UPDATE 13.01.2022

Click on the following link to see my updated comparison of the best Swiss bank as of today: “Best Swiss bank as of today”.

Zak has been my primary Swiss bank for a year now. As explained in my comparison of the best Swiss bank 2020, I chose Zak for three main reasons:

- They are well established (via the network of Bank Cler)

- I can deposit cash at their ATM for free

- They offer a Maestro debit card, convenient for when small stores in the countryside do not accept credit cards

Like all these neo-banks, there is only one mobile app with Zak. If it crashes, there is no web alternative. That’s why I made Neon my secondary bank.

This setup suits us well.

And what’s clear is that we haven’t regretted for a single moment having left BCV and the dubious practices of some advisors with their clients (cf. our mortgage experience).

Nevertheless, all is not rosy at Zak’s, and they could still improve many things. Here are the 4 positive and 4 negative things I observed after 1 year of use.

The 4 positive points about Zak

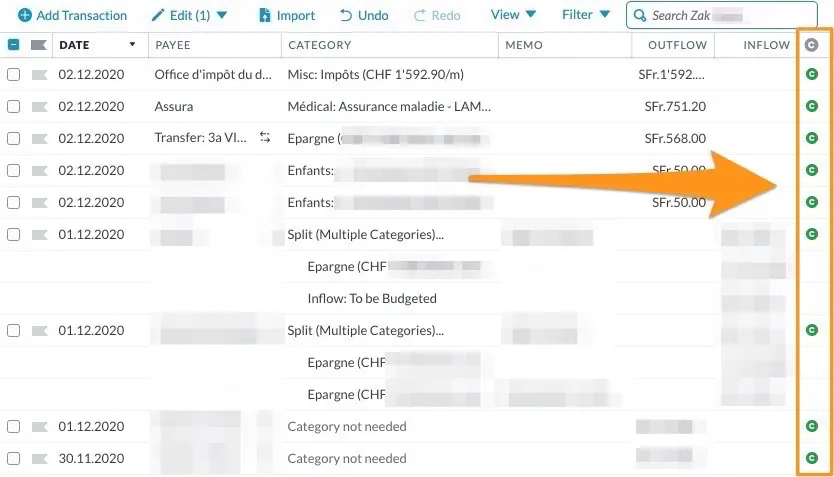

1. ✅ The pots feature to reconcile my budget

Being a big fan of my budgeting software YNAB, I need to reconcile my bank’s transactions with YNAB. Reconciling means having the same amount in YNAB and Zak.

In YNAB, it’s quite easy to track because I can mark each transaction with a small “C” (for “Clear”). Except that in many apps and e-banking, there is no such feature to “mark” a transaction.

Except with Zak.

Indeed, I hijacked their pot system to meet this need. Any new transaction (credit or debit) that happens on my Zak account automatically comes in the “Daily life” pot. In my system, this pot corresponds to transactions that have not yet been entered into YNAB.

When I reconcile my two systems, here’s what I do:

- I enter the transaction manually in YNAB

- I swipe the transaction in Zak to the right, and transfer it to the pot named “YNAB”

- Once the “Daily life” pot is empty, I find myself with YNAB and Zak which are reconciled with the same amount of money

Whether you are using YNAB or an Excel file as budget system, this pot mechanism will help you. It’s really handy!

Also, if you are just starting out in your working life, and you only have one Zak account (and therefore no budget as such), you can very well use the pot mechanism as your main budget system. It’s ultimately quite similar to YNAB where you assign CHF into each expense category, and where you know what you have left in each category at any given time.

2. ✅ Transfer limit increased to CHF 25'000/week

Honestly, it was starting to get annoying to have to “ask Dad (aka Zak)” when I had transfers that exceeded the limit of CHF 5'000/day or CHF 10'000/week.

It only happened once every 2-3 months when I wanted to transfer our savings to invest them via Interactive Brokers, for example, or when we had to pay our mortgage interest on top of all our other recurring monthly payments.

“Hello Dad, yes it’s Marc, could you authorize my transfer that exceeds CHF 5'000 please?” — no thanks!

According to Zak, since this neo-bank was aimed especially at young people, they thought that such a 5-10kCHF security barrier was more than enough. Which I can imagine. Except that since a large part of the Swiss Mustachian FIRE (Financial Independence, Retire Early) community has an account with them, I think they were fed up with getting phone calls all the time ;)

Anyway, for several months now, the limit has increased to CHF 25'000 per week. And I never had to call them again. O joy!

3. ✅ Push notifications

It’s a bit weird to write this in 2020, when every mobile app I use in my daily life offers this feature…

But in the end, if you compare to Neon (which still sends notifications via SMS — for free, fortunately!) or even worse to Cembra for my Cumulus MasterCard (which sends SMS, but only if you pay CHF 4/month!!!), well Zak is rather ahead on this point in Switzerland.

Indeed, I find it very convenient to have a live notification of when a transaction takes place on my account for two reasons:

- To have peace of mind in terms of security, i.e. to know nobody uses my bank account without my knowledge

- Know when my salary or any other incomes/expenses are happening, without having to open my app

4. ✅ Identity verification via online identification when opening the account

Although it didn’t bother me too much, I think it’s cool that Zak decided to go “all digital” for the account opening verification.

No more need to make a call with an advisor to check which face you have (especially when you’re doing it from the warmth of your bed), everything is automatic now and only takes 7 minutes.

So much for the positive “highlights”. I don’t mention the other basic features like payment, transaction view, or view of my balance. These are basic points; it’s normal that they work.

Let’s now move on to the points that Zak needs to improve.

The 4 negative points about Zak

1. 🔴 Still no eBill!

When I switched from BCV to Zak at the end of 2019, this latter announced eBill support for the end of the year (2019, that is). Then it was postponed to spring 2020. Then, due to technical problems, they decided not to announce any more date on their public roadmap.

Frankly, I hesitated to go to Neon at the beginning because I was so used to the practicality of eBill.

After a few months without it, I got used to scanning my invoices in batch once a month, and it’s fine. There are worse things in life.

But still, I think it’s (really) a shame that Zak put other features (like digital identity verification instead of videoconf) before eBill. So I asked my contacts in the Zak marketing team about it. Here is their answer:

“Unfortunately, I can’t answer this question in detail. We were hoping to have eBill much sooner. We get a lot of questions about it, and it’s not easy to explain why eBill is still not available. The fact is that the functionality seems more complex than expected, which is why its release has been postponed several times. We are still working on it. Hoping to release in early 2021.”

At least we can see that this is an internal concern and not a marketing strategy… For my part, I am still wondering whether I should switch to Neon as my primary bank, but for the moment I am (still) waiting a few more months.

2. 🔴 Can’t save beneficiary when scanning ISR

60% of the time, the beneficiary information is not contained in the ISR when you scan it. This means that you have to fill in the beneficiary manually. This is for example the case with our childcare solution. Every month, I have to type in the recipient information manually. So, yes, we’re talking about luxury problems, but still, it’s a pain.

What would I like? That the app would record the recipient’s information. And at worst, if it has changed in the meantime, I’d adapt it. But very often, companies don’t change their address like that.

I hope that with time it will get better.

Afterwards, I know that Zak has implemented the scan function for new QR-invoices. Since I never received any, I don’t know if autocompletion is better through this way (if you know, tell me about it in comments)?

Maybe that’s why Zak doesn’t develop more ISR functionality in the end.

3. 🔴 Auto-complete mTAN SMS

I’m a big fan of double-authentication security, especially when it comes to my CHF ;)

It’s now a habit for me that, when I log in, I have to enter an SMS code to confirm my identity.

Except that in 90% of my apps, I log in, the SMS is received in the background, and I see it displayed just above my keyboard (I’m on iOS), and I just have to type it to fill the field and log in (or do any other secured action).

Except that on Zak, it hasn’t been coded “correctly”, so it doesn’t take advantage of the ease of use offered by my operating system… So I have to open my SMS app, open the “conversation” with Zak’s robot, remember the code (because no copy-paste is possible on Zak app side…!), and go back to the Zak app to enter the code (with letters moreover, which I find harder to remember than numbers).

So yes, again, there are worse things in life. But hey, I’ve warned that I’m going to talk about the things that bother me in my everyday use. So there you go: “Dear Zak product team, please, can you adapt your code a little bit to make my life a little easier every day?”

4. 🔴 Issue with standing orders (reader’s feedback)

I was going to finish my list of things to improve with the previous point, but I received this comment from Lola recently on the blog. I thought it was good to take it into account because I myself have never had a problem with the standing order feature (I have 7 standing orders in total, which I haven’t touched after setting them up.)

Here is Lola’s feedback:

“I’ve been using Zak since the beginning of the year after reading your article. I’m having some problems with the use, especially with the standing orders. Impossible to delete from the app, you always have to call them. And modifying is often not allowed either [1]. I had another inconvenience with the standing order for my rent. Most of the time it works, but it happened twice that it doesn’t work (even though it’s a standing order, so it’s the same operation…). And the app doesn’t warn that the payment hasn’t been made! And since I usually connect just once a month, I don’t see that it doesn’t go through and that the payment amount has been reimbursed. So I get a reminder fee… I called them to report the bug, and I asked for compensation for the reminder fee. But they don’t enter into such discussions. According to them the problem comes from the fact that I don’t write “Suisse” at the end of the recipient’s address. And since my app is in Italian, it automatically writes “Svizzera”. But if you look at the other payments I’ve made, a lot of them have gone through like that… And this same standing order is one of them.”

Not a great experience… Dear Zak team, I hope you’ll fix this soon!

[1] I never faced this issue, and the rare times I tried, I could edit my standing orders without issue.

Conclusion

Compared to very good apps like Revolut, Zak (and Neon too I think) have some progress to make. As much on the functionalities as on the fluidity of the app.

Nevertheless, for me who only uses the app a few times a month (except for the practical part of the pots), it does the job it should do without too much hassle. And in terms of choice, it’s in my opinion still the best free mobile banking alternative here in Switzerland.

So I will continue with Zak as primary bank and Neon as secondary bank.

And you, are you happy with your Swiss bank? Which one did you choose?

PS1: the coupon code “Y06JPR” that entitles you to CHF 25 of welcome cash is still valid with Zak (to be entered in the app once your account is validated). The blog will also earn an affiliate commission, and I thank you for that — as usual, I’m careful to be objective and only recommend products I use myself every day.

PS2: I have recently been asked several times for my opinion on CSX, the new digital and mobile solution from Credit Suisse. My point of view is that the “big” banks are finally moving in the right direction, and that is positive for us as customers in the long term. But when you look at the details, you can see that they still take us for stupid people with their free solution that still charges you CHF 2/withdrawal at their own ATMs… So for the moment, I won’t check their solution in details because Zak and Neon are doing better for the frugalists that we are.

Lower your rent in Switzerland if you live in a …

Net worth and savings rate update October 2020 CHF...

Last updated: December 11, 2020