I got this email from Claire a few weeks ago:

Hi MP,

Thanks for the blog and your book, which I really enjoy.

Like many people discovering the FIRE movement, I want to buy ETFs for the first time and I have a significant amount to potentially invest (more than CHF 50'000).

From what I’ve heard, it’s better to spread out purchases over time (for example over several months). I can’t find clear advice online. I assume it’s a pretty common problem. Can you give me your take or point me to some articles?

Thanks a lot and have a great day.

I get this question all the time. And I get the paralysis, because I had the exact same hesitation.

When we bought our house, we kept all our cash aside for the down payment. Investing it in the stock market before that? Too risky. But a few months after getting the keys, we had about CHF 30'000 available to invest. And then came the paralyzing question: “What if the market is at its peak? What if I put everything in and the market crashes next week?”

So here’s my answer: invest it all at once. DCA on money you already have in cash is market timing in disguise. The economic research is nearly unanimous: lump sum investing beats DCA about two-thirds of the time.

You’re not investing for next week. You’re investing for 15-20 years from now. And over that horizon, the exact moment you get in matters way less than simply being invested.

What is Dollar Cost Averaging (DCA)?

As a reminder, on this blog, we invest in the stock market for the long term through low-cost, globally diversified ETFs. No stock picking, no day trading (and 1-5% max in crypto-casino, if you really want to have fun).

Dollar Cost Averaging (DCA), also called systematic investing or periodic purchases, is an investment strategy where you invest a large amount in regular installments, for example every month, instead of putting it all in at once. It’s primarily a behavioral strategy: the idea is to smooth out your purchase price and reduce the psychological impact of short-term fluctuations.

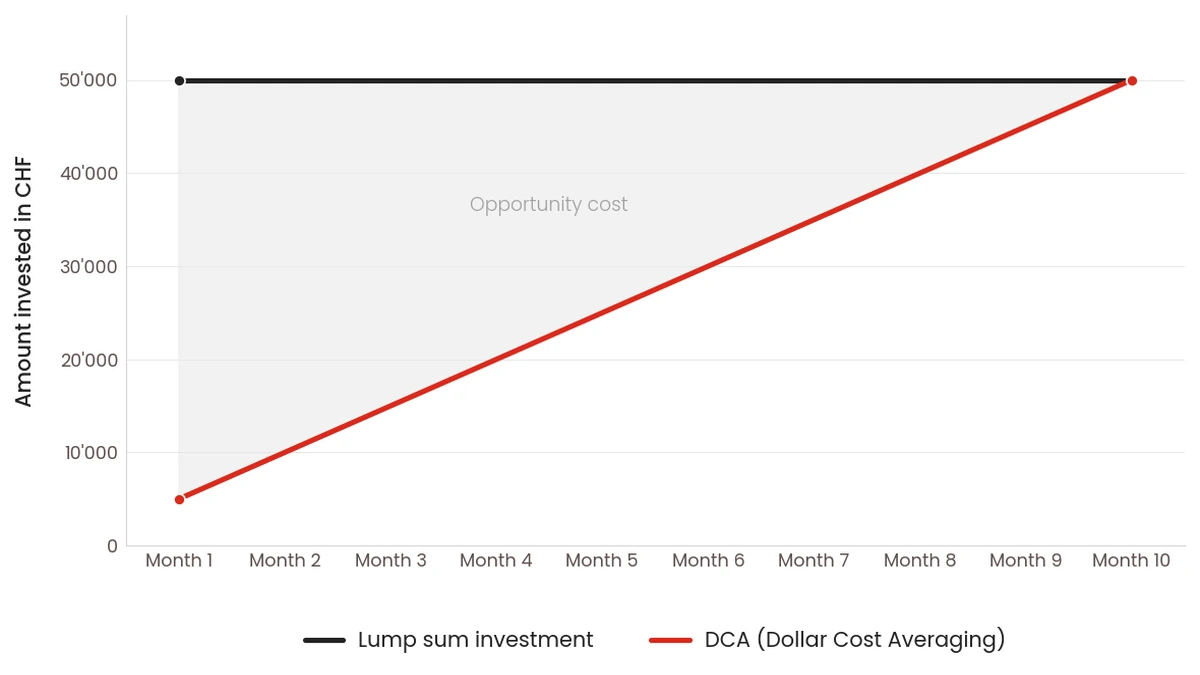

Let’s go back to Claire’s example:

| Month | Lump sum | DCA (CHF 5'000/month) |

|---|---|---|

| Month 1 | CHF 50'000 invested | CHF 5'000 invested |

| Month 2 | CHF 50'000 | CHF 10'000 |

| Month 3 | CHF 50'000 | CHF 15'000 |

| Month 4 | CHF 50'000 | CHF 20'000 |

| Month 5 | CHF 50'000 | CHF 25'000 |

| Month 6 | CHF 50'000 | CHF 30'000 |

| Month 7 | CHF 50'000 | CHF 35'000 |

| Month 8 | CHF 50'000 | CHF 40'000 |

| Month 9 | CHF 50'000 | CHF 45'000 |

| Month 10 | CHF 50'000 | CHF 50'000 |

With a lump sum investment, your money is 100% at work from day 1.

With DCA, you stay partially in cash for 10 months. On average, only about CHF 25'000 is actually invested.

So if the market goes up during those 10 months, you miss part of the gains. And if the market drops, DCA softens the psychological blow.

Don’t mix things up: investing your salary each month when you receive it is not DCA. That’s simply investing what you have when you have it. The DCA we’re talking about here is when you already have the cash (an inheritance, a bonus, accumulated savings) and you voluntarily choose to delay part of the investment.

DCA vs lump sum investing: what does the research say?

This question has been studied by economists for almost 50 years. And the answer always points in the same direction.

The economic theory

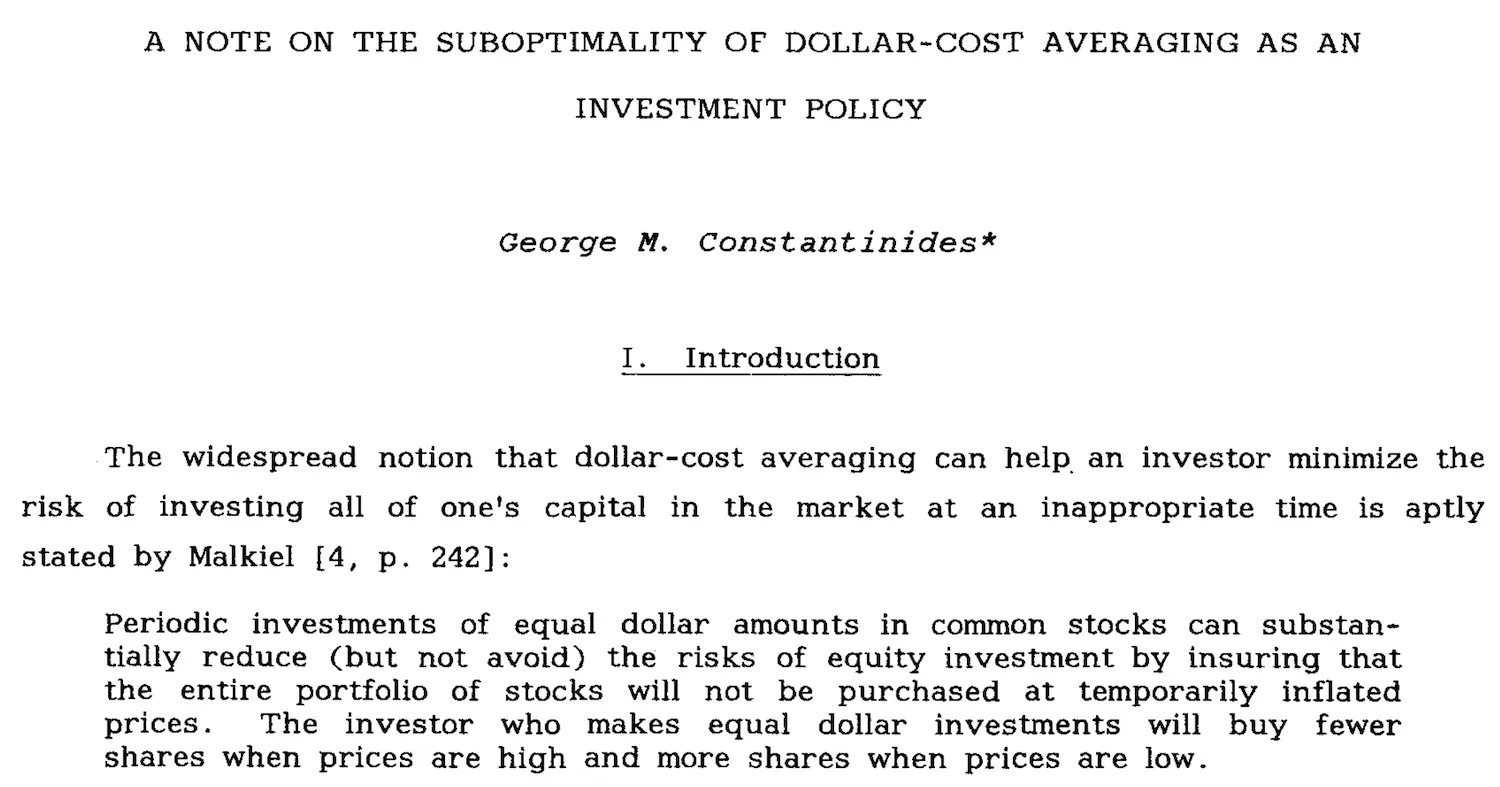

In 1979, Constantinides was the first to formally prove that DCA is mathematically suboptimal 1. In plain English: if you have the cash and want to maximize returns, delaying investment is always a losing move.

Brennan & Solanki confirmed this in 1981 2. Rozeff strengthened it in 1994: after adjusting for risk, lump sum investing is always superior as long as the market has a positive equity risk premium (meaning stocks earn more than cash over the long run, which has been the case for over a century) 3. And Milevsky & Posner (1999) reached the same conclusion using a completely different mathematical approach 4.

Four teams, four approaches, same verdict: DCA is suboptimal.

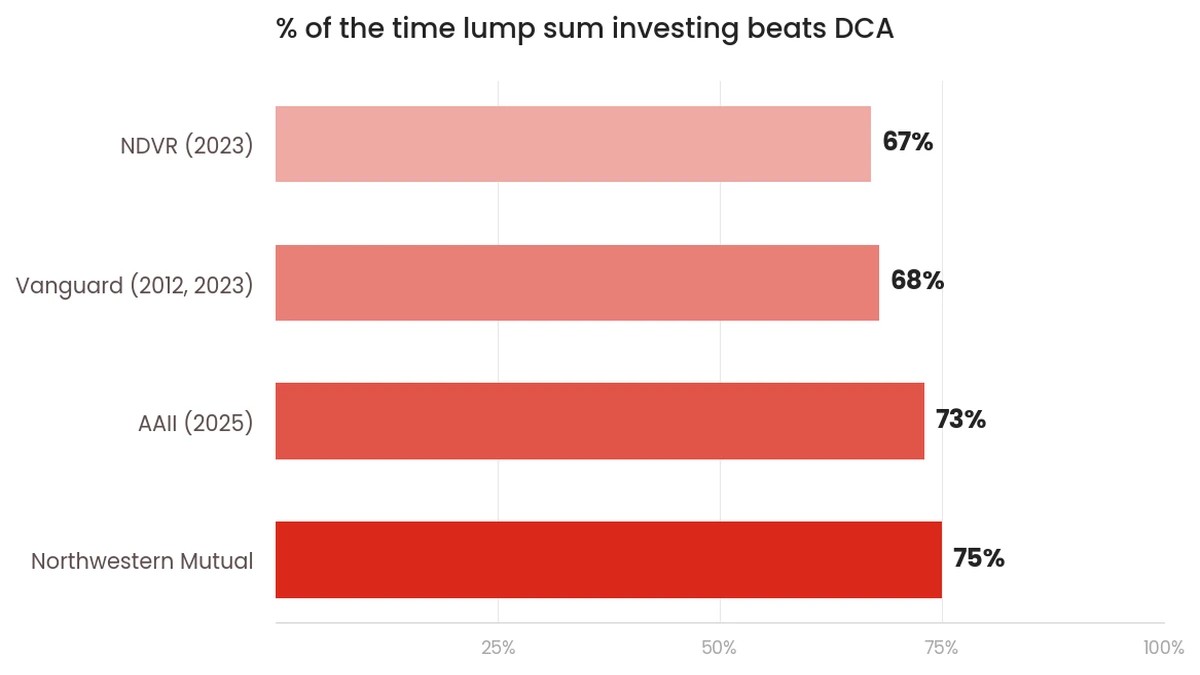

The hard numbers: lump sum wins 2/3 of the time

Theory is great. But we want numbers. And Vanguard did the most comprehensive work here (when I tell you they’re a solid company, these are the people behind the VT ETF!).

In 2012, Vanguard published the most cited study on the topic 5. They compared DCA vs lump sum across three markets (USA, UK, Australia). Result: lump sum investing outperforms DCA about 2/3 of the time. And with a DCA spread over 36 months? Lump sum wins ~90% of the time.

In 2023, Vanguard updated their data using the MSCI World Index from 1976 to 2022 6. Nearly identical result: 68% of the time, investing everything at once beats DCA measured after one year. The longer the DCA stretches out, the higher the opportunity cost.

Other studies converge:

| Source | Method | Lump sum wins… |

|---|---|---|

| Northwestern Mutual | Rolling 10-year returns | 75% of the time |

| AAII (2025) | Rolling 20-year periods since 1926 | 73% of the time |

| NDVR (2023) | Historical simulations | 67% of the time |

The fundamental reason is simple: markets go up more often than they go down (if you need convincing on this point, read this article: “The market always goes up”). Keeping cash while doing DCA means you’re statistically buying at progressively higher prices.

Why do so many people still use DCA?

Because the fear is real. And it’s well documented.

Imagine: you invest your CHF 50'000 all at once. 10 days later, the market drops 8%. Here’s what happens in your head:

- You panic

- You sell to “limit the damage”

- You wait for things to “calm down”

- The market rebounds, but you keep waiting, you want to be “sure”

- You reinvest once the rally is confirmed, and you buy back in at a higher price than you started

This scenario isn’t fiction. Statman documented it in 1995 7: the real risk of investing a large sum all at once isn’t the temporary dip. It’s your emotional reaction that makes you exit the market at the worst possible moment.

The stock market is like the ocean: sometimes it’s calm, sometimes it’s rough. The idea is to learn to surf it, not to struggle and risk drowning.

And the numbers back it up: according to NDVR (2023) 8, in the worst third of historical scenarios, DCA does protect better. A $100 investment could drop to $57 in the worst case with lump sum, compared to $74 with DCA. That’s not nothing.

But be careful with the conclusion you draw from this. The real risk isn’t investing right before a dip. The real risk is:

- staying in cash for years out of fear

- trying to wait for “the right moment” (which doesn’t exist)

- investing and then panicking at the first correction

There’s also an angle that rarely gets mentioned: the people recommending DCA to you don’t always have your best interest at heart. Like a Swiss insurer selling you a 3rd pillar tied to a life insurance policy, or a private bank charging fixed fees per transaction, they have every incentive for you to make 10 purchases instead of one.

So yes, DCA is better than not investing at all. It’s emotional insurance, and like any insurance, it comes at a non-trivial cost (about 2% less return over the DCA period 5 6, or roughly CHF 1'000 on a CHF 50'000 investment spread over 10 months).

But the important point is elsewhere: your Mustachian goal is to adjust your psychology to match the right strategy, not the other way around.

Because the stock market is like the ocean: sometimes it’s calm, sometimes it’s rough. The idea is to learn to surf it, not to struggle and risk drowning.

FAQ on Dollar Cost Averaging

What if I’m too stressed to invest everything at once?

DCA is better than not investing at all. But the goal is to build your investor muscle, not to avoid the gym altogether.

What if I invest right before a crash?

Even if you invested at the worst possible moment (September 2007), you’d have been in the green after about 5 years. Time in the market beats timing the market.

What’s the difference between DCA and investing your salary every month?

They’re two different things. Investing your salary each month is simply investing what you have when you have it. The DCA we’re talking about here is when you already have the cash and choose to delay the investment.

Conclusion: DCA or lump sum?

Whether you have CHF 50'000 to invest because you just realized your cantonal bank’s “investment solutions” are costing you a fortune and you want to reinvest through the best online trading platform Interactive Brokers, or you received an inheritance, or a gift, the answer is the same: invest it all at once.

And if it drops the next day, remember why you’re investing: for 15-20 years from now, not for next week.

That’s what I do with our ETF portfolio: as soon as cash is available, it gets invested. No calculations, no hesitation.

And if you’re still picking your broker, I compared the options in the best trading platform in Switzerland.

And you, do you invest using DCA by spreading out your investments, or do you go all in at once?

Constantinides, “A Note on the Suboptimality of Dollar-Cost Averaging as an Investment Policy”, Journal of Financial and Quantitative Analysis, 1979 ↩︎

Brennan & Solanki, 1981 ↩︎

Rozeff, “Lump-Sum Investing Versus Dollar-Averaging”, Journal of Portfolio Management, 1994 ↩︎

Milevsky & Posner, “A Continuous-Time Re-Examination of the Inefficiency of Dollar-Cost Averaging”, SSRN, 1999 ↩︎

Shtekhman, Tasopoulos & Wimmer, “Dollar-Cost Averaging Just Means Taking Risk Later”, Vanguard Research, 2012 ↩︎ ↩︎

Finlay & Zorn, “Cost Averaging: Invest Now or Temporarily Hold Your Cash?”, Vanguard Research, 2023 ↩︎ ↩︎

Statman, “A Behavioral Framework for Dollar-Cost Averaging”, Journal of Portfolio Management, 1995 ↩︎

NDVR, “Time In vs. Timing the Market”, 2023 ↩︎