It’s time again to compare premiums of the compulsory health insurance plans to see if we’ll change insurance companies or not this year to maximize our frugal spending.

As usual, I used the best health insurance comparison tool in Switzerland on the official website of the Swiss Confederation “Priminfo” (and not Comparis or anything else that puts sponsored items in between results that you can quickly get screwed over).

In a nutshell: how do I change my compulsory health insurance in Switzerland?

Simply follow these four steps to conclude your new compulsory health insurance policy and terminate your current KVG/LAMal insurance:

- Check how much you’re currently paying in health insurance premiums

- Compare on priminfo which is the best health insurer for your personal data

- Subscribe to the new insurer (if you can find a cheaper one)

N.B. normally, the new insurer will ask you what your current health insurance is, so that they can send them a confirmation of affiliation, and so that your cancellation request can be accepted (see next point). - Send a cancellation letter (see template below) to cancel your current health insurance by registered mail

N.B. wait until you’ve received the confirmation email from your new insurer (you usually receive an application confirmation email a few minutes after registering online with the new insurer).

Reminder: health insurance choice of the MP family in 2025

Readers who have been following the blog for a long time know that we have been with Assura for several years now.

Then, in 2022, we switched to KPT, which had become the cheapest insurance for 2023.

And we switched again in 2024 to Visana (for us adults). And the children went to CSS.

This was the most frugal option we could find with our search criteria, namely:

- Mr MP and Mrs MP: deductible of CHF 2'500, family doctor model (to be able to choose our family doctor and not have him imposed on us)

- Children MP: deductible of CHF 0, family doctor model also

And in October 2024, we shopped around again. We switched back to Assura for us adults. The children stayed with CSS, which was cheaper. So we paid the following monthly basic insurance premiums to Assura and CSS:

- Mr MP: CHF 352.95

- Mrs MP: CHF 352.95

- Kid MP 1: CHF 116.45

- Kid MP 2: CHF 116.45

- Total health insurance in 2025: CHF 938.80/month

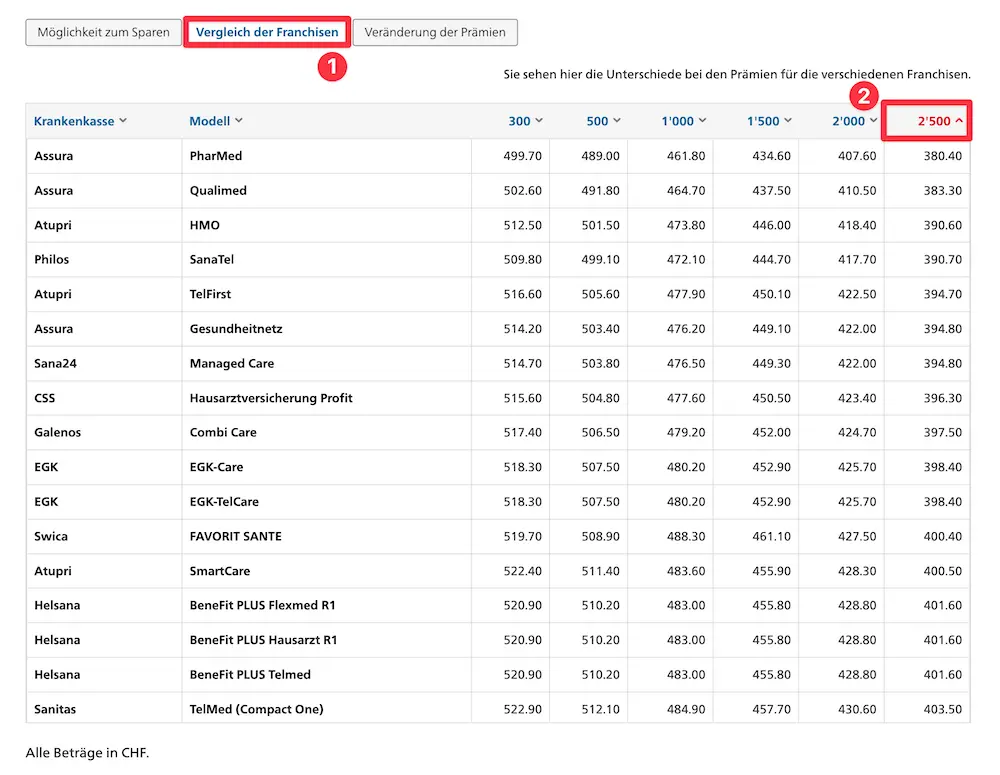

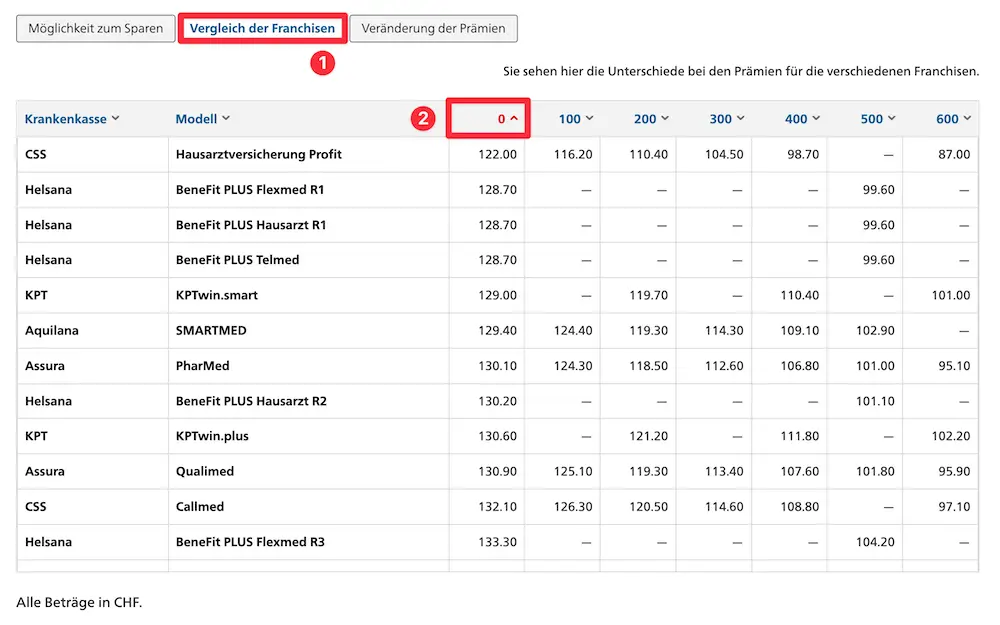

Using health insurance comparison tool priminfo

So I went to enter my info and that of Mrs. MP and the kids on the official federal “Priminfo” website to compare health insurance premiums:

Verdict health insurance premiums 2026 for the MP family

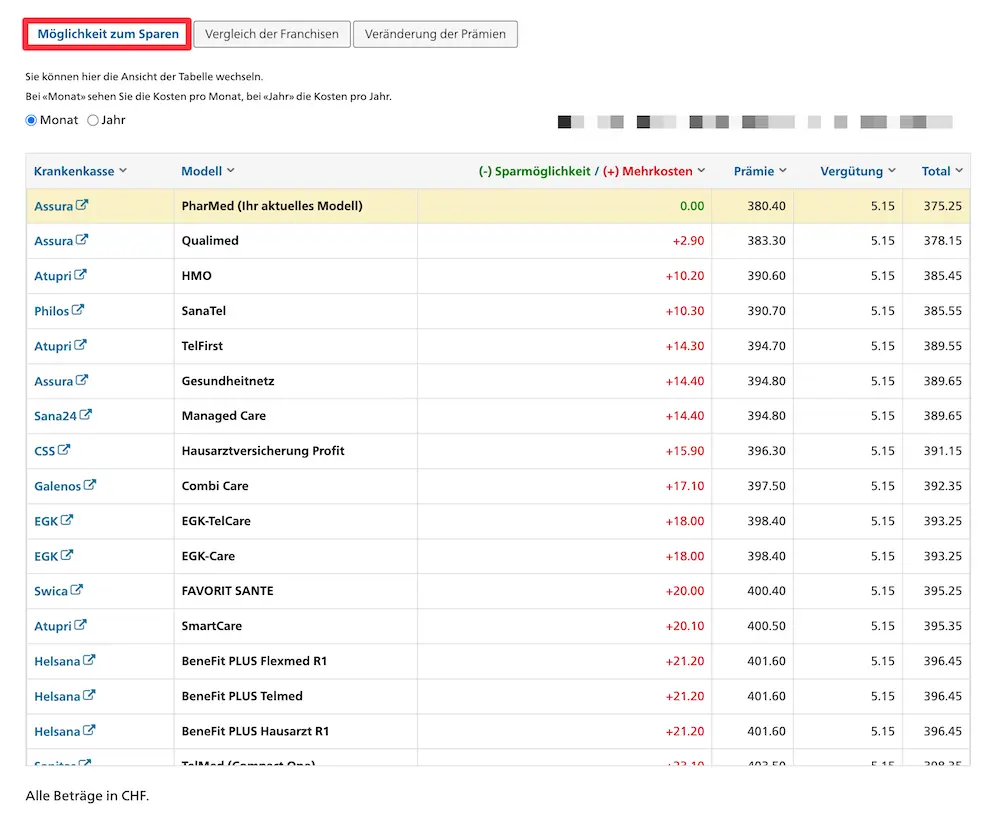

The results of this year’s comparison are obvious:

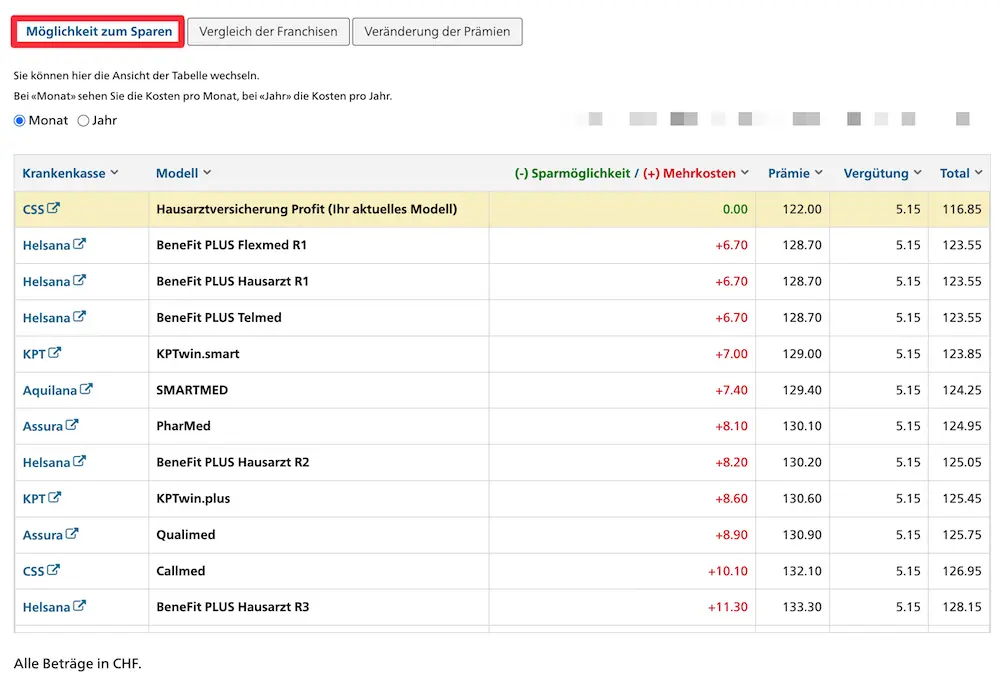

- ✅ Assura PharMed: We stay with the good old Assura basic insurance we’ve had for many years. PharMed gives us the free choice of our family doctor, but restricts our choice of pharmacies (we have to go through Assura’s partner pharmacies, and we have one near us, so all good).

Assura (PharMed) remains the most frugal insurance for Mrs MP and me in 2026.

- ✅ CSS Hausarztversicherung Profit (MP children): Our children will remain with CSS, as it is simply the cheapest basic insurance (compared to Helsana or Assura).

That’s what we’re talking about in numbers, monthly:

- Assura + CSS / MP family 2025: CHF 938.80

- Assura + CSS / MP family 2026: CHF 984.20

- Difference = CHF 45.40 more to pay each month!

It’s less crazy than the 25% between 2023 and 2024, but we’re still talking about a 5% increase 💸

But if we had been with CSS for us adults and stayed there, we would be paying CHF 62.60 more per month!

So, by switching to a new health insurance company in 2026, we would save CHF 751.20 per year (= 62.60 x 12).

And over 10 years, by investing this amount in the stock market via my favorite broker Interactive Brokers, that would make us CHF 11'121 more in our pocket!!!

All this is for the small effort of sending a registered letter to cancel my health insurance and filling in a small form to take out our health insurance with Assura for 2026!

That’s about 1 hour and 15 minutes of work, for a very nice yield in the end!

Sample letter to cancel KVG/LAMal health insurance

If you also want to cancel your KVG/LAMal health insurance (valid for all health insurance companies), here is a standard insurance letter that you just have to fill in, sign, and send by registered mail to your health insurance before 30.11.2025:

Download sample cancellation letter for health insurance (in German) >

Download sample cancellation letter for health insurance (in French) >

I must insist that you send this letter on time, otherwise your request to cancel your basic insurance will not be considered…

Conclusion

Honestly, it’s nice not to have to go through all those health insurance procedures again… But every time I compare health insurance plans, I feel nostalgic, because it reminds me of 2013 when I optimized all my health insurance contracts to become the Mustachian that I am today :)

And a little note about KPT then Visana: even though I’ve cancelled with them, I can confirm that it’s only because of the health insurance premium, because it’s always gone well, and I’ve always been very satisfied.

And you, are you cancelling your KVG/LAMal health insurance this year? If so, with whom? With the family doctor insurance model or another? And also, do you have any opinion on Assura, Visana, or CSS?

FAQ

Cancellation of supplementary insurance

You can normally cancel your supplementary health insurance at the end of each year, giving 3 months’ notice (i.e., by September 30 of each year at the latest).

What is the Federal Health Insurance Act?

It’s the law called “KVG” in German and “LAMal” in French. It regulates the benefits of the compulsory health insurance.

Last updated: October 16, 2025