I thought that with a SARON mortgage, I could switch banks every 3 months when the rate reset… and so be free to optimize my finances by always picking the best rate… What a rookie mistake. The truth is, you’re just as locked in with a SARON mortgage as with a fixed-rate one, only for a few years less.

From my (truly awful!) 10-year fixed mortgage to SARON

When we bought our home a few years ago, I still had very little experience with mortgages.

And since we’d found our dream place, emotion took over. That, plus the stressful FOMO timing, because we felt like we’d never find a place like it again…

So I went around to all the mortgage providers, namely the banks and the insurers… (ugh, it hurts to reread that last word). And of course, as a young guy who didn’t know much yet, I focused on the same thing everyone does: finding the lowest possible mortgage rate in Switzerland.

And of course, insurers almost always offer the cheapest mortgage rates… Why? Simply because they make their money on the worst financial product (a scam!!) still legal in Switzerland: the pillar 3a tied to a life insurance policy.

Long story short, we got suckered into signing with that insurer. On top of that, they managed to get me to close my old pillar 3a (already tied to a life insurance policy) and sign up for a new one, also tied to a life insurance policy… pretty embarrassing for a personal finance blogger…

And you see, with a 10-year fixed-rate mortgage, you can sign now and you’re all set for a decade… it’s reassuring to know the rate won’t keep changing.

— Our

insurance agentrug salesman at the time

An insurance agent sells me a 10-year fixed-rate mortgage and a pillar 3a tied to a life insurance policy

Then I learned from my mistakes and managed (after some intense contract negotiations) to close that whole mess and move to a SARON mortgage. Yeah! (the full story is here: Closing a mixed pillar 3a (and early termination of a 10-year fixed mortgage!))

But I still had a few things to discover…

SARON mortgage: the best choice for a Mustachian

The further I went with my Mustachian approach, the more I discovered how to optimize my finances.

And the mortgage was no exception.

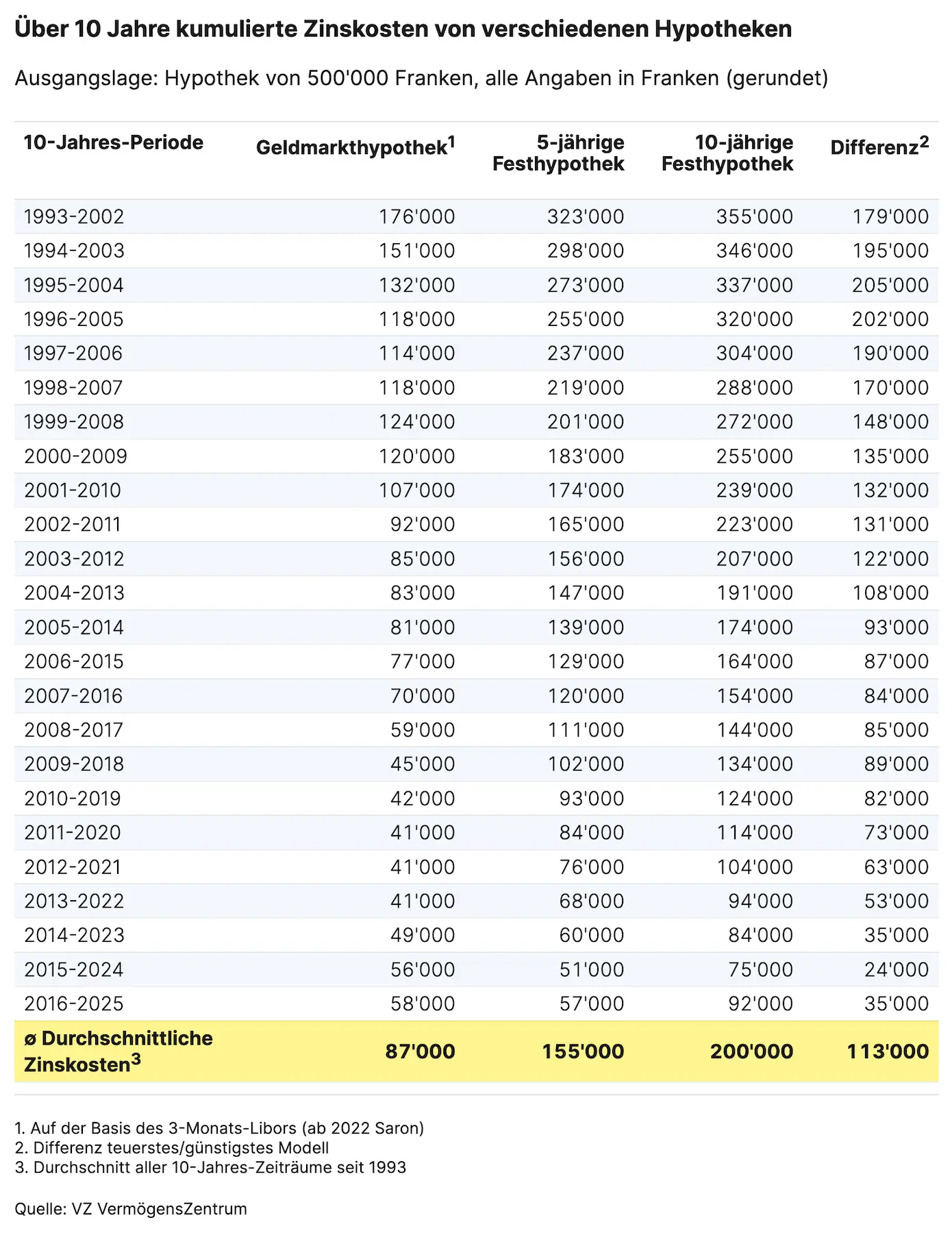

Reading tons of articles, I realized that over the last 30 years (that is, since the early ’90s), the SARON mortgage beat the fixed-rate mortgage (5 or 10 years) almost every single time.

And over a decade, we’re talking about a difference in interest paid of tens of thousands of Swiss francs. That’s huge!

But insurers and banks scare you by telling you it’s complicated, that the interest rate changes every 3 months, and so on. Their pitch is well-rehearsed… simply because they make more money off you by selling you a fixed-rate mortgage.

SARON (short for Swiss Average Rate Overnight) is an official Swiss interest rate, based on what banks lend each other from one day to the next. In plain terms: it's a market rate, not a number your bank pulls out of a hat.

It replaced the old LIBOR rate (London Interbank Offered Rate), the same kind of rate but run out of London, retired at the end of 2021 (partly because some banks got caught manipulating it). Since 2022, all new variable-rate mortgages in Switzerland are SARON mortgages.

And concretely, when we say the SARON rate, we mean two pieces:

- the SARON rate, which moves with the market (usually recalculated every 3 months)

- and a fixed margin from your bank on top (generally between 0.9% and 1.5%, and negotiable depending on your profile)

The SARON rate changes every quarter, and the second one doesn’t budge for the whole contract.

And here you’re thinking: “But wait, so my contract renews tacitly every quarter, but can I also stop it whenever then?”

Can you switch your SARON mortgage whenever you want?

For a long time, I honestly thought this SARON setup was a no-strings-attached deal.

My reasoning: if the mortgage rate gets recalculated every 3 months, then I can cancel and take my business elsewhere at each reset.

So I figured I finally understood why banks prefer to lock you into a fixed-rate mortgage for many years.

Except… no, the reality is quite different.

The real SARON rule: framework contract, notice period, penalties, and tacit renewal

What they forget to tell you is that your SARON mortgage is tied to a framework contract (the famous “Rahmenvertrag”, in good Swiss German). And that’s what locks you in, not the rate.

The rate, sure, it changes every 3 months. But the framework contract has a fixed term: generally between 1 and 5 years (often 2 or 3). At VIAC and Bank WIR, for example, it’s 3 or 5 years. So for that whole term, you’re committed. Just like with a fixed mortgage, only over a shorter period.

And even at the end of the term, you don’t just walk out overnight. There’s a notice period to respect, usually 3 to 6 months. Except it varies wildly from one lender to another: at UBS, it’s 13 months’ notice for their standard SARON, versus 1 month for their Flex version. In other words: read that clause BEFORE you sign, not the day you want to leave.

And if you want to break your mortgage before the end of the framework contract? You pay. It’s called the early termination penalty, and it’s calculated like a fixed mortgage: roughly, the gap between your rate and the market rate at the time you leave, multiplied by your mortgage amount and by the years you had left. Plus processing fees, of course.

A concrete example courtesy of UBS: CHF 500'000 mortgage, 1% rate gap, 3 years left, that’s CHF 15'000 in penalty. But the upside with a SARON mortgage is that the final bill is usually gentler: the remaining term is short, and the calculation is mostly based on the margin you had left to pay, not the entire rate. Still, it exists, and that’s worth knowing.

An often-forgotten little consolation: switching from your SARON to a fixed rate with the same lender is generally possible at any time, and free of charge. The penalty mostly kicks in when you want to move to a different bank entirely before the term. But hey, as Mustachians, we’re not too keen on a fixed-rate mortgage anyway ;-)

And the last trap, the sneakiest one: tacit renewal. At the end of your framework contract, if you don’t cancel within the deadlines, many contracts automatically roll over for another round. And there you are, locked in again for a few years without meaning to… and watch out, at that exact moment your margin can also be repriced (up or down), whereas mid-contract the bank can’t touch it.

So the reflex to build from the moment you sign: note the end date and the notice period in your calendar, with an email reminder something like 4-8 weeks ahead (because yes, when you get that reminder, your upcoming weekends will probably already be packed, I speak from experience haha). It costs you 30 seconds, and it saves you from getting auto-renewed against your will.

Bottom line, on paper, SARON locks you in almost as much as a fixed mortgage. Except that my experience with Bank WIR (via VIAC) showed me that between what’s written in the contract and what actually happens, there’s sometimes a big difference…

My SARON mortgage experience with VIAC and Bank WIR

One thing you shouldn’t forget in all these personal finance and optimization discussions is the human relationship. And the trust you build over time.

For context, I chose to get my SARON mortgage through VIAC (and their partner Bank WIR) because at the time, they were the only ones willing to pledge my pillar 3a at 100% of its value, even though it’s invested 100% in stocks (and so has a value that swings quite a bit depending on how the market’s doing).

And while I was questioning my approach to financial independence, I wanted to know whether there was a risk of my borrower file being reviewed (I’ll save that for another article). And chatting with my advisor at the Bank WIR branch in Lausanne, he told me:

By the way, if you’d wanted to change anything about your SARON mortgage (switching mortgage type, terminating, etc.), you’d have had to wait 3 years because your contract tacitly renewed 2.5 weeks ago…

Then, on his own, he added:

But look, since you’re a long-standing client, we can talk it over and work something out at no extra cost if you still want to make changes.

So my takeaway: yes, the contract clauses exist, but the client relationship matters just as much (thankfully!). At least with some financial institutions around here, like the Bank WIR branch in Lausanne, from what I can tell.

What I would do today

So much for the theory and my SARON mortgage experience so far.

If I were buying my primary residence today, here’s the checklist I’d use:

- Go with a SARON mortgage no matter what, because it’s the most attractive option mathematically (compared to a fixed-rate mortgage)

- Quick reminder: NEVER take a mortgage from an insurer, because they’ll do everything they can to push a pillar 3a tied to a life insurance policy on you (that’s how they pay for their bonuses…)

- Before signing: read the commitment term, how the penalties are calculated, and the tacit renewal clause.

- Keep a good relationship with your bank advisor, and mean it

SARON mortgage FAQ

Can you terminate a SARON mortgage at any time?

No. The rate is recalculated every 3 months, but you stay committed for the length of the framework contract (often 2-3 years), with a notice period of 3 to 6 months depending on the lender.

How much does early termination of a SARON mortgage cost?

A penalty = (rate gap) × remaining term × amount, plus processing fees. The sum is usually modest given the short remaining term of a SARON, but it exists. Switching to a fixed-rate mortgage with the same lender is often free.

SARON or fixed rate: which should you choose?

For a Mustachian, SARON wins in almost every case: historically, it works out cheaper than a fixed rate (based on VZ data since 1993), as long as you keep a safety cushion to absorb the quarterly swings. A fixed rate is only really justified if rates go negative again, or if you can’t sleep at night with a rate that moves. All the details in my guide to choosing the best Swiss mortgage.

Does a SARON mortgage renew automatically?

Often yes, by tacit renewal if you don’t cancel within the deadlines. So set yourself a reminder the moment you sign.

Last updated: June 25, 2026