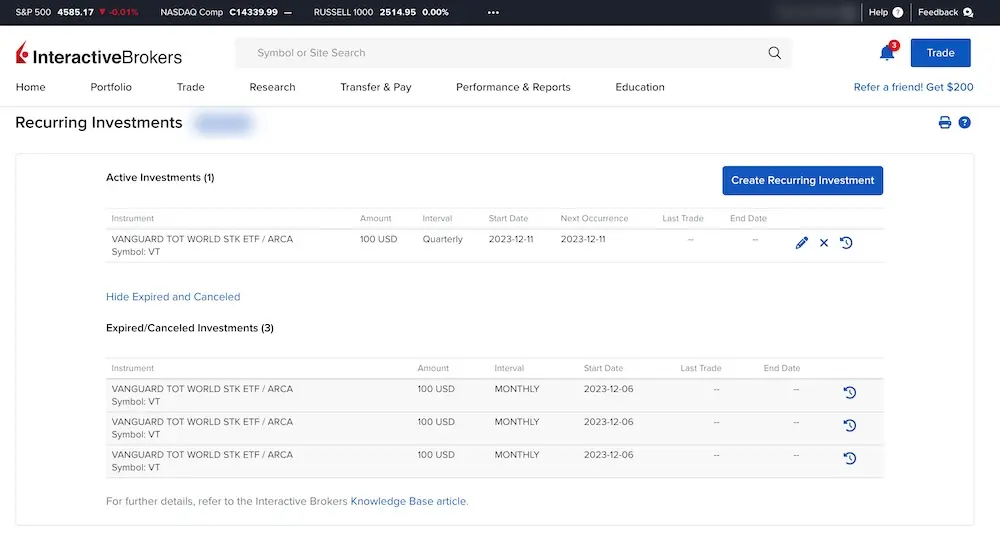

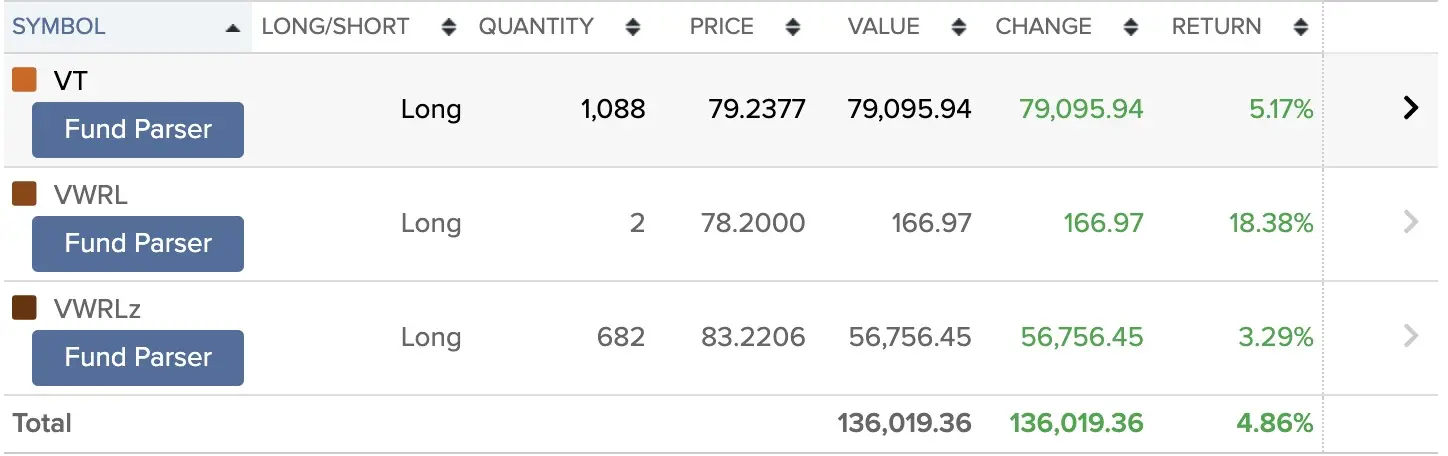

All their savings are invested in the VT ETF. We set them up with an Interactive Brokers account each. And they invest themselves every quarter (well, with me next to them, because they click mega fast and I wouldn’t want them to click “Sell” by mistake haha!)

The power of the 4% rule

Reading Becky’s story reminded me of the day I discovered the 4% rule on Mr. Money Mustache’s website.

Thank you Internet though…

It was spring 2013.

And then, EUREKA!

I had finally found the method that would make me rich and financially independent in the long term. It was mathematical. It was logical. The opposite of all those Influencers-Insta-Youtube-Tiktok-quick-money-crypto-yo! I knew it would take years, between 10 and 16 in my case. But I knew I could stay the course with my persistence.

I’m looking forward to moving forward with our FI Planner tool to bring even more detail than the vague 4% rule to any Swiss who wishes to reach early retirement well before the official age of 65. If you’d like to join the waiting list, let me know by replying to any of my newsletters.

Freedom to deepen your why

While chatting with Becky by email in preparation for this article, she wrote me an important sentence:

Now that I have more free time, I might build up these “side jobs” [that I already had when being an employee] to earn more, and/or possibly other work where I feel I can add value and help people, but in general I am grateful that I don’t feel the pressure to HAVE to earn more money from them or any activity. I think actually that’s when things can take off even more successfully, i.e. when one focuses on the “Why” and not on the money earned.

I so agree with the last part of her sentence.

This is one of the reasons pushing me to “really” be FI before quitting my job as an employee. Because if there’s one thing I wouldn’t want, it’s to have to think about how to make money with the blog first, before considering the WHY behind it.

And you, what did you take away as inspiration or lesson from Becky’s story?

US citizenship: beforehand I was a US citizen, so I was not able to invest in passive investments like ETFs outside of the US without harsh tax consequences (and some brokerages outside the US just won’t allow ETF investing for US persons). Ironically I could invest in crypto here without any problem!

Then I got Swiss citizenship and gave up the US one so that financially things are much less complicated. So I have moved my non-retirement funds from US to Switzerland and invest in ETFs (and have some cash) here.↩︎

Buckets: I’ve tried to at least earn something on the cash amounts, so I opened a savings account with ZKB and one with Swissquote Invest Easy, maximizing the amount to earn the most interest (I don’t usually like Swissquote’s fees, but as this savings account is free, I decided to take advantage of it).

My non-cash buckets are all ETFs (in Interactive Brokers and DEGIRO) and Index Funds (in my US retirement fund/brokerage). In addition I have a (slowly) increasing equity in the apartment that I live in and bought 15 years ago but am not counting that in my total net worth when I calculate the 4% rule.

My mid-term bucket consists of some Bond Index Funds (in the US) and Gold ETFs here. Long-term bucket is all equity ETFs and index funds, mostly Vanguard, which I started investing in already 30 years ago in the US when I started earning money from my first (real) job. So your recommendation of the VT ETF is right in line with what I’ve done all these years 👍

As for the overview, I have 85% in Equity ETFs/Index Funds, 5% in Fixed Income or Gold ETF, and 10% cash. I’m still in process of investing more of my cash, since I just recently transferred it from my US investments to reduce my currency risk.↩︎

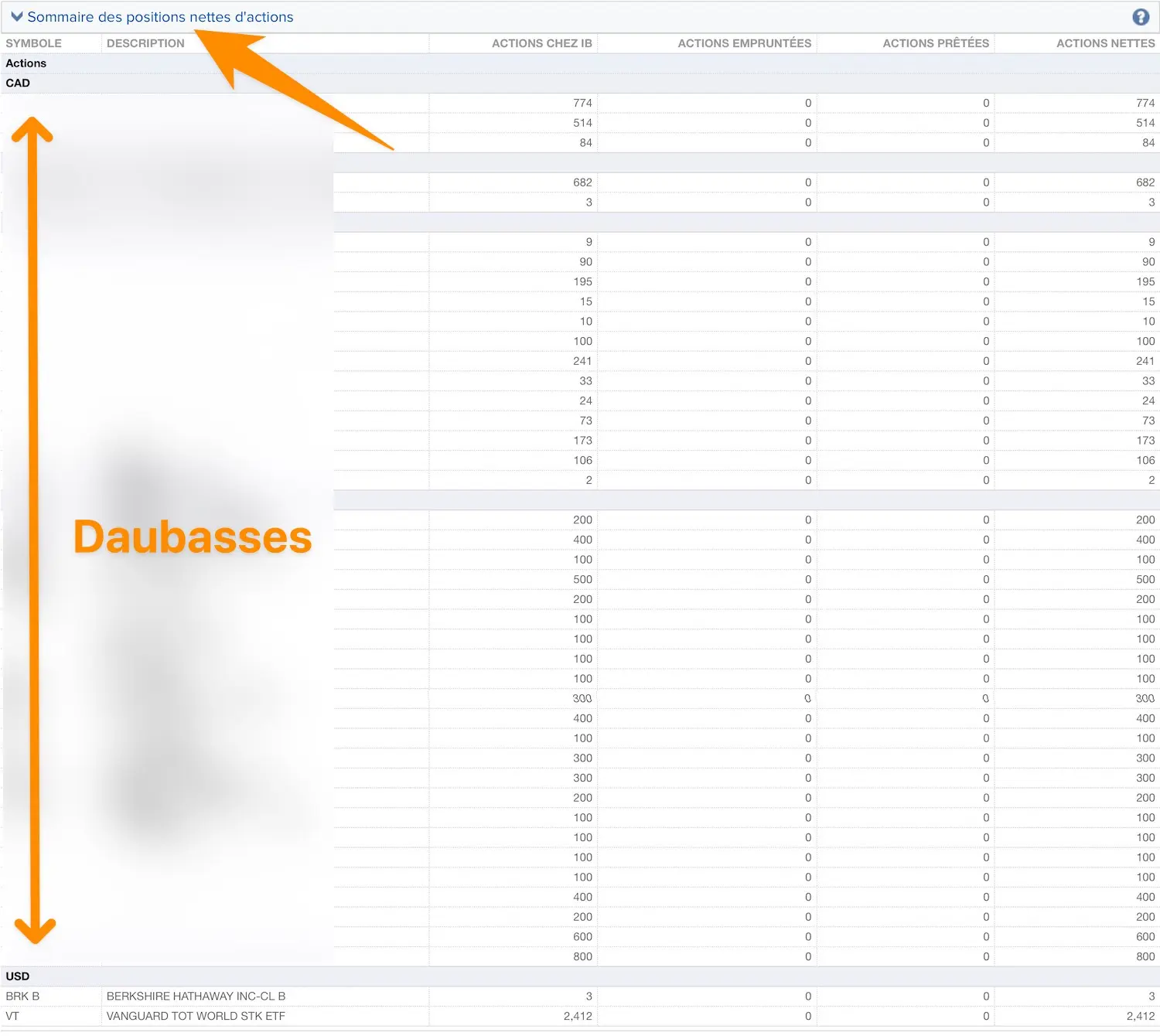

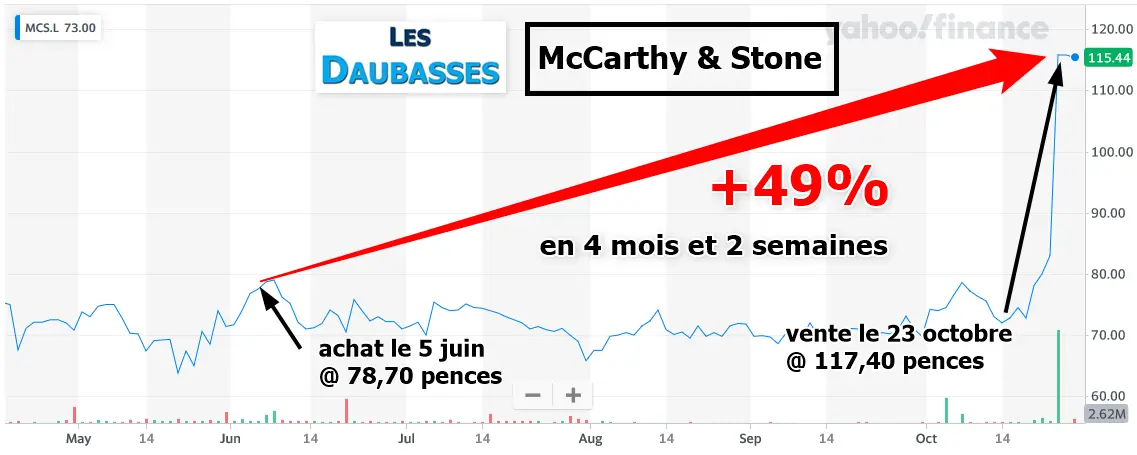

]]>I'm not Value Investing with The Daubasses anymore2025-03-27T02:27:00+00:002025-03-27T02:27:00+00:00MPtag:www.mustachianpost.com,2025-03-27:/blog/im-stopping-with-value-investing/I have value invested for 6 years (via the Daubasses newsletter), and have decided to stop due to two main reasons.I’ve been reflecting on it for several months, but I’ve now made the decision. I’m going to stop with “value investing” (via my Daubasses portfolio).

If you’ve just discovered my blog with this article, I’d recommend you to read about my experience with value investing.

In sum:

Several years ago, I was looking to increase my stock market returns

This was before I fell in love with real estate investment in Switzerland

Objective: +10% annualized return over the long term

The 2 reasons behind my decision

Since 2019, I’ve spent more and more time on real estate investments starting with a first rental property, then a second, you know the rest :).

It’s time-consuming, but I like it.

And like any good productivity geek, I know that focus helps to achieve success in any field.

Knowing that real estate offers me a greater return than the potential of my Daubasses portfolio, the latter has become a distraction in my strategy.

Also, the Daubasses newsletter and forum are hugely interesting but I never have the time to read, learn or delve into the subject, in order to potentially find my own little nuggets of value.

I’ve therefore decided to overcome the “FOMO” effect and stop my Daubasses portfolio for these two reasons:

Simplification of my global investment portfolio, by getting rid of the distraction and active management needed to buy/sell by strictly following the Daubasses signs. This is in order to put all my active management concentration into real estate in Switzerland (rental return and development).

Not enough time or desire to dig into the gold mine of information provided by Les Daubasses (the forum is incredible). It’s very individual, as some investors will prefer the appeal of being glued to their computer screen like Warren Buffett, while others see their future in the more, if I dare to say, interesting and beautiful real estate.

The gold mine of the Daubasses forum

Do I still recommend Les Daubasses?

You could wonder if I’m hiding something behind my decision.

And I’m really not.

If I wasn’t so active in real estate in Switzerland, I definitely would have kept this value investing part of my portfolio. I have to admit that being a bit active when it comes to my investments satisfies this part that every investor has inside them of wanting to “actively do something” (N.B. I only have CHF 38'000 in Daubasses, which represents 4.6% of my total wealth invested in the stock market).

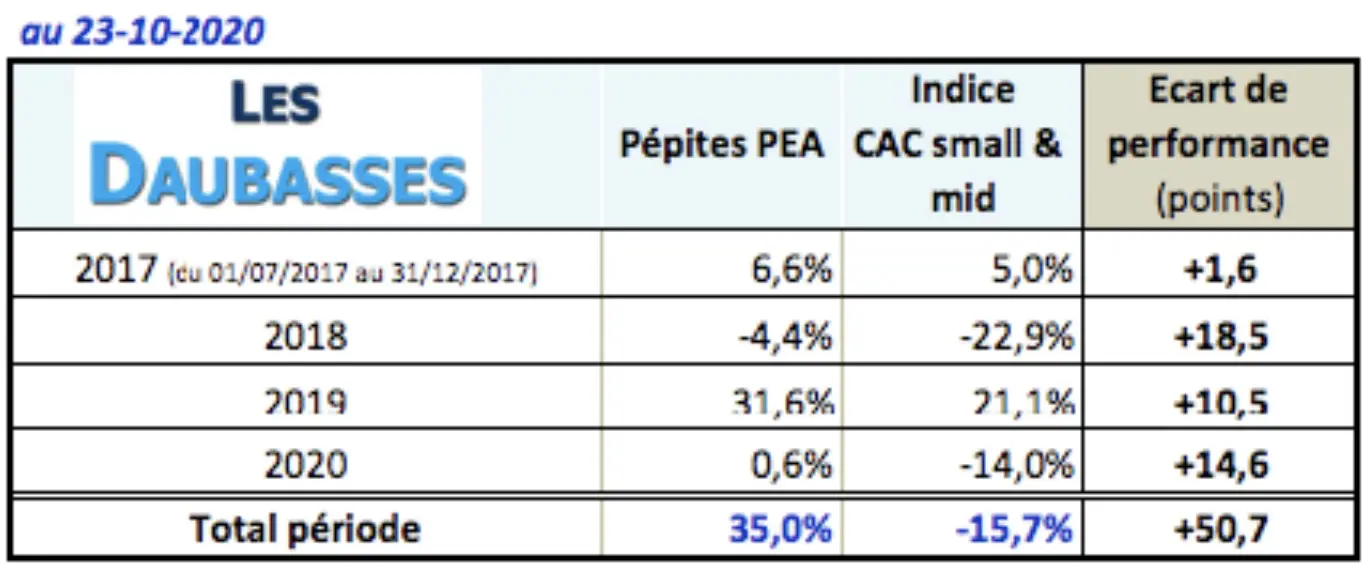

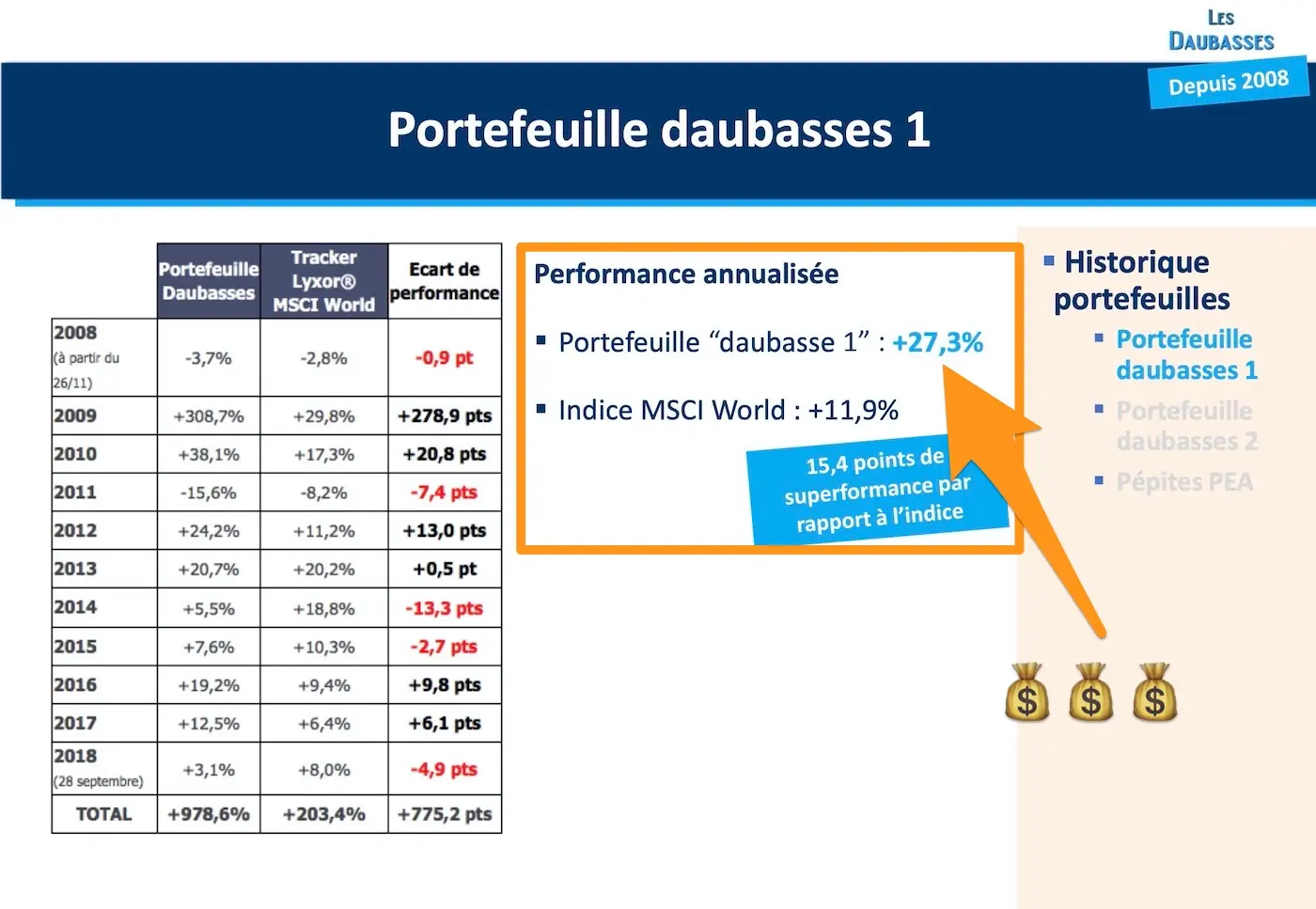

My Daubasses track record

Just to give you context on what we’re talking about, here’s the performance of my Daubasses portfolio.

If I combine these two periods, we get an annualized return of our Daubasses portfolio of… 8.1% between June 2019 and March 2025.

Note to myself: I was expecting more, but overall, over a period of 6 years, it’s actually not bad at all.

“But MP, it’s ‘just’ a few clicks every month at most!”

I can hear you saying this behind your screen already. And a part of my brain agrees!

But the other part of my brain which has read “The One Thing” knows how much simplification and focus are catalysts for success.

I had the same problem before when I had to give up several entrepreneurial projects just to write the blog that you’re reading. And I would never regret this decision!

So yes, I could keep this little bit of my portfolio in “Daubasses / Value Investing”… but no!

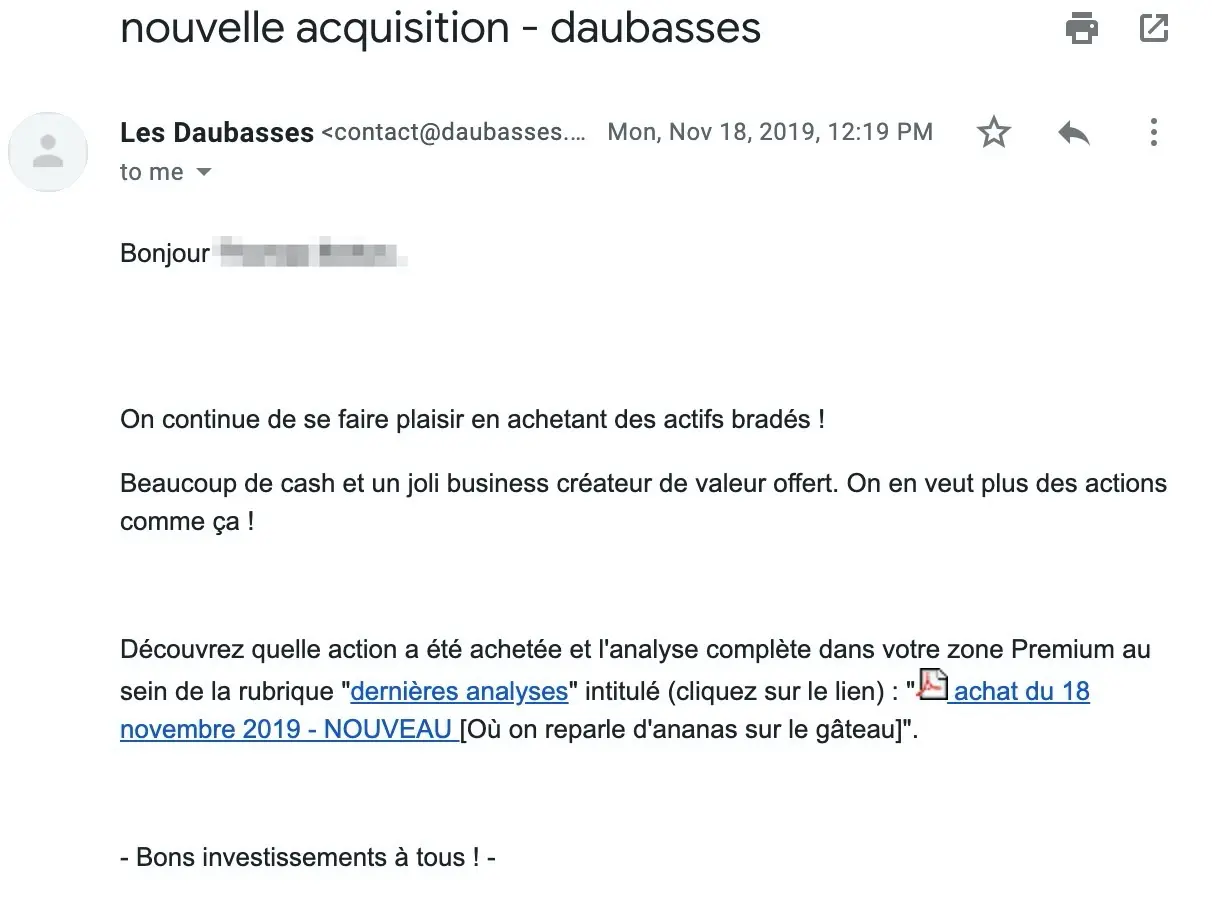

Example of a Daubasses buy alert received by email

How I’m going to divest from my value portfolio

I’m not on a kamikaze mission, so no, I’m not going to sell my entire Daubasses portfolio in one go, and endure several losses.

My strategy is the following:

I won’t buy any new Daubasses stocks, nor strengthen any position when Les Daubasses do it

I’ll sell each Daubasses stock when Les Daubasses sell them

It may take several years to sell off the whole portfolio, but that’s fine with me

Conclusion

The beauty of simplicity can also be applied to the world of investing. I’ve decided to concentrate on the active management of my investments in real estate rather than value investing.

The main reason for me: I can reach a greater return via real estate (15%+ in rental, and much more in real estate development) than with Daubasses (10%+). However, it requires greater effort and time, and I fully acknowledge that.

Nevertheless, if I wanted or need to get into value investing again in the future, then I’d still do it with Les Daubasses. Their forum is a gold mine for anyone who is willing to devote the effort and time to it, and the same for their newsletter.

For me, when it comes to the stock market, I’m pleased to only have a single interest with my favorite VT ETF:)

At least I’ve tried it, and I have no regrets!

How about you, have you reviewed your investment strategy? Which part did you end up cutting out?

]]>Thoughts from my interview with Fabienne and Benoît (Swiss blog Novo-Monde)2025-03-13T02:27:00+00:002025-03-13T02:27:00+00:00MPtag:www.mustachianpost.com,2025-03-13:/blog/thoughts-from-my-interview-with-fabienne-and-benoit-novo-monde/Red wine? Life phase transitions? Unicorn trainer? Here are my thoughts from my interview with Fabienne and Benoît from Novo-Monde.I lost track of time when chatting to Fabienne and Benoît (from the Novo-Monde blog) about their journey of entrepreneurship and backpacking around the world (for 1h47 haha!)

The transcription of the article was pretty long. So, I thought it was better to separate my thoughts in this dedicated article.

Red wine, yes, but above all the mirror effect!

I laughed a lot at their mention of red wine, which helps to resolve all of their problems. It’s clear that alcohol reduces the obstacles in your brain, and enables you to be creative.

But red wine alone wouldn’t be as effective.

I get the impression that what helps them to find a solution to a significant problem is the fact that there are two of them around the bottle of red. With the well-known mirror effect, like when you go to a therapist or coach, and you talk about your problem.

The person opposite reshapes it.

This makes you become more aware of it, and helps you to better understand your own thoughts and emotions…

…and often to find your own solutions.

Because if Fabienne or Benoît were alone in such a situation, he/she would end up stuck in “daydream” mode. With or without alcohol :)

So wine, yes, but with someone else (a person in whom you have 100% confidence), it’s even better!

Life phases (and transitions)

When we were talking about the psychological threshold between nomadic life and sedentary life, Fabienne responded by saying that it had been done gradually. And not out of the blue.

That immediately made me think of a problem, in my very Cartesian brain (haha!), where I too often see the life of financial independence as moving from one life to the next overnight.

You’re working on a Tuesday. And then boom, on Wednesday you’re FIRE! 💥

Although, since I’ve been getting closer and closer to financial independence in the last 2-3 years, I’ve realized like Fabienne mentioned that it happens gradually.

And I think it’s really important to see it as a transition from one life phase to another, which takes time. Otherwise, it can be very destabilizing psychologically.

That brings to mind a book that a reader recommended to me many years ago: “Transitions” by William Bridges.

The book 'Transitions' by William Bridges (recommended by MP)

This book made me realize at the time how past rituals (like from the time of Yakari etc.) were important.

We need rituals. Previously, there were rituals for each transition through an important point in life. Adolescence, reaching adulthood, etc.

But now, we no longer have these milestones which can seem to us to just belong in folklore…

However, that really helped to apprehend such changes, like the transition from nomadic life to sedentary life, or from employee to FIRE.

One of the ways of managing such transitions (when you’re right in the middle of it) is to write your autobiography, in order to verbalize where you’re coming from, and in order to better see where you’re going. And that’s sort of what Fabienne and Benoît are doing when they do their annual review. As I think that helps them a lot more than a simple annual recap.

This also makes me realize that my own reviews (in the form of “blog anniversary” articles) help me just as much. Interesting :)

I’m mentioning all this to tell you that if you’re in a period of significant change (marriage, divorce, change of job — and whether it’s positive or negative, it’s still a change of life phase), then I strongly recommend this book to guide you.

And it’s not an esoteric book, pitched at a high level or whatever, it’s actually very rational ;)

I want to give it all up haha!

You feel like giving up… get to work!

Fabienne got me with this Paulo Coelho quote:

If you think adventure is dangerous, try routine. It is lethal.

I’d already read it when I was younger, but now, a few years away from my FI date, it just makes me want to pull the plug. NOW :)

Find your why

I felt that Fabienne and Benoît were truly fulfilled. Really satisfied.

That then reminded me how much the higher you go up Maslow’s hierarchy of needs, the more it’s important to know your “why”. Because otherwise, nothing makes sense anymore.

Earn money? Why when you don’t need it to live anymore.

Have free time? You have ALL the free time in the world, but to do what, you ask yourself…

I’m talking about this here as it’s the same for a plan to become financially independent. You need to know your why for two reasons:

It’s a strong “why” that will enable you to keep going when your morale dips over a journey of 10 to 17 years to achieve FIRE

And it’s a strong “why” that will enable you to be as fulfilled and full of satisfaction as Benoît and Fabienne clearly are

Because no, having a pile of cash (as big as it may be) doesn’t increase your baseline happiness.

All this means: define your why, and the rest will follow! (tip to help you: Ikigai)

South America on my list

Ah, traveling…

The Machu Picchu of the Incas, in my dreams!

I love big open spaces. Scandinavia, Canada, Siberia, all these names transport me just by writing them.

And I admit that when I think of big open spaces, South America doesn’t spring to mind.

Chile (photo credit: novo-monde.com)

But when Benoît responded without a second thought at the end of the interview by saying: “South America without hesitation, for its big open spaces!” — well, that immediately set me thinking.

I did a search on Google Images straight away, and now South America is on my list of the next trips to do :)

Tayrona National Park in Colombia (photo credit: grubenvadrouille.com)

Do you want to adopt their lifestyle?

Whether it’s to become a nomad (digital or not ^^) during a round-the-world trip, or live in a coliving space, the only thing that differentiates you from them right now is simple…

Taking action.

As I often talk about on this blog, it’s clear that the idea of giving up your job and heading off for a year can be terrifying or too big a step. But you don’t need to go in so strong.

You can already read their blog to inspire you, then plan a trip of one week more than your usual two weeks’ vacation, and to a place that you don’t know at all.

This principle of gradual exposure to a new experience is what works best for daring to take the plunge into any adventure that scares you: from the stock market to living in a coliving space;)

And talking of coliving space, if you dream of setting one up, the first good step could be to simply reserve a few weeks of remote working at Alpiness Coliving, it seems like the owners are cool ;)

The most important thing being: stop daydreaming, and take action, now.

The places mentioned by Fabienne and Benoît

I wanted to share here a few photos of the places mentioned by our two fellow travelers, around their new paradise of Les Haudères in Switzerland:

Loop hike at Grande Dixence: the Prafleuri hut

All the photos are credited to Novo-monde.com (Fabienne and Benoît):

Climb above the Grande Dixence dam

Oh, these glacial blue rivers and Swiss mountains <3

Fabienne made me laugh out loud when she mentioned being a unicorn trainer.

I’ve already talked to our children about believing in their dreams, and not letting themselves become discouraged by people who just project their own fears onto you.

But this new angle of a unicorn trainer is so fun that I shared it with our MP children and they loved it haha!

In Fabienne’s words:

The important thing is to try and not be afraid to take risks. In fact, as long as you’re doing something and you continue to learn, it’s never the end of the world.

When they’re older, I’ll tell them how I also believed in my dreams. And yet, in 2013, when I was explaining my financial independence plan to an acquaintance, this person tried to discourage me by saying that she’d already tried it and hadn’t even lasted three months… but in my case, I’ll have made it and would be living proof for my children ;)

Fabienne and Benoît are financially independent

After having edited the video and put together this article, I came to the realization that Fabienne and Benoît are in fact financially independent.

They’re living their dreams while receiving passive income from the blog and coliving space. Well yes, it’s not passive like a loafer would imagine on a beach with nothing to do but laze around for hours on end… on the contrary, it’s even more positive passive, with diverse and varied activities which fill them with satisfaction, joy, and appreciation.

Genuinely, bravo to you two!

And you?

What did you take away from this interview with Fabienne and Benoît from Novo-Monde / Alpiness Coliving?

]]>Interview with Fabienne and Benoît (from the Swiss blog Novo-Monde)2025-02-27T02:27:00+00:002025-02-27T02:27:00+00:00MPtag:www.mustachianpost.com,2025-02-27:/blog/interview-fabienne-benoit-novo-monde/What if you too could go on a world tour, then open a coliving space in Switzerland? Fabienne and Benoît explain their journey in detail.When I found out that Fabienne and Benoît were embarking upon a new adventure in their life of backpacking around the world, I just had to interview them for a second time.

Who are Fabienne and Benoît from Novo-Monde?

Fabienne and Benoît are two Swiss people who left to travel around the world in 2012.

This decision changed the course of their lives.

I came across them through their blog Novo-Monde, when I was also dreaming of doing a similar thing.

And as they’re Swiss, that made it all a bit more special.

Then, by chance (in fact not, as I created this chance!), I contacted Benoît to arrange meeting up for a coffee as two Swiss bloggers.

Since then, we’ve always kept in touch, though irregularly.

Then, when I saw that they were launching a coliving space in Switzerland during 2023, I wrote to him to set up a new interview, of which here is the result.

Video with Fabienne and Benoît

Transcription of the video

If you prefer to read rather than watch the video, then here’s the transcription of my interview with the cofounders of Novo-Monde and Alpiness Coliving.

In light of the length, I’ve taken the liberty of summarizing some parts via ChatGPT :)

1. Can you introduce yourselves?

We both grew up in Switzerland, followed a traditional academic path, and started fairly conventional careers. I (Fabienne) studied statistics and econometrics, while Benoît completed a PhD in digital biomechanics. After our studies, we had our first expatriation experience in Vienna, where Benoît was doing his PhD, and I was working at a startup.

But soon, we felt the need to move even more. We decided to embark on a 19-month trip around the world. At the time, I was worried about how it would look on my CV, but in the end, the experience completely changed our perspective on work and life. It was also during this journey that our blog was born—originally just to share our travels with family and friends.

When we returned, we took jobs in Switzerland, but the corporate experience, especially for me, turned out to be frustrating. I ended up in burnout, and that’s when we decided to leave Switzerland and become self-employed. We first started building websites while continuing to grow our blog, which eventually became our main source of income.

We fell in love with the digital nomad lifestyle. We spent several years between Europe and Asia but quickly realized that finding a good place to live and work wasn’t always easy. That’s when we discovered colivings, particularly during a stay in Tenerife, where we had our first experience as volunteers in a coliving space. We immediately connected with the concept—a place where you can work efficiently, be surrounded by like-minded people, and avoid the isolation of remote work.

Since 2018, we’ve spent nearly 50% of our time in coliving spaces, and the idea of opening our own quickly became obvious. What impressed us the most was the impact a coliving space can have on a small village. In Galicia, for example, we saw a community of remote workers developing social and tech projects to help the local area.

Today, we have found our ideal place—in the heart of the mountains.

2. The Paradeplatz in Zurich or the jet d’eau in Geneva?

We are not made for city life, whether it’s Paradeplatz or the Jet d’Eau in Geneva. The urban rhythm doesn’t suit us. Personally, I have always preferred quieter places, while you used to be more of a city person. But today, we both agree: the city is too far from nature.

To be happy, we need to be able to start a hike right from our doorstep. This morning, for example, we went skiing for three hours before recording a podcast. That’s the kind of quality of life that, for us, is impossible to find in the city. So if we had to choose between the two… we wouldn’t choose either.

3. Which is the book you have gifted most often?

I tend to listen to podcasts more than I read books. Since Covid, I’ve been tuning into a lot of content related to environmental issues, a topic that matters to me. One of my favorite podcasts is Serw, which is actually a YouTube channel but also offers long-format podcast episodes. Not everything resonates with me, but I appreciate the in-depth discussions and diverse perspectives.

When it comes to books, I’ve read several by Naomi Klein, whose philosophy aligns well with my own. However, I don’t read traditional books often. I read a lot in school out of obligation, but nowadays, I consume more content online. This might be against the current trend of reading personal development and entrepreneurship books, but I’ve tried a few, and they don’t always click with me. For example, The 4-Hour Workweek was hugely popular when I was in Chiang Mai—everyone recommended it—but I just couldn’t get into it.

A documentary I absolutely loved, though unrelated to entrepreneurship, is The Biggest Little Farm. It follows two people who, after a career change, start a biodynamic farm, letting nature restore its own balance. The film beautifully illustrates how ecosystems self-regulate over time. For instance, they initially struggled with a mole infestation, but these moles actually aerated the soil, which later helped them avoid flooding. Then, owls arrived and naturally controlled the mole population, followed by lynxes that further stabilized the ecosystem. It’s a really inspiring documentary, even if farming isn’t your goal.

Lastly, one website that had a massive impact on my life is Le Site du Zéro, now known as OpenClassrooms. Originally a platform for learning to code, it has expanded to offer courses on a wide range of subjects. The creator of the site is truly inspiring, and he has been featured in several great podcasts. Without a doubt, this website has played a major role in shaping my journey.

4. If you could set up a giant billboard in the middle of the Paradeplatz in Zurich, what would it say?

A great way to promote our coliving space would be to contrast two different lifestyles. On one side, we could show an image of our workspace with a breathtaking mountain view, and next to it, a picture of the same resident skiing through fresh powder after finishing their workday.

A quote from Paulo Coelho could reinforce the message: “If you think adventure is dangerous, try routine; it is lethal.” The goal is to encourage people to rethink their priorities and break free from the rat race.

A catchy tagline like “I live and work where you go on vacation” would perfectly sum up the spirit of coliving—combining work and an exceptional quality of life.

5. What is a coliving space? And what’s your role as managers?

A coliving space is designed for people who work remotely. It is usually a large house with dedicated work infrastructure, such as a coworking space, a conference room, and excellent WiFi. In addition to professional facilities, it offers shared spaces like a large communal kitchen, a living room, and even a small gym. The goal is to create a comfortable home in a natural setting, close to the mountains, while ensuring an optimal work environment.

The Role of the Manager

As managers, our role will evolve over time. Right now, since we just launched the coliving space, we handle everything ourselves: logistics, administration, cleaning, and minor renovations. However, in the long run, our goal is for the management to require less effort, more like overseeing a large shared house.

Daily Life at the Coliving

Residents have different work schedules, some following European time zones and others American ones. To foster a sense of community, we organize group dinners from Monday to Friday, where everyone takes turns cooking for the group. This ensures a daily moment of social interaction and strengthens connections.

Beyond work, we organize activities to help residents explore the region: hiking, mountain hut stays, walks around the village, game nights, and movie screenings. Another key aspect of coliving is skill sharing. For example, a resident specializing in artificial intelligence recently gave a talk about his field, inspiring an interior architect to collaborate with him and launch a business project.

The Coliving Spirit

Coliving is not just about living and working together—it’s a space for networking, learning, and creating new opportunities. Our job is to facilitate these interactions and encourage collaborations among residents. While we still handle most operational tasks ourselves, we plan to delegate some of them over time to focus more on community-building and enhancing the coliving experience.

6. What type of clients does it attract? Only digital nomads, or people from other walks of life?

Coliving attracts a much more diverse crowd than the usual stereotypes suggest. While there are developers, designers, and online trainers, many professionals from various industries also take advantage of remote work opportunities for a few months each year. For instance, we’ve hosted employees from Galaxus, as well as HR professionals and people from other fields. Some choose a mountain coliving like ours in Switzerland, while others prefer seaside locations like Tenerife.

The age range is also quite broad: our youngest resident was 22, the oldest 54, but in other colivings, we’ve met people as old as 75. A particularly interesting case was a chef in his 60s who came to write a book on Peruvian cuisine. He tested recipes and let us taste his dishes, making for a unique and memorable experience!

Ultimately, coliving is for anyone with the flexibility to work remotely. For example, my sister, a statistician at Lausanne’s public transport service, often stays with us because she can adjust her schedule. Similarly, a real estate agent from Martigny arranges her property visits once or twice a week while handling administrative tasks from our coliving. So, coliving isn’t just for digital nomads—it’s a much broader and more adaptable lifestyle solution.

7. Do you consider yourselves financially independent with all your passive income from the blog?

Since purchasing our coliving space on April 19, 2023, we have barely worked on our blog, yet our revenue has remained stable. In fact, last summer, we recorded our highest earnings ever, even though we weren’t actively working on it. It’s a bit ironic, but it proves that our past efforts continue to pay off.

That said, so-called “passive” income still requires prior effort and ongoing maintenance. You can’t just sit back forever, or performance will eventually decline. However, our financial situation gave us a safety net, unlike those with traditional jobs who would see their income drop to zero if they embarked on such an intense project as renovating a hotel.

Our blog and related products (books, etc.) generate around 80'000 CHF per year. It’s not an enormous amount, but it’s stable and requires almost no effort at this stage, apart from keeping the site online with a steady traffic flow. This source of income allows us to maintain a comfortable lifestyle while fully dedicating ourselves to our coliving project.

8. How much did the hotel cost? How much for the work? Total cost once complete?

We haven’t finished the renovations yet, but the hotel cost us CHF 870'000. It’s a large 600 m² building with 11 rooms, a separate apartment, and a ground floor that used to house a restaurant and a bar, which we have completely transformed. The purchase price is comparable to that of a three-room apartment in Geneva, but with significant renovation work required.

The building is old and, while it was still inhabited, it hadn’t been in operation for 12 years. We have a budget of CHF 500'000 for renovations, with CHF 400'000 allocated for the exterior (facade, insulation, windows, and roof) and CHF 100'000 for the interior. So far, we have invested about CHF 100'000 in interior renovations, bringing the total project budget to approximately CHF 1'350'000.

However, the exterior renovations have been delayed compared to our initial plans. One of the key aspects of this project is that we did almost all the interior work ourselves, with the help of volunteers throughout the summer. This allowed us to renovate a 600 m² building for less than CHF 100'000.

We expect to receive some government subsidies for energy-efficient renovations in Switzerland, but we are not relying too much on them. They might amount to 40'000 to 50'000 CHF, but they will take time to be disbursed. Additionally, since our building is located in a protected village center, we must comply with specific regulations, particularly regarding the stone roofing and solar panel installations.

Finally, we had planned for these costs in our initial budget. We took out a mortgage covering the entire project, including both the purchase and the renovations, rather than just a mortgage based on the purchase price.

9. How much did you save in labor costs by offering bed and board in exchange for help with the renovations?

We spent around CHF 100'000 on interior renovations, but by doing much of the work ourselves, we saved nearly an additional CHF 100'000. For example, hiring professional painters would have cost about CHF 50'000, while we bought high-quality paint for only CHF 2'000. Similarly, we installed 150 m² of flooring ourselves, resulting in substantial savings.

For us, this project is not just a financial investment aimed at generating returns—it is a true life project. We are passionate about coliving and wanted to learn how to renovate, as relying on contractors in Switzerland is difficult. Initially, we had no DIY experience, but we have learned a lot and are now much more independent.

A key element was organizing a collaborative construction project. We invited digital nomads and remote workers interested in coliving to help us in exchange for free accommodation. Over the summer, about ten volunteers contributed to the work, allowing us to make much faster progress. Of course, it required management, but by assigning them the simplest tasks, we optimized their help.

For more technical skills, we hired a renovation coach. He taught us new skills (plastering, painting, flooring, etc.) in one-day sessions, guided us on material and tool purchases, and corrected our work. This service, not well known in Switzerland, turned out to be extremely cost-effective, as it helped us work efficiently and avoid unnecessary expenses.

We also hired a carpenter for a few weeks to renovate the kitchen. He taught us how to use various tools and supervised the work, allowing us to complete most of the renovation ourselves.

Finally, this collaborative approach had a huge impact on the launch of our coliving. Many volunteers stayed or spread the word about the project. As a result, even before opening in September, we had strong demand, and by October, the coliving was fully booked thanks to word-of-mouth from these early participants.

10. Was it not difficult to control quality with other people working onsite?

We believe it all depends on the approach. If the goal is to invest in real estate and scale quickly, we probably wouldn’t have done a project like ours. But in our case, it was a personal project in which we invested ourselves immensely. Of course, we would do it again, but it’s clear that it requires total commitment.

Physically and mentally, it was extremely exhausting. By the end of the renovations, we were barely sleeping, waking up at 5 AM every day to manage every detail. In fact, we appeared on RTS in the Forum show, and several people told us that we looked younger since August. In reality, we had simply regained a normal sleep rhythm after four intense months that had literally aged us!

In terms of work quality, we did almost everything ourselves, except for the installation of fire doors and the electrical system, which we entrusted to professionals. Ironically, these were the two elements that disappointed us the most. Not that they were a disaster, but deadlines were difficult to meet, and the work was sometimes rushed because construction professionals are often overwhelmed and prioritize speed over precision. In the end, we were more satisfied with the work we did ourselves than with what the professionals delivered.

11. How much did you take out in a mortgage vs. own cash?

We faced some challenges in securing funding, especially with our modest income and an unproven business model. However, we had approximately CHF 500'000 in equity, and I inherited an apartment in Zurich, mortgage-free, which allowed us to take out a CHF 450'000 mortgage on the property. Since this property had been rented for over three years at more than 2,000 CHF per month, banks were willing to lend to us.

Technically, we have CHF 820'000 in mortgages, but only CHF 400'000 is allocated to our current project. We received several rejections from traditional banks, but thanks to our long-standing relationship with the Swiss alternative bank (ABS) and our status as shareholders, we were able to obtain preferential rates. This made negotiations easier, although securing the mortgage would have been much more difficult without my grandmother’s apartment.

We chose not to maximize our debt and took out less than the initially proposed amount. However, without my grandmother’s apartment, it would have been impossible to secure such a high level of funding. Additionally, we had to sell our own apartment to complete the financing.

Banks are often more reluctant to finance commercial projects, and since coliving is still an underdeveloped concept in Switzerland, we had to work hard to convince lenders. However, ABS believed in our project, and we were fortunate to have a representative who advocated for our case. In the end, we had a choice between several banks and opted for ABS because it supports projects like ours while offering preferential rates due to our shareholder status.

12. What mortgage rate did you obtain? SARON or fixed?

Fabienne, who has the numbers in front of her, will give you more details, but here’s what I can tell you: we decided to increase the mortgage on the already rented apartment, which allowed us to get a better rate than for our commercial project. We chose a rate of 2.75% for 7 years for the apartment (loan of CHF 400'000) and a rate of 2.98% for the commercial project.

For the coliving project, we opted for a mix of Saron, with a loan of CHF 100'000 at 2.38% when we signed. This rate has probably changed since. We also took fixed rates for 3, 4, and 7 years based on our financial plans. We have obligations to pay off in 6 to 8 years, which influences our repayment decisions. We tried to find a balance between paying off debt and managing it.

We’re not experts in optimization, but we know we’ll keep some debt because it’s in our best interest. The idea is to repay part of it now, but without trying to maximize everything. In any case, the current rates are not alarming for us, and if our project can’t handle this, it would be a sign that there’s an issue with the project.

13. What will be your monthly overheads for the coliving space?

Fixed monthly expenses are around 3,500 francs for low occupancy (e.g., no customers), with mortgage interest at 1,000 francs, tourist promotion tax and other small charges such as taxes. If the coliving apartment is full, costs rise to around 4,000 to 5,000 francs, due to the additional costs of space management, energy consumption and the supply of basic kitchen products such as coffee and oil.

Before the move, the apartment we owned cost around 1,300 francs a month. Today, although the project costs around 3,000 francs a month, we no longer have these housing costs, so we only spend 700 francs more while benefiting from a much larger living area.

The worst-case scenario was calculated in advance, and even in this case, the income would be sufficient to live on. Today, with 100% occupancy until March, forecasts have been far exceeded, and the situation is better than expected.

14. How much do you expect to make in turnover and profits once the coliving is fully up and running?

In 2025, the goal is to generate between CHF 120'000 and CHF 180'000 in revenue with an occupancy rate of 60-80%. However, this includes periods of closure for renovations, such as the creation of a gym in the basement, which will result in months without income.

Currently, the goal is not to make a profit, as all revenue is being reinvested in major renovations like installing a gym, replacing windows, and repairing the roof. The profit will come later once these projects are completed. For now, all the money is reinvested into the project.

On the expense side, the couple has reduced costs by living in the building, meaning they do not need to pay themselves a salary. The coliving project is covering their living expenses with passive income.

The gym, while personal, also serves to attract guests. In the mountains, the off-season is perfect for activities like climbing, and having an indoor climbing wall is a strong marketing tool to draw in guests during low season. The couple also loves climbing, so this project is both a passion and a business opportunity. The climbing wall, located in the basement, allows for adjusting the difficulty of workouts and provides a fun way to improve technical skills.

15. Before the coliving project: what was the breakdown of your income from the blog?

Bloggers are often assumed to earn money through press trips or sponsorship deals, but this is not the case for us. Our values don’t align with such practices, so we mainly rely on affiliate marketing, which is our primary income source. We work with companies whose products we genuinely use, such as Trails (a hiking app) and Leader (a site for technical gear, which we use for our ski equipment). This model works well for us because it’s based on authentic relationships and products we truly believe in.

In addition to affiliate marketing, we also earn revenue from our books. We have three books published by Hvétique Editions and three self-published ebooks. Our royalties generate about 20'000 francs per year, and our ebooks bring in about 10'000 francs annually. While this isn’t enough to live solely from writing, it’s a good supplementary income.

Our business model relies on several small income streams that, combined, allow us to live in Switzerland. During the COVID pandemic, our income from hotels and partnerships dropped, but the sales of our books, especially those about hiking, increased. This helped offset the losses. The key to our success lies in diversifying our income sources, which makes us less vulnerable to fluctuations.

16. After the coliving project: what is the expected breakdown of income?

At the beginning, we didn’t set very high financial goals for the coliving project. Our business plan anticipated about 2000 to 2500 francs per month in additional income, but we don’t really need it, as this money would be reinvested into the project. The medium-term goal is to make the coliving independent, so that we are no longer essential to its daily functioning. This includes hiring a manager to run the coliving and creating processes that will allow it to function on its own.

We believe a salary of 2500 francs for someone working 20 to 25 hours a week with free accommodation could attract motivated candidates, especially from abroad. However, the goal is not pure profitability, but rather to reinvest funds back into the project.

We also plan to hire a housekeeper once the coliving is more full, to delegate some tasks. Currently, we rely on volunteers, often people starting their own businesses or looking to save money. These volunteers work about 15 hours a week, alternating between cleaning tasks and community-building activities.

This model allows us to free up time to focus on other aspects of the project while maintaining a good atmosphere in the house.

17. How did you manage to take the psychological leap from “free and location-independent nomad” to “a sedentary life stuck in a specific place”?