In two years, I went from “real estate in Switzerland is just out of reach” to signing a mortgage at 80% on a brand-new apartment in Zurich, with CHF 70'000 negotiated off the price. Today, my wife is quitting her job to watch our kids grow up. But we also nearly made two big mistakes along the way. Here’s how it happened.

My name is Cédric. I was born and raised in France, and studied there. I moved to Switzerland 10 years ago, when I was 25, for work. I didn’t really know Switzerland, how it works, or even the variety of languages spoken here. But I got a unique career opportunity, so I went for it and landed in Zurich.

I was charmed by the country very quickly: the rigor, the reliability, the safety, and the beauty. That’s why I’ve stayed so long and don’t plan on leaving anytime soon. But at the start, it’s pretty disorienting. Sorting glass by color, putting cardboard out in front of your house, buying specific trash bags…

Everything works differently from France and nobody guides you when you arrive! With my roommates, we’d make a game out of it: “This magazine is plastic-coated, so what’s your bet, paper bin or regular bin?”, then we’d check together on the official website.

OK, these examples are pretty basic.

Then at work they start telling you about the 2nd pillar… What’s that?

And how do taxes work? Thankfully, with my B permit, taxes are withheld at source so I have nothing to worry about. Wait, what? I should declare my pillar 3a? Hold on, how many of these pillars are there?

Another big example: real estate. In France, owning your home is just the baseline. Once you start working, you save for that, and as soon as you’ve got a bit of capital you buy and stop bleeding money on rent.

Being a typical Frenchman, I quickly started looking at apartments in Zurich.

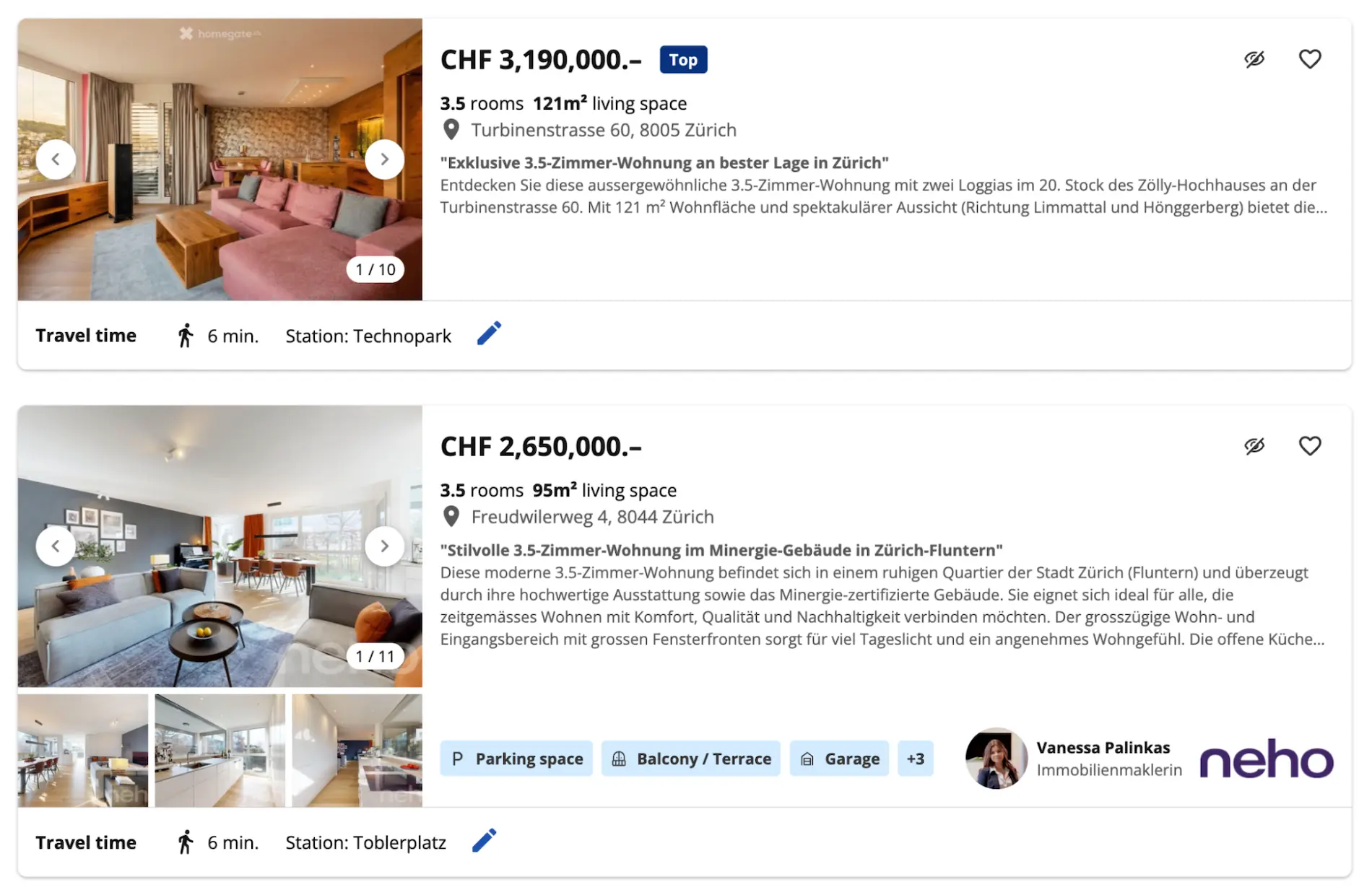

I still remember the very first apartment I looked at on Homegate: two bedrooms, 75 m², fairly recent, in the outskirts of Zurich about 20 to 30 min from the center… CHF 1'700'000 !!!

WHAT!??

These Swiss people are crazy!!

I told my roommate about it, still in shock. He said:

Haha, yeah, I told you, that’s why the Swiss don’t buy! Here, most people never own their home, they rent their whole life.

Oh, OK, weird, that’s sad but that’s how it is. I closed my laptop and gave up on the idea…

It took me a while to learn all this stuff as I went.

At some point I even thought I had it all figured out, and I made peace with the idea that real estate would always be out of reach for me. But that was before reading MP’s book.

The Father’s Day that changed everything

I met and married my wife in Switzerland.

Today we have two beautiful kids.

In June 2024, for Father’s Day, my wife gives me a strange book titled “Free by 40 in Switzerland”.

My first reactions:

- I don’t like reading

- I’ll never have time to read this brick of a book

- I HATE anything to do with finance

- But hey, it’s the first Father’s Day gift of my life so “Thanks honey, that’s so sweet!”

To be honest, this gift didn’t really come out of nowhere. My wife had been bugging me about this Mustachian thing for a long time.

Her ex was the one who got her into it…

That’s maybe why I had never dived in, or maybe because I thought I already had my finances under control.

But she knew my logic and discipline would make me buy in if I gave it a chance.

And she was right!

Once I dived into this book, I couldn’t stop!

The very concept of FIRE was completely unknown to me until then. The idea of choosing your own retirement age when you have a job that doesn’t pay you millions every year had never even crossed my mind.

I read later that what I experienced reading the first chapters is called a “paradigm shift”.

I devoured the book in two or three weeks. I felt like a gladiator who had just learned that by surviving long enough in the arena, I could earn my freedom.

What I learned from this book is immeasurable.

First, that yes, I actually did have time to read a book (I started reading a lot more after that, including “Rich Dad Poor Dad”, which also opened my eyes a ton).

Second, that finance isn’t actually that hard… especially all the inner workings of the Swiss financial system: how it works, how to optimize it, and how to take advantage of it.

And guess what: being a homeowner in Switzerland is actually possible!

Since I discovered the book at 34, I never expected to be FIRE by 40.

Plus I’ll be honest, I really love my job and probably don’t want to leave it anytime soon.

What got me hooked was all the Switzerland-specific lessons, all the stuff I described earlier as so disorienting.

With all this new knowledge, I set two goals for us:

- Buy our own apartment

- Optimize our finances so my wife and I wouldn’t have to work full-time and could spend more time with the kids

A year later, we were homeowners.

Today, two years later, my wife is quitting her job to watch our kids grow up.

A decent financial upbringing… but with a blind spot

I was lucky to get a really good upbringing on how to manage my money. My parents always taught me not to spend pointlessly. I wouldn’t say it’s Mustachian-level frugality, but not far off.

The idea is to save as much as possible on big expenses, buy little but buy quality, and save as much as possible while still allowing yourself small pleasures.

With that upbringing, I managed to put away between CHF 200'000 and CHF 300'000 over the first 35 years of my life.

Sounds good, but that number could have been SO much bigger if I had read MP’s advice earlier, especially about investing in the stock market.

Because yes, my parents had some really bad investment experiences and their only advice was:

Never invest!

Put everything in a bank, on an account with the best interest rate you can get, and that’s it.

(In their defense, back in their day, bank interest rates could hit 5%, while today it’s hard to find even 1%.)

Anyway, CHF 200'000 was enough for a mortgage, so we started looking for an apartment.

How we bought our apartment in Zurich

We went all-in for 5 months, almost signed 2 bad deals (more on that in a sec) before finally finding a nice new build, in a village perfect for raising two kids, with a direct train to my office.

We signed in November 2024 (six months after getting MP’s book), and we moved in June the following year. Today, we’re over the moon and saving a lot of money every month. All thanks to MP’s book!

I know Mustachians love numbers, so here goes:

- Our new apartment, with the parking spot, cost CHF 1'305'000. We managed to negotiate it down to CHF 1'235'000. Then, since it was a new build, we couldn’t help upgrading some materials and adding things for a total of CHF 40'000. Final total cost: CHF 1'275'000.

- Crédit Agricole Next Bank agreed to finance us at 80% on a SARON with a negotiated margin of 0.65% and indirect amortization through the 3rd pillar.

- Quick anecdote: one of the first things the banker offered me was a 3rd pillar tied to a life insurance policy… Thanks to MP’s warnings, I was able to look her straight in the eye and say “NO” flat-out in a sharp tone. She looked a bit intimidated and didn’t push it. It’s probably a scam I could have fallen into before reading all the warnings on MP’s blog.

- So our down payment was CHF 255'000, which includes CHF 75'000 pulled from my 2nd pillar.

- Today, with a SARON rate at 0%, we pay CHF 550 a month on the mortgage, plus utilities on top. Before that, in our much smaller previous apartment, we paid CHF 2'800 in rent. You can imagine the difference!

We were really lucky to be able to negotiate CHF 70'000 off the price. That’s huge!

The development was actually made up of two buildings with a total of twelve 4.5-room apartments, and four 5.5-room apartments. We were originally interested in one of the 4.5s with an attractive price around CHF 1'000'000. Unfortunately the building right across from it was way too in-your-face. And just as we were about to give up, we noticed that while the 4.5s were selling well, none of the 5.5s had found a buyer yet…

That’s probably a stressful situation for a developer, a few months from finishing the project.

We used that leverage, plus the fact that we were originally planning to buy a much cheaper unit from them (the 4.5), to negotiate the price down. To be honest, we tried it without really believing it would work. We were incredibly lucky that it did, especially since the other three 5.5s sold very fast afterwards.

The two bad apartment deals in Zurich we dodged

A first apartment that was too noisy

I also want to tell you about the two bad deals we almost signed, because I think you can pull some lessons from them for your own home-buying journey in Switzerland.

The first, also a new build, was love at first sight! A big rooftop with a beautiful view of the river. Unfortunately it was right next to a railway crossing. We asked ourselves a lot of questions about how much noise it might cause. We studied the question in detail (number of trains per day, how loud they are, height of the noise barrier wall, etc.).

The situation was relatively acceptable given how much we loved that apartment…

But while we were trying to listen to the train noise, it was the small road right next to it that caught our attention.

Why on earth was there nonstop traffic?

Looking online, we found out that this small road was THE connection point between the highway linking the North to the West of the region and the one linking the East to the South. So every vehicle, including trucks, heading South from Germany passes through there. And that, unfortunately, was not acceptable.

A geothermal heating system that wasn’t ours…

The second Zurich apartment was another nice new build (yes, yes, we like new builds).

It was super charming with a pretty view over the fields.

The price was reasonable and we were ready to sign.

Before doing that, we still asked my wife’s uncle, an experienced construction engineer, to take a look at the contract.

What he saw was going to cost us a lot…

Turns out the geothermal heating we loved so much wasn’t ours, since it was leased from the electricity company that maintained it.

And that lease would have cost us more than CHF 50'000 over 30 years!

Given this new piece of info, we tried to negotiate the purchase price, but it didn’t work and we had to walk away.

Up next: rental investing in Switzerland

This experience with our primary residence was very positive and gave us a lot of confidence in managing our finances. On top of that, lots of small optimizations here and there (best Swiss 3rd pillar, cashback credit card, free bank accounts, etc.) that add up fast to nice savings.

Today, we want to keep going on our real-estate journey and buy to rent. I followed MP’s program “How to invest in rental properties in Switzerland” for that.

Once again, MP gives you the keys to avoid paralysis. Paralysis from ignorance, then paralysis from too many decisions. We still have a lot to learn and research, but I hope we’ll get started soon. Exciting stuff!

There’s one area where I really struggle to get started, though. The stock market.

Investing in stocks… easier said than done!

I followed MP’s tutorials and opened an Interactive Brokers account (IB), and invested a bit of money (around CHF 30'000) in the VT ETF.

But I can’t bring myself to invest bigger amounts.

I’m stuck.

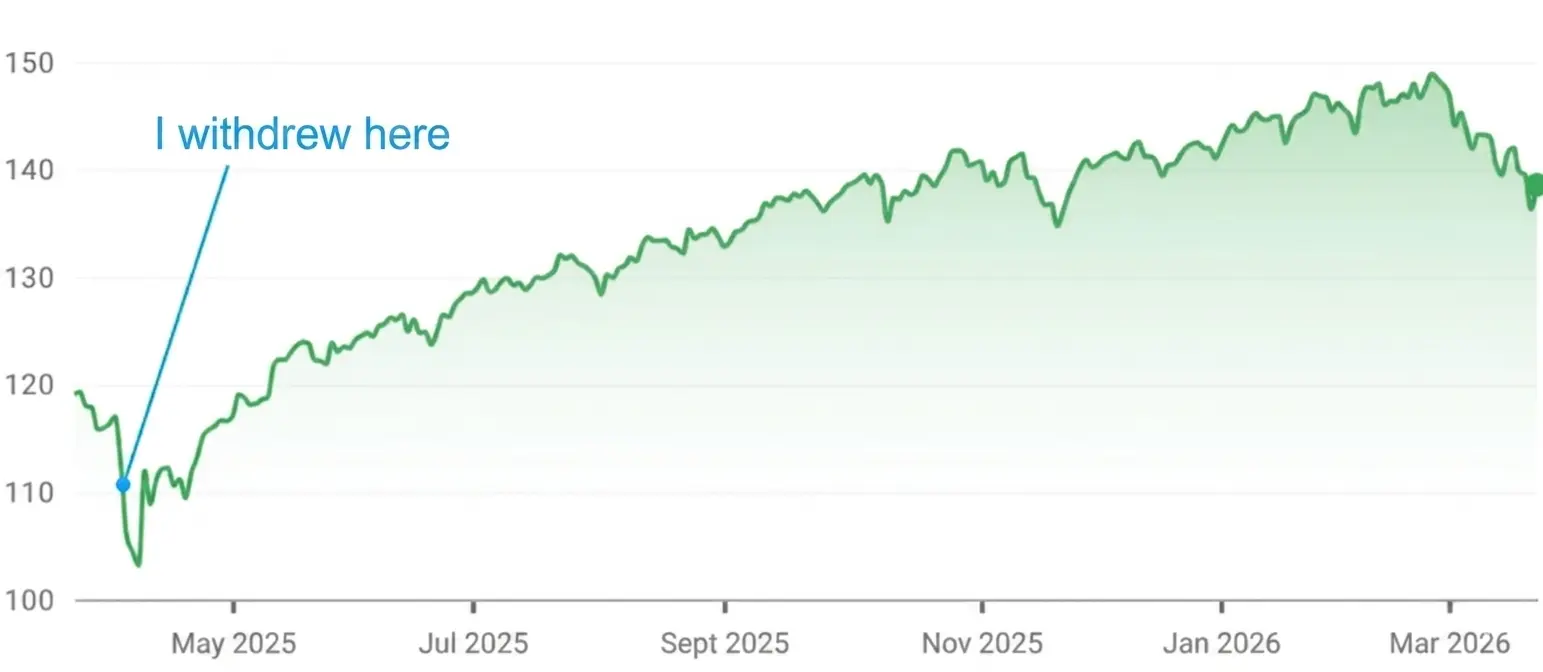

It comes from several things: my parents’ upbringing, past bad investment experiences, the likely need for big amounts in the short/medium term if we go into rental real estate, Trump and the current state of the world, neither of which I trust, and the April crash that traumatized me…

When Trump started cranking up import tariffs left and right in April 2025, I read everywhere that the dollar was going to crash and lose up to 50% of its value. Which means even if the VT ETF stays stable, I lose 50% of my net worth. So I did exactly what you’re not supposed to do, I panicked, pulled everything out, and converted back to CHF.

The dollar didn’t actually crash, and the VT ETF had an exceptional year.

I’d rather not calculate how much I lost by pulling everything out.

It’s really tough mentally!

I spent weeks glued to IB every single day and I really didn’t feel good. I’m still stuck today. There’s a new war breaking out every day and I have this feeling the market is going to crash again the moment I reinvest…

My 3rd pillars, on the other hand, are fully invested in stocks and doing well, so at least there’s that.

I hope I’ll be able to share our progress soon on the rental real-estate side (and maybe stock investing too). I’m really happy with how far we’ve come since that famous Father’s Day that changed everything, and there’s plenty of good stuff still ahead!

What I would tell my 20-year-old self

If I could talk to my 20-year-old self, I’d tell him not to treat finance as a taboo subject or as an overly complicated task.

Unfortunately, our education system doesn’t give us the keys to take charge of our finances. It’s basic stuff, and yet they don’t find it useful to teach.

It drives me crazy!

That said, there are tons of resources out there, whether it’s books, blogs, podcasts, etc., and it’s worth educating yourself. Honestly, it’s not that hard, you just need to put in a bit of time to understand how it works and learn the mechanics.

My mistake with my finances at 20 wasn’t carelessness or procrastination, it was just ignorance. I genuinely thought I was doing the right thing. I was following my parents’ advice, saving, and spending responsibly. I was convinced everything was perfectly under control, so educating myself further on the topic wasn’t even something that crossed my mind.

What MP’s book taught me is very important: taking charge of your finances is accessible to everyone. It’s really not complicated, you just have to put in a bit of time. And the long-term impact is huge.

And the real question is: how many Swiss people miss out on their financial freedom just because nobody told them it was accessible?

Header image credit: Ivo Scholz / myswitzerland.com

Last updated: June 4, 2026