If you’re just starting to invest in the stock market (or want to start), then I recommend this article explaining how I’d invest CHF 10'000 in the stock market if I were starting out today.

And this is how my investment portfolio has evolved over time:

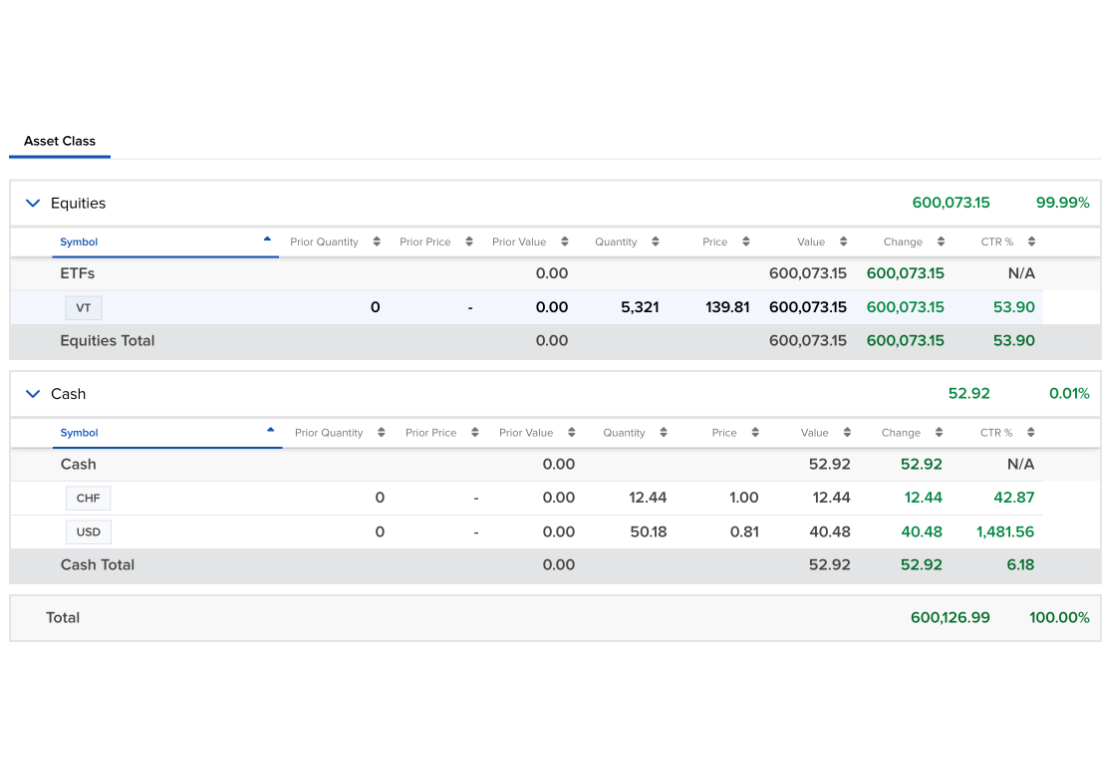

01.2025 => today

After reading more and more articles and books about investing in the stock market, I decided to switch to a portfolio consisting entirely of VT ETFs. You can find all the details in this article: “Why I’m switching from Bogleheads to 100% stocks”.

I still see my second pillar as the “Bonds” part of my investment portfolio. As long as I’m employed.

But when I become financially independent, I plan to transfer all that cash into the best vested benefits account and invest all of it 100% in global stocks.

Simple. Effective. High-performing.

| ETF | ISIN | Symbole | Percentage of portfolio |

|---|---|---|---|

| Vanguard Total World Stock ETF | US9220427424 | VT | 100% |

As usual, if your investor risk profile is more moderate than mine, the Bogleheads method (described below) is still the one I recommend to my friends and family.

05.2020 => 12.2024

For several years, I limited myself to 60kUSD of my favorite VT ETF, and I bought the VWRL ETF above that amount. Indeed, I wasn’t completely sure how the US estate tax (40% potentially!) worked. Then, I finally got a professional’s confirmation that we would be fine. That is, if Mrs. MP or I were to die, we would have nothing to pay to the US tax authorities until our portfolio was worth several millions.

That’s why from now on, my ideal portfolio of 3 ETFs (of the “Bogleheads” type) looks like this:

| ETF | ISIN | Symbole | Percentage of portfolio |

|---|---|---|---|

| Vanguard Total World Stock ETF | US9220427424 | VT | 53% |

| UBS ETF (CH) SMIM (CHF) A-dis | CH0111762537 | SMMCHA SW | 13% |

| Money of my 2nd pillar | n/a | n/a | 34% |

When I say ideal, I mean that if I didn’t own shares in my Swiss-based company (not so good to have a salary and shares coming from the same company!), then I would opt for this ETF UBS SMIM.

As for the money I should have in bonds (as recommended in a Bogleheads strategy where you have your age in bonds, and the rest in shares), if I didn’t have any second or third pillar, then I would keep that part of my allocation in cash (or at worst, I would look for US bonds that still yield some 1-2% — but until when…). Because the current negative bond rates don’t tempt me at all!

Finally, if you have chosen a broker that does not offer the Vanguard VT US ETF, then I recommend that you replace it with the following alternative: Vanguard’s Irish VWRL ETF (whose ISIN is IE00B3RBWM25). N.B. if you have chosen DEGIRO as your broker, then consider buying this VWRL ETF on the Amsterdam stock exchange (known as EAM or Euronext Amsterdam), as you won’t pay any transaction fee :)

And if you’re wondering whether it’s better to go for an accumulating ETF or a distributing ETF, you’ll find a clear and detailed answer in my tax guide for Swiss investors.

11.2016 => 04.2020

| ETF | ISIN | Symbol | Percentage of portfolio |

|---|---|---|---|

| Vanguard Total World Stock ETF (up to 60kCHF max) | US9220427424 | VT | 55% |

| Vanguard FTSE All-World UCITS ETF (for money above 60kCHF) | IE00B3RBWM25 | VWRL | 55% |

| UBS ETF (CH) SMIM (CHF) A-dis [1] | CH0111762537 | SMMCHA SW | 13% |

| My 2nd pillar’s money [2] | n/a | n/a | 32% |

[1] I don’t own this one yet as I still haven’t enough international ETFs, but that’ll be this Swiss based ETF that I’ll buy as soon as I can [2] My current allocation has too much bonds’ money nowadays. If I’d need more of it, I’d anyway keep it as cash, until bonds’ rise up again above 0%

06.2015 => 10.2016

Update 09.08.2016: I stopped investing after our home purchase back in summer last year. The portfolio below had quite a short term view with two CHF hedged ETFs. I wouldn’t recommend an hedge ETF anymore for a long term perspective. We’re going to be back into the market later this year, and I will update this page accordingly.

01.2014 => 05.2015

| ETF | ISIN | Symbol | Percentage of portfolio |

|---|---|---|---|

| iShares Core CHF Corporate Bond (CH) | CH0226976816 | CHCORP | 40% |

| iShares Swiss Domestic Government Bond 7-15 (CH) A | CH0016999861 | CSBGC0 | 20% |

| iShares Global High Yield Corp Bond CHF Hedged UCITS | IE00B988C465 | GHYC | 10% |

| iShares SMI (CH) A | CH0008899764 | CSSMI | 10% |

| iShares MSCI World CHF Hedged UCITS ETF | IE00B8BVCK12 | IWDC | 20% |