In Switzerland, as of today, there are 55 billion assets in vested benefits, of which the owners of 13 billion have not been found. This concerns something like 20% of the population. That’s when you think that this could be your case, and that you might be interested in knowing more.

Especially when you’ll know that you could also make babies with this money of yours :)

“MP, sorry to interrupt you, but could you please remind me quickly what a vested benefit is?”

What is a vested benefit?

Ah yes, good question! Because I myself didn’t know what it was when I received a letter after a job change some years ago.

Basically, when you are an employee, you contribute to the BVG (also known as the 2nd pillar) with your employer. The money you accumulate there is to pay your retirement when you get there (the “real” one, not our FIRE (Financial Independence, Retire Early) :D).

And when you change employer, or you become unemployed, or you take a sabbatical, or you leave Switzerland for a while, well, all the money from your BVG goes into a transitory account called a vested account. Other names you may have heard that refer to the same money are: exit benefits, or vested benefits.

And if you take up a new job as an employee, it is your responsibility to apply for the transfer of your vested benefits to the BVG pension fund of your new employer.

The first question you ask yourself is what the hell should you care about knowing whether you have so much money in vested benefits, because at the end of the day, it’s money locked up for your retirement, right?

I would answer that first of all, it’s still interesting to know whatever happens for the calculation of your net worth. Because as a FIRE wannabee, it is important to know the amount of all your assets so that your calculations are as accurate as possible.

Secondly, you might also be interested in knowing that you have money in vested benefits for the following four reasons:

- If you are looking for all your available equity for the purchase of your main residence in Switzerland

- If you want to become self-employed

- If you want to take an early retirement 5 years earlier than the legal age in Switzerland

- If you leave the EU/EFTA permanently

Because yes, these are four conditions where you can touch your cash which is in the BVG.

Put your vested benefit money to work too!

But the reason I’m talking to you about this today is mainly to explain that this vested benefit money is automatically put into a blocked account with the BVG’s Substitute Occupational Benefit Institution of the Swiss Confederation after two years without any news from you — it’s kind of the last Swiss safety net to prevent these assets from being lost/forgotten forever.

And I might as well tell you that, in general, BVG assets are invested conservatively (and that’s normal, it’s for your retirement after all), but then when they end up in the Substitute Occupational Benefit Institution, your returns are going to be really not great… (even negative if you look at some previous years). To give you a concrete example, the 2021 rate of this Institution’s fund was 0.01% of return…

The alternative to that is that as soon as you know you have vested money, well, you transfer it to VIAC or valuepension in order to invest it (there’s a future article coming up about which platform to choose based on your situation), and get it make babies while you go about your business.

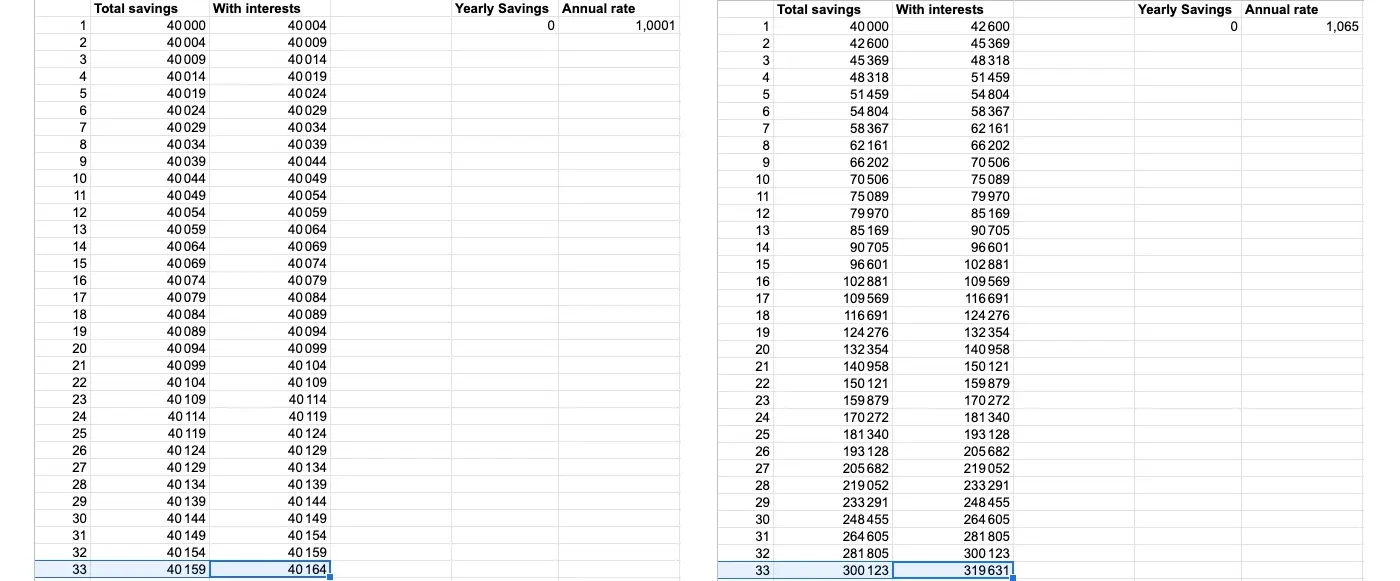

Because let’s imagine that you change job at 32 years old, with CHF 40'000 in vested benefits, and that the official retirement age in Switzerland is still 65 years old, then here is the difference of return if this capital is invested at 0.01% (Substitute Occupational Benefit Institution) or at 6.5% (via VIAC or valuepension):

- Value of BVG’s vested benefits not invested, at age 65: CHF 40'164

- Value of BVG’s vested benefits when invested, at age 65: CHF 319'631

So, the moral of this story is that yes, you are suddenly very interested in knowing if you have any vested assets lying around so you can start making them work for you as soon as possible!

Let me introduce you to Kala

After realizing how much cash you are losing by not investing your vested benefits, you naturally ask yourself:

But MP, how do I know if I have any vested assets that I forgot to collect?

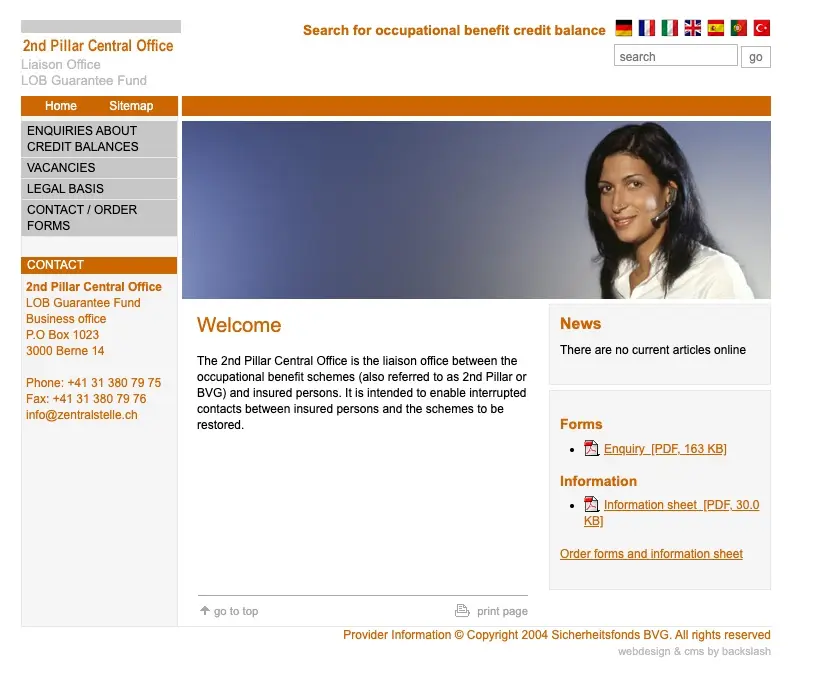

The answer until the end of 2020 was: “Go to the website of the 2nd Pillar Central Office (the institution that ensures the link between the BVG pension funds and the insured), which will do the research for you. It’s almost easy, just send a letter!”

“A letter? In 2020? Seriously?”

Except that, since 01.12.2020, there is a team of guys from the Jura (the founder is from the same network as Icanfly, it must have something to do with the clean air of the region ^^) who saw a business potential behind this nice old website from the 2000s and its processes via paper forms.

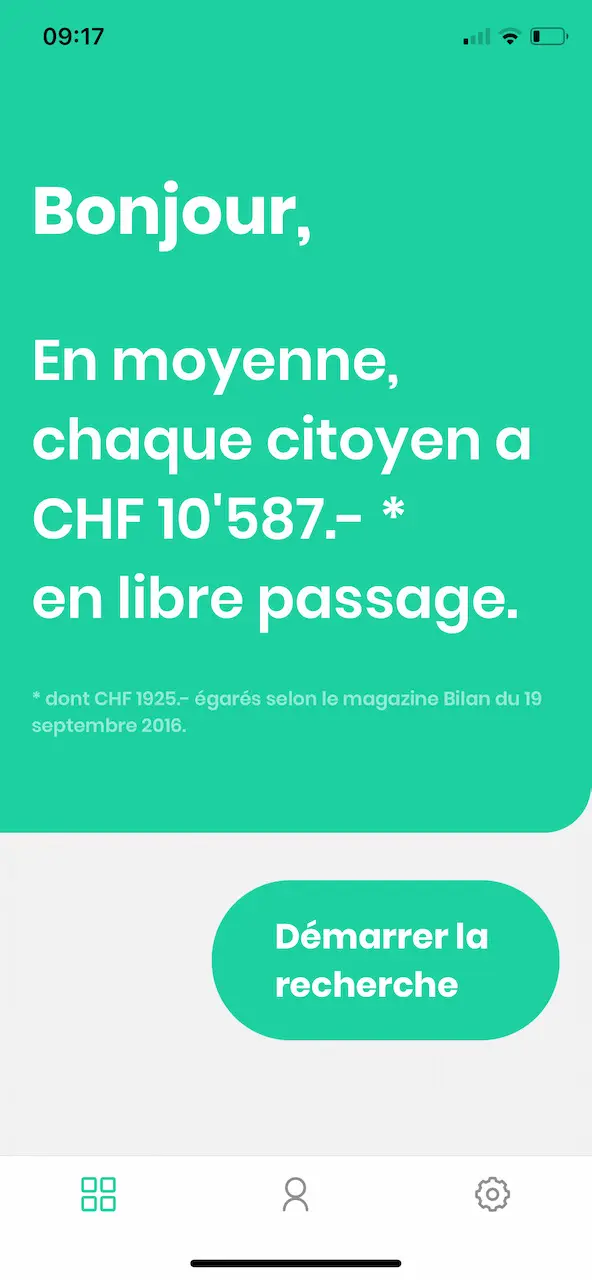

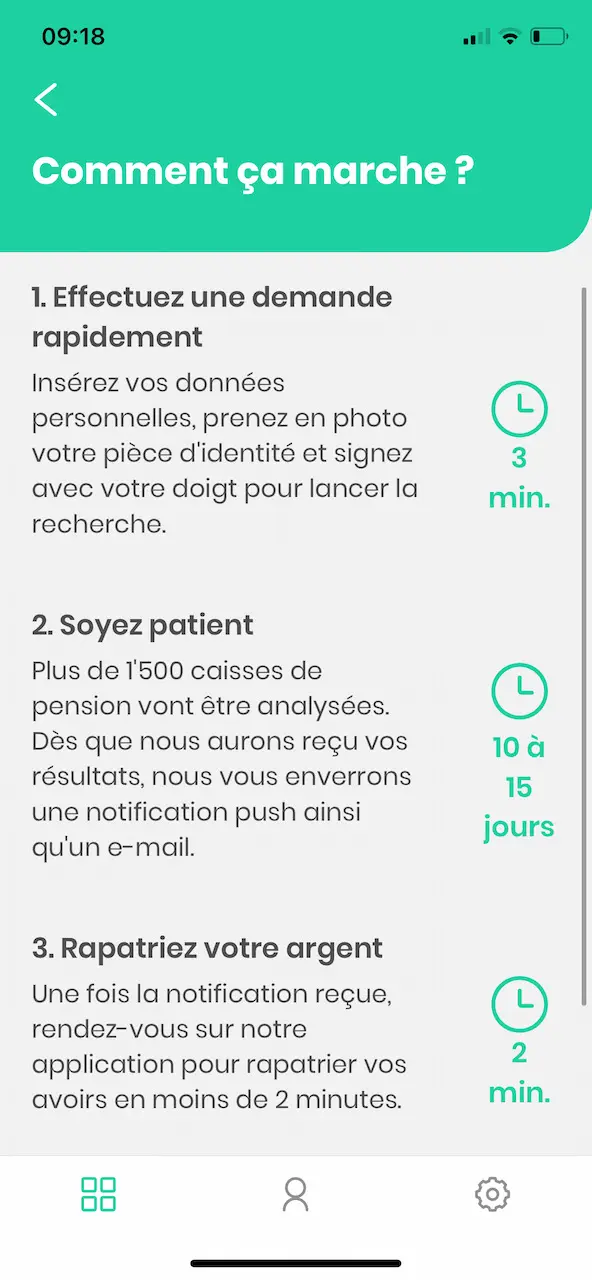

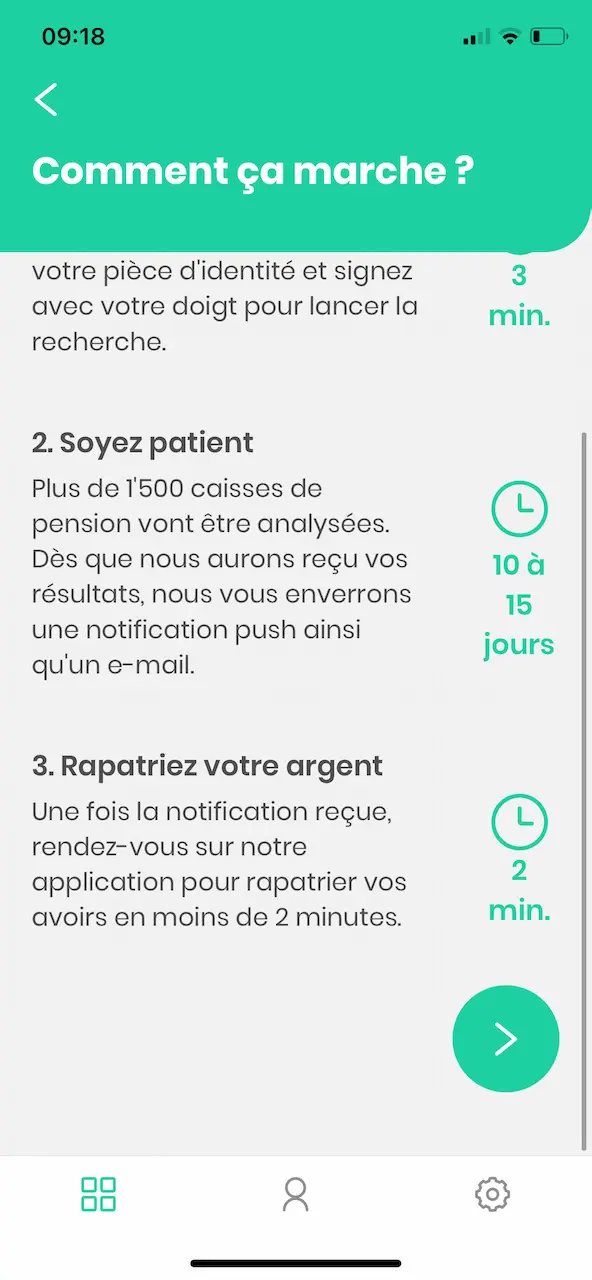

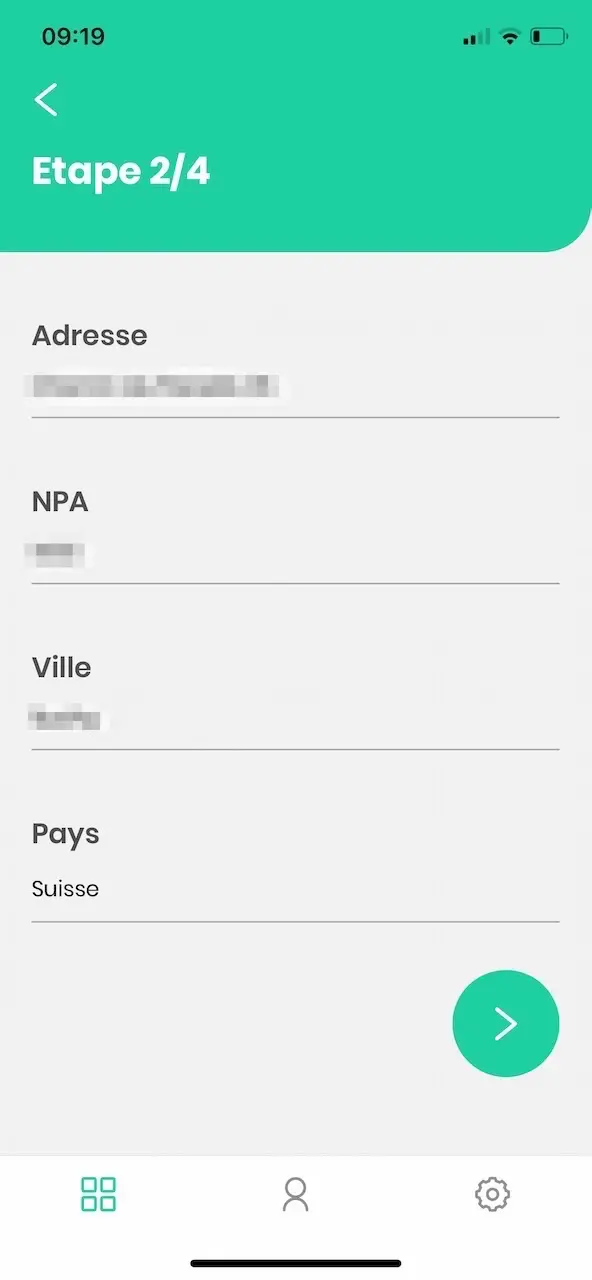

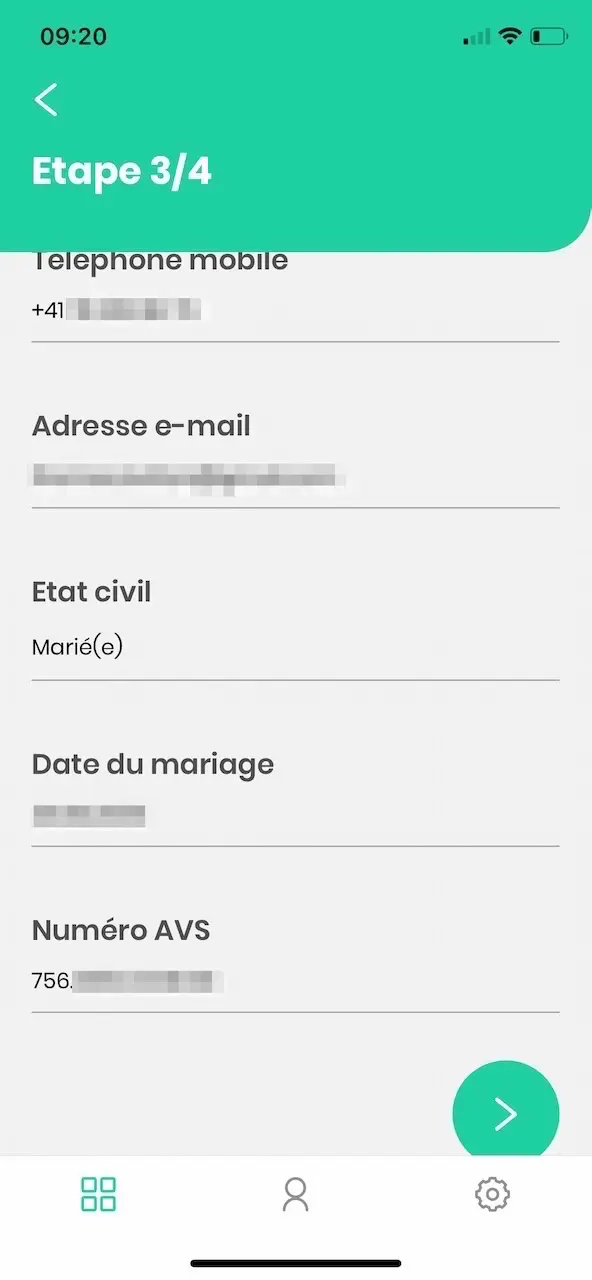

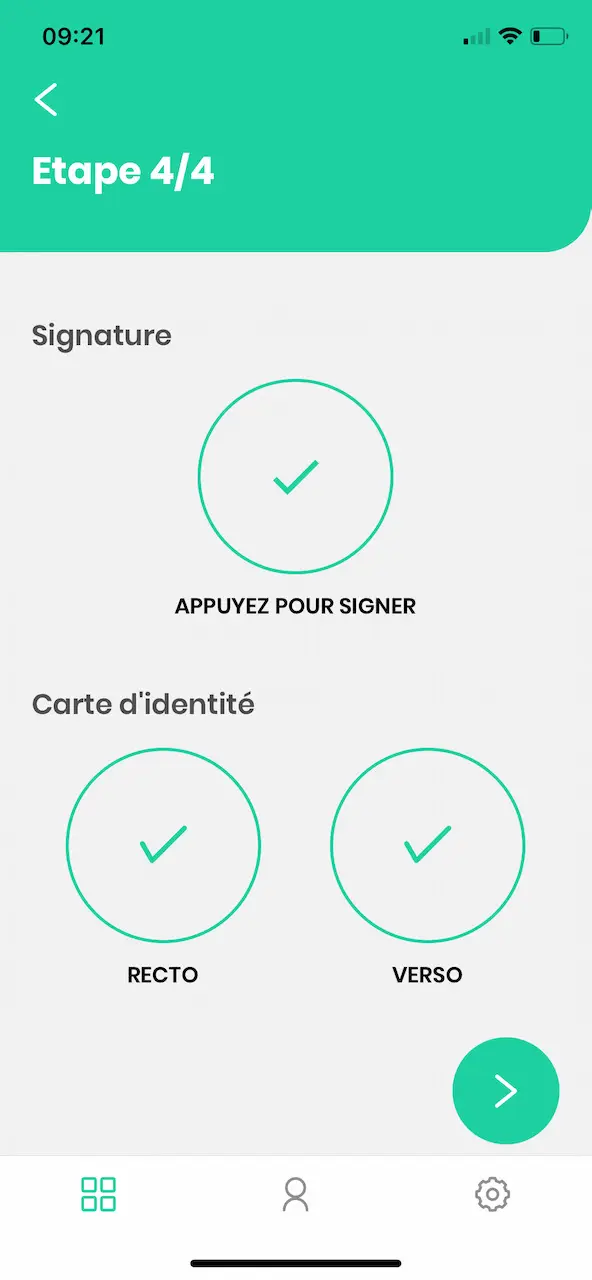

To make it short, the team of Kala has created a mobile application that allows you to search for your vested funds in the more than 1'500 pension institutions in Switzerland, and this, literally in 3 minutes (if you have your ID card and AHV number at hand). The screenshots (see below in the article) of my application are the proof.

And it’s free.

Too good to be true?

That’s what I wondered too, because I didn’t want to enter such confidential information in such a first app that came along.

Hence, the first thing I do: I check on LinkedIn who is in this company. And there, outch, the founder and director works at Swiss Life Select. Big warning in my brain like “Swiss Life Select = insurance = 3rd pillar that I don’t like at all” :)

And my brain goes on “Yeah, they’re going to sell the data to the insurance companies, so no thanks! Bye!

After some peregrinations on the kala.ch website (especially their FAQ), I see that no, they are not going to sell the data.

Also, digging deeper into Diego’s resume on LinkedIn, it turns out he’s not “just an insurance guy”, but rather a serial entrepreneur with a job on the side :)

Intrigued, my rational brain tells me that it would be interesting to dig even deeper, by asking my questions directly to the founder.

Interview with Diego Rohner, founder and director of Kala

I’ll put his LinkedIn profile here if you want to see his background in detail.

My preconceived ideas about Diego and Swiss Life Select immediately fell apart because he is such a cool guy from the Jura (I love this region :))

So, I didn’t beat around the bush, and I was quite frank with him. I’m putting the summarized transcript of our Zoom discussion below:

MP: What is your business model since it’s free for the end customer? How do you make money? Do you resell the data to insurance companies and stuff?

Diego: It’s funny because this is always the first question I get asked.

Basically, our business model is not based on B2C (i.e. for customers like you or your readers). We don’t make money with this version of Kala. It’s an investment actually, but I’ll explain that later.

First, let me answer your question. In fact, Kala’s business model is based on B2B, which is a pro version for brokers, bankers, insurers, fiduciaries, and other law firms. In Switzerland, our estimates show that there are 65'000 requests made to the 2nd Pillar Central Office every year, of which 50'000 are made by professionals. Their needs are for financial or retirement planning, or in the event of death with the management of inheritance, or even divorce.

And knowing that this kind of application work towards the Central Office takes between 6-8 weeks of file follow-up, well, there are quite a few advisors who don’t do it because it’s long and tedious.

It is by selling Kala to the pros that we will do business.

MP: OK cool, that makes me feel better. But then, why are you making this app available to the general public?

Diego: As I told you before, we actually see it as an investment.

We made this app available to the general public for two reasons:

- To start getting known

- To quickly test our solution in pilot mode, in order to make it bullet-proof and bug-free, so that we can ensure our credibility when we talk to professionals — because testing it with a big insurance company would take us ages, whereas now we’re already in production :)

MP: OK, but will it stay free for life or not?

Diego: So listen, for now, I can guarantee that until the end of July 2021, yes it will be free.

After that, depending on how things go with the professionals, we will potentially stop the general public app. Or we will ask for a small financial contribution from the user. We don’t know yet.

So, the only advice I can give you and your readers is to test it now ;)

Oh, and to be totally transparent, once you’ve received your answer from the Central Office (via a push notification in the Kala app, and also by mail directly from the Central Office), we have an employee who will call you to know if you’re happy with the service, and if so, if you can rate us on the application stores. In no way will he force your hand in terms of what rating you put, but it’s to help us with marketing.

MP: Interesting, and thanks for the honesty, we appreciate that at Team MP. Silly question maybe, but why not fund yourself by proposing cool vested benefits products (and receiving a business referral fee) if you ever see that the person actually has money?

Diego: Hey, we did think about it. And we even started to activate this feature recently. For the moment, once you know that you have vested funds, you will be offered to invest them via Mirabeau and Gonet investment funds, in 3 clicks. I know that you would prefer VIAC or something else, but for the moment, we are not yet partners with them. But Mirabeau and Gonet are private banks with hundreds of years of experience behind them, and they are the first ones who approached us and agreed to completely digitize the application process. And let’s face it, it’s still much better than the returns offered by the Substitute Occupational Benefit Institution :D — for example with the Gonet fund most used by our private clients, which is quite “safe” (30% equities, the rest in bonds and real estate) and costs “only” 0.73% TER, which is not so bad compared to the competition (and especially, again, compared to the fund proposed by the Substitute Occupational Benefit Institution! :D)

You think of everything :) You’re right, we prefer VIAC on my blog, but nothing prevents the readers who find funds to make the transfer request manually. Another question that remains in my mind: you guarantee me that you never sell the data to third parties?.

Diego: Yep, 100% guaranteed. If we do that, we’re shooting ourselves in the foot, because in 2021, people don’t get fooled anymore, especially with such data and a free product.

So no, we will NEVER resell the data we have.

I even add that everything is stored in Switzerland (Hostpoint), and that we are compliant with the GDPR.

And as for security, all communications between the app and the server are secured via SSL. And in terms of data, the photos of the ID card and the signature are encrypted.

MP: Oh good, you anticipated my questions related to security. If we continue with the technical side, how do you manage to ask 1'500+ pension institutes? Do you have a lot of interns? :D

Diego: Ahah, no you’re crazy. We don’t query all these institutions manually. In fact, what we do is to use the service offered to the citizen by the 2nd Pillar Central Office, and it is they who do all the scanning. We have “just” automated the visible part of the iceberg for the end user with the input and sending of the requests.

And to tell you how well it works; we launched the service on 01.12.2020, and by 26.02.2021, we had already processed 3'331 requests!

MP: Oh wow, not bad! It’s taking off well. And if I apply after we finish our call, how long does it take for me to receive the information from the 2nd Pillar Central Office?

Diego: So, normally we would say about 2 weeks. But since we launched Kala, the 2nd Pillar Central Office has been overwhelmed with new requests… ahah… so now we say 25 to 40 business days to get the answer in the app.

And how it happens, well, it’s simple:

- You receive a live notification in the Kala app that will tell you whether or not there are lost assets that have been found for you

- The 2nd Pillar Central Office will then send you a letter with the exact amount and the pension institutes where there is cash in your name

After this exchange with Diego, it reassured me and frankly, it’s a pretty cool idea and system.

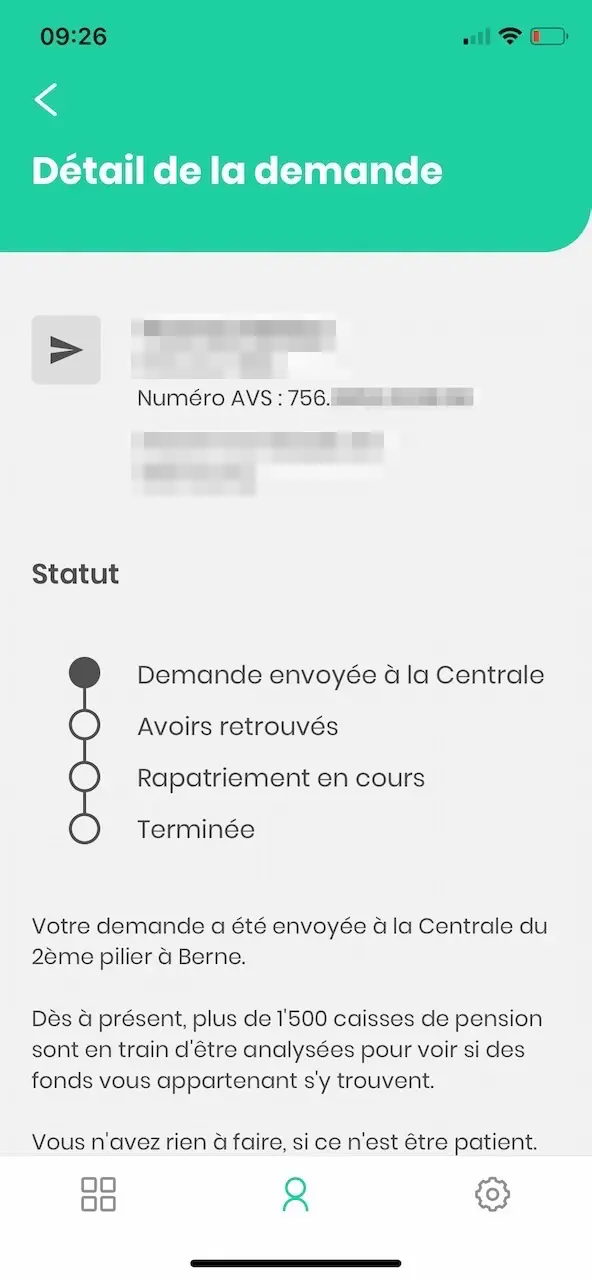

Kala mobile application test

Even if I know I have (normally :D) no vested benefits lost, I couldn’t resist to test the Kala app. And also like that, it allowed me to make you screenshots as you like so much :)

And indeed, I can confirm that if you have your ID card at hand, as well as your AHV number (available on your health insurance card), then it really only takes 3 minutes :)

The proof in pictures:

My opinion Kala

I was quite skeptical before talking with Diego, but now I am 100% reassured as I understand their business model.

I strongly recommend you to apply via their mobile app while it’s still free (until the end of July 2021).

And if you find lost BVG assets, well:

- Come and celebrate it on this article by leaving a comment to tell us how much you have recovered

- Don’t hesitate to rate Kala on the Apple or Google store to thank them for the service, it can’t hurt for their company

- Transfer all that cash (or only a part of it, depending on your legal situation) to an institution where you can make your hard earned CHF work for the next few decades until the legal Swiss retirement age

Consumers or investors, who has the (real) power …

From renter to frugal homeowner: Raphaël’s FIRE...

Last updated: April 14, 2021