If you’d ever told me I’d be talking to the godfather of FI (financial independence movement), I wouldn’t have believed you…

And yet… it did happen!

JL Collins has been the author of the blog jlcollinsnh.com since 2011. If you’ve been following the FIRE movement for a while, you’ll notice that he started his blog the same year as Mr. Money Mustache (MMM).

But unlike MMM, JL became financially independent before the name even existed!

His blog has given me a great deal of insight into the stock market, stocks, ETFs and bonds. By the way, I’ve got a surprise related to this in store for you at the end of this article ;)

So thank you, JL, for the inspiration of your blog and your books on personal finance; last but not least, thank you to your daughter Jessica, without whom none of this would exist!

MP video interview with JL Collins

Take a good coffee or tea with you because my discussion with JL went on for 1 hour :)

So here’s my interview with the Godfather of the financial independence movement:

Important note: You can activate German or French subtitles if they don’t appear automatically.

Video transcript

And if you’d rather read than watch the video, then here’s the transcript of my interview with JL.

1. What’s your real name behind JL?

Sure, it’s James Linton. Linton is a family name. So that’s where the JL comes from.

2. Why “nh” in jlcollinsnh.com?

Ah, so when I was first creating the blog… I wanted it to be my name because I was just going to share it with family and friends.

I never dreamed I’d have an audience, or I would have come up with a more creative name…

So I wanted them to know it was me. And all the versions of my name were already taken, but we were living in New Hampshire at the time, and so I found if I did J.L. Collins and put NH for New Hampshire at the end, I could get that URL.

So that’s where that comes from. We don’t no longer live in New Hampshire, so now it’s kind of nonsensical, but there it is ^^

3. Can you tell us how you grew up?

Sure, I grew up in the Chicago area in the United States, and I’m a baby boomer.

I was born in the 1950s, so that kind of places the time when I was coming of age, I suppose. The most striking thing about that, though, is that my dad was a manufacturer’s rep, and he was a pretty successful guy. So we had a pretty comfortable life but… he was also a cigarette smoker.

And as the cigarettes debilitated him because he was self-employed, his ability to earn money diminished.

So over time, our circumstances went from being very comfortable to being very uncomfortable as his earnings dropped along with his health. Cigarettes kill you slowly, and they debilitate you along the way.

I wanted to make sure that if the time ever came when I couldn’t work for money […], that I would have investments that would take up the slack.

So, I think that’s one of the things that informed the way I look at money. I watched his ability to earn, which was the only source of income that we had, go away, and I determined that as soon as possible, I wanted to make sure that if the time ever came when I couldn’t work for money, or I just preferred not to, that I would have investments that would take up the slack.

And my dad was not an investor. So that’s probably what set me on the early path to seeking my own financial independence.

4. What were your parents doing for a job?

In my early childhood, my mom was a stay-at home mom. But again, as my dad’s health failed, and his income dropped, she had been a school teacher before they were married, and so she went back to teaching school.

When I was a young child, growing up in grade school, for the most part, I grew up with my mother working. So I was what they used to call “Latchkey kid”, you know, you came home and neither of your parents were at the house.

You just let yourself in and began your after-school day on your own.

5. What did your parents teach you about money?

Money was not really a topic of conversation in our household. We were, or should I say, they were fairly thrifty people. They were fairly frugal people. But again, when the times were good, when my dad was healthy and his business was going well, we lived pretty well.

And the challenge is: his health failed was trying to maintain some of that lifestyle, which of course, became progressively more and more difficult.

By the time it was my turn [to go to college], there was just no money available to do that.

So, for instance, I have two older sisters. One is ten years older than I am, one is six years older. My parents paid for their college education. By the time it was my turn, there was just no money available to do that. I’m sure they would have done it had they been able to, but I had to put myself through college, which was something I take a lot of pride in, was a great experience, so I don’t feel bad about that.

That is sort of an illustration of how the family fortunes changed.

6. What career path did you follow?

I was an English major in college, which qualifies you to do virtually nothing…

But when I was in college, I really didn’t give any thought to what I was going to do for a career. I know that probably sounds pretty stunning in this day and age where parents and children are both obsessed about what career a degree will lead to, but that was not something that I was concerned about.

When I came out, and I started looking around, my older sister was in the advertising business. So, I started looking for jobs in that business, and I wound up getting my first job.

It took me two years out of college to get my first professional job. So, it was not easy back then… the seventies were a difficult time economically in the United States.

Hence, my first job was in the magazine publishing business, and that’s where I spent the bulk of my career. I fell into it almost by accident, and it turned out to be a happy accident because it was pretty good business to be in the day, and I enjoyed it and I was fairly good at it.

So, yeah, but it was not investing. Investing was an avocation rather than a vocation.

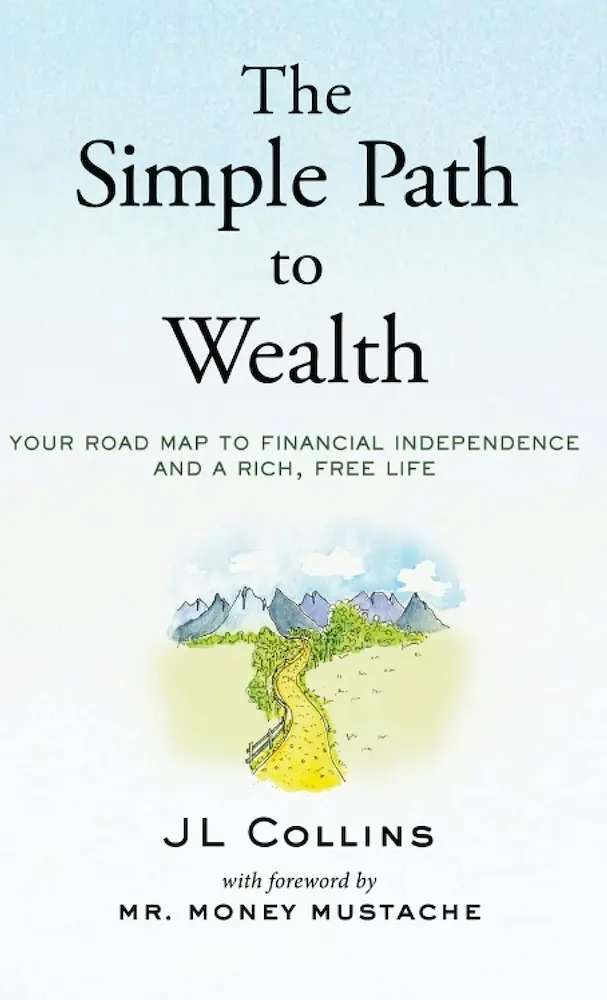

7. Can you introduce newcomers to the basic concepts of your book “The Simple Path to Wealth”?

Sure, so I have three books out.

The first I published in 2016, which is “The Simple Path to Wealth”, and it is far and away the book I am most well known for.

It’s sold worldwide over 700'000 copies at this point.

And I wrote “The Simple Path to Wealth” based on the material I put together in the blog, which I’d started in 2011. And all of this was written for my daughter because when she was young, I had tried very hard to tell her about this stuff, and I pushed it too hard and too early, and I managed to turn her off to all things financial, so I wanted to make sure the information was available if and when she was ready to hear it.

So that was the origin of the blog, and then at some point I realized there’s enough material in the blog for a book so that all of this info was more concise, and better organized and more polished.

And basically, “The Simple Path to Wealth” is what I told my daughter that she’d do financially. The three fundamentals are:

- Avoid debt

- Live on less than you earn

- Invest the difference (specifically, invest it in broad-based low-cost index funds)

Order “The Simple Path to Wealth” >

The second book was called “How I lost money in real estate before it was fashionable”. It’s a very short book. It’s very wonderfully illustrated. So it’s a cautionary tale if you will.

It’s the story of the very first thing I ever, real estate, ever bought which was a condo in Chicago, and it was a disaster from beginning to end until I finally got rid of it.

It took me a long time before I could laugh about this, but once I got to the point where I could laugh about it, I thought this will make an entertaining book and maybe help people who get seduced into real estate from making the same kind of mistakes that I made.

And so it’s very short, it’s kind of fun, it’s a humorous story, and as I say, it’s very cleverly illustrated. Not by me. I’m not an illustrator.

Order “How I Lost Money in Real Estate Before It Was Fashionable: A Cautionary Tale” >

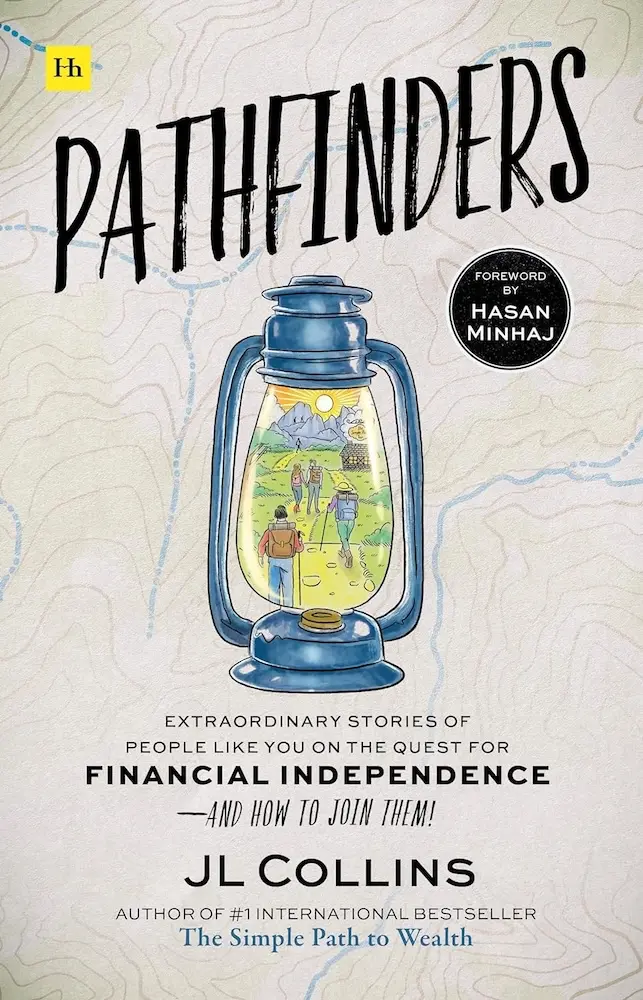

And the most recent book which came out last fall is this one [JL is showing the book to the camera]: “Pathfinders”. It’s a book that I’ve wanted to do for years, literally.

Shortly after “The Simple Path to Wealth” came out, probably six, eight months after it came out, I started to hear from people all over the world who would tell me about how they took the principles in “The Simple Path to Wealth”, and applied it to their unique situation.

And this was endlessly fascinating to me because I’d written this for one person at first.

I’d written it for my daughter.

And she was in college at the time, so at the beginning of her journey. She is an American, so it’s kind of a US-centric book.

And yet people at all different ages, at all different stages of their journey, people that have accumulated debt that they have to unwind from, or people that maybe have acquired some investments that they realize they’re not the best so they have to unwind. People from different countries who have different specifics to what’s available to them from an investment point of view.

All of them were finding great value in “The Simple Path to Wealth”.

And I’d heard these stories, where they said to me very clearly that this is a path that’s available to anyone.

And one of the things that I noticed writing the blog is in this financial independence community, a lot of the pushback would be, well, that’s great, you know, if you’re a college-educated engineer, and you’re making six figures, but it doesn’t apply to the rest of us.

Well, that’s simply not true.

And “Pathfinders” is a collection now of 100 stories from all over the world, people of all different stages in their life, all different walks of life, all different countries. There are stories from every continent except Antarctica. And then, I had somebody who was stationed in Antarctica reach out and say: “I wish I’d known your book before because it had a big influence.” But that story’s not in there.

But the striking thing is there are a couple of people who fit that profile of high income, Silicon Valley engineer. Like this particular story of a couple from Ohio who moved to Silicon Valley, lived as cheaply as they could, saved their money, made the big income, and then moved back to Ohio where the cost of living is a lot less.

But there are also stories from other people. For instance, this guy who is a migrant fruit picker with a humble beginning.

That’s why I love it because it illustrates that this is truly a path that’s accessible for anybody who chooses to walk it.

8. Can you explain the parable of the Monk and the Minister?

“The Simple Path to Wealth” opens with a parable.

It’s one of my favorites that I’d heard years ago.

The parable tells the story of two boys who grow up, and they go their separate ways. And years later, when they’re adults, they run into each other on the road.

And one of them has become a humble monk who has a begging bowl, and the other has become a very successful, wealthy minister to the king.

And, as they meet on the road, they’re happy to see each other and they’re catching up, and what have you.

I think they are setting themselves up to essentially be a slave to their jobs.

The minister is looking at his friend in his kind of tattered robes, and he wants to help. So he says to the monk: “You know, if you could learn to cater to the king, you wouldn’t have to live on rice and beans.”

To which the monk replies: “If you could learn to live on rice and beans, you wouldn’t have to cater to the king.”

And for me, that’s the spread of how we approach our life.

And I’ve always been closer to the monk.

I’ve always wanted to live on less, and invest the difference and secure my financial independence.

People live paycheck to paycheck and spend everything they make, and go into debt to buy more to maintain some lifestyle. I think they are setting themselves up to essentially be a slave to their jobs, always to have to cater to the king, so to speak.

9. Has your wife already been in debt? And your daughter?

Thankfully, neither my wife nor my daughter have carried debt.

You know, I tell a funny story that I used to say to people: that you should always talk to the person that you’re thinking about marrying about money before, because money is the biggest stressor in marriages, and the leading cost of divorce is when people have different attitudes towards it.

On our first date, you told me I needed to save 50% of my income!

But I used to say, you know, I just got lucky because Jane and I, when we were dating, we never talked about money. And I was telling that story one time in front of her, and she stopped me, and she said, “What are you talking about? We never talked about money? On our first date, you told me I needed to save 50% of my income!”

So I guess I talk about it without realizing that I’m talking about it.

She was very frugal, very responsible with money. Not like me. She never carried debt.

In fact, as you know, over the years, if you follow “The Simple Path to Wealth”, which we have, you ultimately wind up wealthy.

And so we have considerably more resources available to us now than when we were first married.

But you have the habit; at least we have the habit of being frugal, which served us well getting to where we are but isn’t necessarily what we need now that we’re here.

And so I’m constantly trying to encourage my wife to go out and spend money, which I know runs counter to most people’s experiences.

And I’m constantly failing in that because she just doesn’t care about the sort of things that money can buy, for the most part.

10. What has always been a struggle in your Collins family regarding expenses (that you wish were lower)?

So the truth is, there aren’t any.

You know, when I got my first professional job, it paid $10'000 a year.

Again, this was back in 1974, so that’s more money than it sounds like today, but it still was not a lot of money.

And I just arbitrarily decided that I was going to live on half of that.

And I knew people who were living on $5'000 a year, so I knew I could do that.

And I created a lifestyle in the city of Chicago in those days where I could afford to live on that 5'000. And that freed up the other 5'000 to begin buying my freedom, which, of course, I did with investments.

So we’ve never really had struggles, and as I mentioned earlier, my wife is also very frugal with money, very careful with it.

So we’ve never had an expense that we’ve looked at, and we’ve said, oh, we really need to rein that back.

As I say, the problem we have is very opposite at this point in our lives, where we could spend a lot more money than we do.

But we don’t deny ourselves anything that we really want. It’s just that, going back to the parable of the monk and the minister; our wants are pretty modest.

But, for instance, one of the indulgences that we have granted ourselves in recent years is when we fly. We fly first class. That’s expensive. But that makes something pleasant that I don’t like to do, which is flying.

It’s such an unpleasant process in this day and age, much more so than it was, you know, back when I was flying for business, that, you know, if I can spend a little bit of money and make it a little less painful, then I’m happy to do that.

So, we don’t hesitate to spend money if we think that it will improve our lives.

But Warren Buffett tells a great story.

He rarely buys cars.

And he says, “I only buy a new car when my daughter starts to tell me, dad, this is really getting disreputable, this car of yours.”

Warren Buffett, who’s worth something like $100 billion, can afford to buy any new car he wants. So he said pieces I just don’t want to spend half of my day, which is what it would take buying a car.

And I kind of agree with that.

You know, we don’t buy cars very often.

And, you know, if it was an easier, more seamless process, maybe we would. But the fact that I’m going to spend half a day or a day buying a car, that’s just not how I want to spend my time.

11. How do you deal with lifestyle inflation?

Yeah, so, lifestyle inflation.

Just to define it real quickly, it is when people come out of school, and they start working and their career starts advancing, and typically, they start making more money, then, well, they have a tendency to spend more money as they make more money. And sometimes it slips even beyond that, where they find themselves borrowing money to maintain some sort of lifestyle.

So that’s what lifestyle inflation is, when as your income rises, your lifestyle gets bigger and bigger and sometimes even faster than your income.

Lifestyle inflation is a very dangerous path to go down.

It’s a very dangerous path to go down.

Talking about it is a challenge for us because, as people can probably guess now, we never fell prey to that because I had this hard and fast rule that we lived on half of our income.

Now, to be sure, you know, that meant that our lifestyle did inflate, but at a very controlled pace.

So I mentioned that my first professional job out of college paid $10'000 a year, so I lived on $5'000.

Then, when I was making $20'000 a year, my lifestyle doubled.

It went from five to 10'000.

Of course, the amount I was investing also doubled.

So that was putting me in an ever stronger financial position when I was making $100'000. Well, now I’m living on $50'000.

So my lifestyle inflated, but at a very controlled pace because of that financial approach.

But my most important thing to me was that what also was inflating was the amount I was saving and investing. And that, of course, put me in a stronger and stronger financial position.

12. How do you recommend to compute one’s savings rate (pre- or post-tax income), and why?

You know, I don’t really give that a whole lot of thought.

That’s one of those questions I get on a pretty regular basis.

So it seems to be something that people obsess about.

I think if you’re going to save 50% of your income, obviously, if you save 50% of your income pre-tax, that is going to be a larger number.

If you save it after tax, then, you know, 50% of your after tax income is going to be a smaller number.

It kind of depends. Mine was pre-tax. Again, in the beginning, I was making $10'000 a year. That was my salary, and I just skimmed 5'000 right off the top.

You can compute your savings rate either way, whatever makes you more comfortable.

And of course, in those days, at that income level, I wasn’t paying a whole lot in taxes. But even as my income grew, and my tax brackets got bigger, and I was paying more in taxes, I personally still all thought of it as the salary, the total income I was making before taxes.

And that, of course, meant that it was a bigger dollar amount.

But really, you can do it either way. Whatever makes you more comfortable.

13. How did you concretely set up your financial system to make sure you saved 50% consistently?

Well, in the beginning it was manually, just because there was no way to set it up automatic, right.

I suppose it requires more discipline to do it manually, but it didn’t feel that way to me because I think it’s important to understand that this was not a sacrifice I was making, this was not deprivation to do this, that 50% that I put into saving and investing.

I was spending that money buying the most important thing that I thought my money could buy: my financial freedom.

I was spending that money buying the most important thing that I thought my money could buy, which was ultimately my financial freedom.

And you buy your financial freedom, your financial independence, by buying investments.

So I actively looked forward to getting my paycheck and to taking that portion of money and deploying it, just as somebody who maybe finds great value in a fancy car or fancy clothes would look forward to shopping for those things.

So it was not a hard thing for me to do because that was my priority.

I was buying the most important thing to me in the modern age.

And when it became available, I set it up and automated it. So the money just got invested without my having to think about it. And that’s what I would recommend because that’s available now, and I am old.

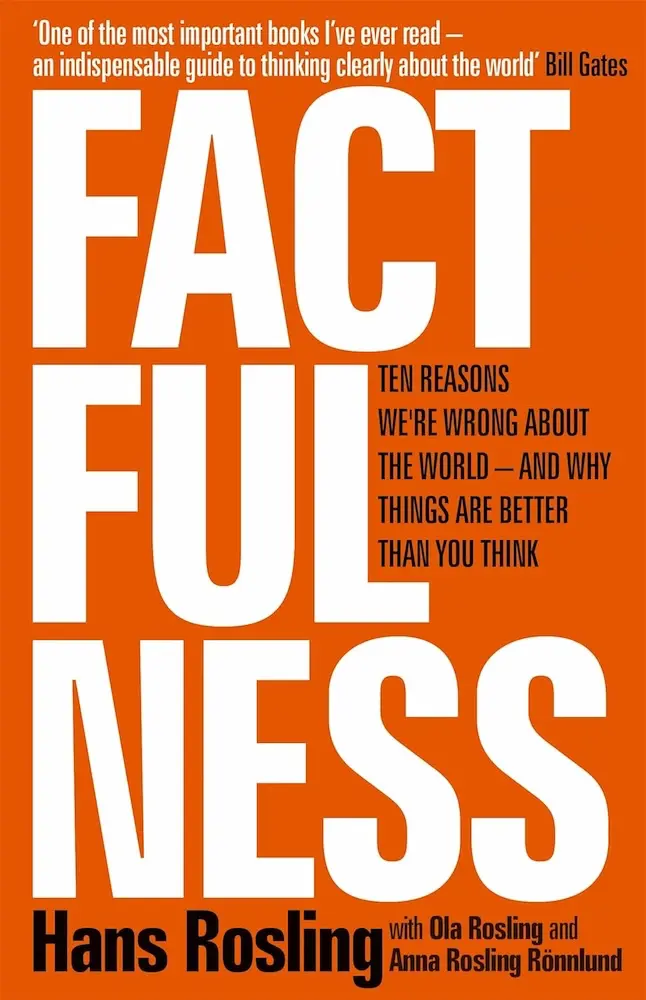

14. What’s the best book to understand capitalism, the good and bad parts of it, without politics entering into play?

So, first of all, I am a huge fan of capitalism.

You know, the world has become a vastly healthier, cleaner, wealthier place than at any other time in history.

And the root cause of that is capitalism.

It’s given more freedom, more liberty, better standard of life to more people than anything that has ever come before it.

So I’m a huge fan.

And if you’re following “The Simple Path to Wealth” in your investing in publicly traded companies, by definition, you are embracing capitalism. Probably.

I don’t know that this is a book about capitalism per se, but one of my favorite books to illustrate the point that I just made is called “Factfulness”, and it was written by a swedish guy, and he’s passed away since.

But what he did is he went back 200 years or something like along those lines and looked at the objective numbers, right?

Things like child deaths, deaths of children and the child death rate, you know, the longevity, income, and measured the improvements.

And without question, I mean even with war, violence, all these things, without question, every single metric has gotten significantly better.

So, if you were to do a thought experiment and say, you know, if you could choose to be born at any time in history, when would you choose?

And what I would say is, if anybody chose any other time in history other than right now, then you need to study a little more about history because things have never been better.

It doesn’t mean that we don’t have challenges and problems.

So there are certainly people in the world who are still living in abject poverty, but the percentage of people living in abject poverty has never been lower, and it’s dropping.

Certainly, we have challenges - environmental challenges - but air and water is just vastly cleaner than it was when I was a kid.

And I’m an old guy, but that only goes back to the fifties and sixties, right? I remember when polluted lakes were just accepted as that’s the way it was. Nobody in those days even thought about cleaning them up. Well, those same lakes from my childhood are now recreational facilities that people fish and boat and swim in.

So things have gotten measurably better.

And you wouldn’t know that listening to the day-to-day media.

Part of the thing is that, that because our world has become so interconnected that if any bad thing happens anywhere in the world, we can know about it instantaneously.

And I suppose that’s a good thing.

But the downside of that is it tends to make people think that there’s nothing but bad things happening, and things have never been worse than they are now.

I hear people saying this, and it’s just nonsense.

So “Factfulness” is a book that actually looks at data. These are things that we can measure, and the conclusion is pretty powerful.

So I highly recommend that book.

15. You said in your book: “Done well, [stock picking] can [work].” Yet you regret not choosing index investing before. Why is that?

Indexing is better, no question there.

You know, Jack Bogle created the first index fund in 1975, which, coincidentally, is the year that I first started investing.

I didn’t know about index funds at the time.

I didn’t know; had not heard of Jack Bogle.

I didn’t hear about index investing myself until 1985.

And then, it still took me a long time to fully appreciate how powerful it is.

And there was an enormous pushback against index investing because the investment community recognized that this was a threat to the very high fees and commissions they were charging their customers.

So they tried very hard to strangle this concept in its crib.

They mocked it.

They disparaged it.

They said it can’t possibly work.

But now, you know, decades and decades later, there’s been a lot of research done about it, and there’s no question it works and works better than just about anything else you can think of.

Now, I think where it gets confusing for some people, and this is what kept me from embracing it sooner, is it’s not like stock picking can’t work.

So you’re not choosing between a bad thing and a good thing. You’re choosing between a good thing and a better thing. And if you’re already involved in the good thing, which in this case is stock picking, and again, stock picking can be effective if you do it well, but most people don’t do it well, so most people lose money.

And those are the people you will hear saying: “Oh, the stock market, it’s like a casino, you’re just gambling.”

Well, that’s because you don’t really understand how it works and how to invest.

But if you do stock picking well, it can be effective, but it takes a lot of effort.

And the research is pretty convincing at this point. It’s a lot of effort for probably a result that will be good, but not as good as just investing in broad-based, low-cost index funds, which takes no effort at all.

And when that finally sunk in for me that I could get a better result for no effort, as opposed to the pretty good result I was getting with lots of effort, then making the switch to indexing was a no-brainer.

16. Why only US investors should choose home country stocks solely, without international stocks needed. Do you have economical proof that this couldn’t be the same for China or India?

So right now, and ever since World War II, the United States is far and away the most dominant country when it comes to the stock market stocks available.

I forget what the percentage is offhand, but I think the US accounts for over 50% of stocks around the world.

You’re right that China and India are rapidly growing economies, but their stock markets are not nearly as great a percentage of the world economy is represented in the United States.

There may well be a time in the future where people in those countries can also buy just their own market. But right now, I wouldn’t suggest that to anybody other than Americans.

And I think the time may come when it won’t apply for Americans either.

Because what’s happening is the rest of the world is growing and prospering, which it is, as that book “Factfulness” illustrates so wonderfully well, that the overall pie is getting bigger and bigger again, and you see that with China and India which are great examples.

And the US portion of that pie, from World War II to today, has gotten steadily smaller.

Now, that’s not been a bad thing for the US because the pie itself has gotten so much bigger that our smaller portion of that pie is significantly bigger overall for the economy.

So it’s still a good thing.

And of course, the vast majority of large us companies are international by nature. So by investing in the United States stock market, I am also benefiting from the growth of those worldwide markets.

But if I were in any other country, I would probably buy a world fund that would invest in the US, of course, and would invest proportionally so about 50% of it would be in the US and then proportionally in other countries.

And the time may come where that will be the advice I would give my daughter and other Americans. But right now, as an American, I think we can comfortably invest just in the United States and do well.

17. Should I invest solely into the S&P500 as a Swiss (or European) investor living in CHF, or stick to the Vanguard VT ETF?

You know, as I said a moment ago, I think if I were European, like yourself, a lot of your listeners, I would be in the world fund, which I think is VI [correction MP: it’s the VT ETF], you could certainly invest in the S&P 500, and you would mirror what I’m doing.

And that has pretty dramatically outperformed over the last couple of decades.

But those things are cyclical.

In fact, a lot of people are saying, maybe now is the time for us investors to embrace more international stocks because those stocks have more attractive valuation, and they could be right.

So I think if I were sitting in your chair, I’d keep investing the way you are [aka in the VT ETF].

18. Why markets are said to always recover?

Because human beings are industrious, and we are always working to make things better. This is one of the beauties of capitalism because capitalism encourages individuals to be industrious and to come up with new and creative ideas, and it rewards them for doing it.

You know, capitalism simply means that individuals are able to own things, and own the means of production.

Other economic systems basically say the politicians own everything and control everything. So therein lies the difference.

Well, when you empower people and reward them, allow them to reap the benefits of their work and their efforts, they accomplish amazing things.

And, for instance, if you look at global warming, one of the key issues of our time, well, my particular opinion is, if we are going to solve this problem, and I think we will, it will be because of capitalism.

It will be because innovative, creative people put their minds to it and come up with a solution. And in the process of doing it, they will probably make themselves and the people in their circle fabulously wealthy.

And I say that’s a wonderful, wonderful thing all the way around.

19. Why is it said that markets always go up?

So, first of all, you can’t be sure of that with individual companies because individual companies have, like human beings, they have a lifespan, right?

They grow, and they get stronger and stronger if they’re successful.

And then eventually they fade away as newer, younger, more aggressive, more creative places come and companies come up and take their place.

The beauty of being in something like VTSAX [MP note: or with the VT ETF for us in Switzerland] is that I don’t have to worry about that because whatever company is growing and prospering at the moment, I will own it, and I will own a greater and greater percentage of it. Because these funds are cap weighted, that simply means that the bigger the company, the more successful the company, the greater a percentage of the fund it represents.

Now, when companies begin to fade away, then that percentage that you own them begins to drop, and eventually, they’ll drift off the index altogether.

So that’s a process that I call self-cleansing.

So the index is always self cleansing.

I never have to worry about whether I’ve chosen the right company or not because I own them all.

So I never have to worry about whether I’ve chosen the right company or not because I own them all. And those that go to the top, I will own them when they do.

One of the criticisms of a fund like VTSAX, which is the total stock market index fund for the United States, which invests in every publicly traded company in the United States, is that when you look at the percentage of the fund, it is very heavily weighted into technology companies at the moment.

And so people will say, well, that’s a problem because you really own just a technology fund.

And what happens if technology doesn’t do well?

Well, in my world, that’s not a bug, that’s a feature, right?

Because right now, it’s technology.

But I’m an old guy.

I can remember when it used to be energy, when it used to be financial, and when it used to etc. you know, so I don’t know how long technology will be at the top, but I don’t have to worry about it, and I don’t have to worry about what will replace it when the time comes because whatever it is, I will own it.

That’s a feature.

And because human beings are creative, and we have had wonderful success in this technology arena that allows people to be even more productive and more creative. And whenever some new innovation comes to light at the moment, it instantly becomes available and benefits the entire planet.

If you think back to when we were hunter-gatherers, if somebody in your tribe came up with a better way to make a stone axe, well, nobody else is going to know about that new technology other than the people in your tribe. Maybe you could trade with the tribes that were closest to you.

But now, if you come up with a way to make a better whatever, you know that instantly, and then other people can build on it and contribute their ideas.

So we live in, really, a golden age, I think.

Now, could that be derailed?

Well, sure, it could be derailed.

I mean, if we get drawn into a nuclear war, well, all bets are off.

This is also dependent on capitalism being the economic system that you’re using because that’s where these things prosper.

If capitalism is replaced by something else that doesn’t encourage people to be innovative and doesn’t reward them for it, well, then this can die.

So there’s no guarantee it will last forever.

But what I will say is that if those things happen, then where you’re invested won’t matter. So, you know, I don’t see those things happening in the immediate future.

I mean, for instance, one of the big concerns of the moment is artificial intelligence, you know, taking over and destroying humanity. Some people think that’s not a risk at all. Some people think that we’ve got maybe five years left before we’re exterminated.

I don’t really know.

But I know that if we’re not exterminated, AI is going to be tremendously beneficial.

And if we’re exterminated, it won’t matter ^^.

20. Why do you NOT recommend the “Your age in bonds, the rest in stocks” portfolio strategy?

The traditional way of thinking about what percentage of bonds you ought to have in a portfolio is very much driven by your age.

And the thought process behind it is that as you get older, you want to become more conservative in your investments. You want to have less volatility in it. So stocks give you the highest possible return, but they’re very volatile, so they go up and down a lot, and that can be scary.

Bonds tend to give you a much smoother ride, but you don’t have the growth.

And so that’s the balance that you try to strike.

And the traditional way of thinking of things is you come out of college, you work for 40 plus years, and then you retire.

And so that’s where that formula you described comes from.

But what I notice in the financial independence community is that’s not true anymore.

There are people who are saving and investing aggressively, and they might retire in their thirties and then their earned income goes away. Well, they might want to add bonds at that young age to smooth the ride.

And then maybe, let’s say, they turn 40 and they’ve started a business that begins to prosper, or they just decide they want to go back to work.

Well, now maybe you want to go back to being invested fully in stocks because you have that earned income that smooths the ride for you.

So I think we live in a different world.

And the other thing that bothers me about that more traditional formula is it assumes that you are investing only for your lifetime.

And the statistics show that that’s not true.

Even if people are intending it to be true.

Most people who save and invest wind up passing on money when they die. And so when I look at my portfolio, I’m not investing just for my lifetime. I’m investing for well beyond my own lifetime, for my heirs and the charities that I support.

And so I’m going to be more aggressive because you want growth for those things.

So I have a longer time horizon than my own life.

21. Switzerland has no capital gains tax. What does that inspire you?

Yeah, I remember seeing that when you sent me the email, and I didn’t know that, and I envy you.

I mean, the idea of having no capital gain on your investment returns is obviously very appealing. And I think it’s a good thing.

I can’t speak for Europe, although I think you have similar plans to what we call IRAs [equivalent to our pillar 3a] and 401(k) [equivalent to a mix of 2nd and 3rd pillars].

And it’s always seemed to me that the government is a little schizophrenic in how they think about letting their citizens build wealth.

So, in the United States, they want you to be wealthy enough that you’re not dependent on the government in your old age. So, they created things called IRAs and 401(k) that provide tax advantages if you invest, but they put severe limits on them because for whatever reason, they don’t want you to become too wealthy, right.

And I think that’s a political thing because, the wealthier and freer people are, well, the less dependent on politicians they are.

So I’m all for freedom and being less dependent on politicians. That’s my personal preference.

So, if it were up to me, I wouldn’t have all these complex tax-related investment vehicles that they’ve conjured up and are continually changing and tinkering with.

I would simply say: “You know what, investment income is not going to be taxed. We want you to save and invest and become wealthy, because that makes the country stronger, that makes you stronger, that makes your family stronger, that makes the people around you stronger, and that is a good thing overall.”

But that goes against some of the political preferences in our country. And I imagine in Europe, too.

22. How does the global warming issue (to be taken care of nowadays) affect the “always recover and always go up” market’s truth?

When it comes to global warming, it’s my opinion that if we can solve this problem — and, of course, there’s a chance that we can’t solve it, but if we can solve this problem, it’s not going to be solved by politicians berating people for not being more responsible in the way they live their life.

And you are certainly not going to get people in less developed countries to go along with saying you can’t develop the way Europe and the United States has because that would be environmentally bad because people want to enjoy the same kind of living standards that we have.

So if global warming is going to be solved, is going to be solved by creative, dynamic people coming up with technical solutions to that problem.

And again, this is the kind of thing that a capitalist system fosters.

Now, hopefully, that will happen quickly enough to resolve the problem soon enough.

So a good example of that is Elon Musk and Tesla. Almost single-handedly, Elon Musk decided: “I’m gonna start making electric cars, which had been discarded basically”.

I mean, it’s an incredibly audacious thing to do, but it worked. And now he has a successful company.

But moreover, it’s encouraged other automobile companies to do this.

And you look at China, for instance. China has a huge push in electric cars. And they’ve obviously said: “We’ve got a huge population and these huge cities. If we have all of these gasoline burning cars, we’re going to have a pollution problem, no matter how clean we make them because there’s always some pollution.”

So they’ve embraced this technology that’s an example of capitalism, technology companies solving these kinds of problems.

Plastic waste is a huge problem, and it’s one that particularly bothers me. Well, the issue is that plastics are incredibly useful materials, and they are used in applications for which there are no other materials that are nearly as good.

So you’re not going to solve plastic waste by getting people not to use plastic. You’re going to solve it when somebody comes up with a better material that has the same performance characteristics of plastics, but without the downside of them lasting forever, decomposing into microplastics.

So this is how both the economy will continue to grow, stocks will continue to grow, and human problems will continue to be solved.

23. What about ecology and financial independence — as on one hand, FI is about less consumption, while, on the other hand, it relies on stock market capitalism?

I think we touched on this with the last question because I think capitalism and growing companies are the engines that solve these problems.

So Tesla is a great example. And all of the electric car companies in China that it’s inspired are great examples of capitalist approaches.

Solving an environmental problem while still providing people the kinds of transportation that they want.

Now, when I set aside 50% of my income to invest rather than to buy stuff with, I suppose that speaks to my nature of being closer to the monk than the minister.

If more people bought fewer junkie things, then that would be bad for some companies, but it would be better for other companies that made higher quality things that maybe last forever.

I believe very strongly that it is a mistake to assume that owning more things will make you happier because the research indicates that really doesn’t work very effectively.

But I don’t choose to own less things for environmental reasons, and I don’t criticize people who choose to own more things for that reason.

I think it’s just a better, happier way to live.

But, yeah, if more people bought fewer junkie things, then that would be bad for some companies, but it would be better for other companies that made higher quality things that maybe last forever. So I think that’s a choice that individuals can make that will improve the economy and improve their own lives.

24. How did you handle the FI topic (including expenses) with Mrs. Collins over the decades?

So we didn’t do anything on a regular basis.

Again, my wife and I, in terms of our spending, we were completely aligned, so it didn’t really require any conversation.

Now, as time went on in our household, my wife basically is in charge of spending the money, and I’m in charge of the investments.

And we both worked, so we both earned the money.

But I think one of the mistakes that I’ve seen people make, including a very good friend of mine (who’s now passed away), like me, in his home, he handled all the investments, but he never told his wife what he was doing or why.

And so, when he passed away - and he died very suddenly - I was talking to her, and she had no idea what they had. She had no idea if she could keep the house. She had no idea if she was rich or poor.

Turns out she was fine.

Turns out he’d been a good steward of the money, but she didn’t know that, and she didn’t know where it was or how it was invested.

Huge mistake.

So one of the things that my wife and I do on a regular basis is we talk about what investments we have and why we have them and where they’re held.

Now, for us, it’s pretty easy because, again, I follow “The Simple Path to Wealth”. So I don’t have a lot of individual stocks that she’s going to have to worry about.

And one of the reasons for that is, when I pass, I want things to be as easy and as simple for her and, by extension, for my daughter as it can possibly be.

By the same token, every night again, we sit down, and she explains to me how she pays the bills, what the bills are and what the mechanism are for paying them and what she pays attention to.

And that were she to die first, which is unlikely, but not impossible, that I won’t have to suddenly wonder, how do we pay the credit card bill? How do we pay the real estate tax bill?

So it’s important we communicate on those things.

So communication is certainly important :)

25. In your FI journey, how long did it take you to start having philosophical questions about your own life?

So when I first started, and I made my first investment in 1975, I had no concept of being financially independent.

That was not something I’d ever heard before.

In fact, I didn’t hear that until many, many decades later.

What I did know is I didn’t want to be completely dependent on my ability to earn money like my dad was because I didn’t want to take that risk.

So I knew that if I saved and invested money, I would slowly build up more and more resources there. But I didn’t know, because the concept had never been put in front of me, that there would come a time where there was enough money invested that I didn’t have to work at all.

And partially, I enjoyed my career. So I had no particular burning desire to retire early.

And I didn’t retire early.

I enjoyed my career, but I also stepped away from it multiple times. I took sabbaticals, and I liked having the money available to allow me to do that, that I could go without income for an extended period of time.

But I thought of it as having F-U money, which was a term I got from the novel “Noble House” by James Clavell that I read in the seventies.

He had a character who has that as her goal is to accumulate what she calls F-U money.

So I had that concept in my head.

I wanted to have that.

But it wasn’t until much later, when I was taking one of those sabbaticals, and I suddenly realized, as I was doing the year-end financials, that we’d paid all our bills. And we didn’t have any income. My wife had also quit her job at that point because she wanted to go back to school.

We didn’t have any income.

We had a new baby.

We were living basically the same lifestyle that we’d lived before.

And at the end of the year, we had more money than we started with!

And I knew that something remarkable had happened.

And I went back, and I looked at the year before, and that was the same thing, which I hadn’t noticed that year, but I didn’t have a name for it.

I didn’t realize that, oh, this is financial independence. And it also didn’t occur to me that this means you never have to work again.

And then, in terms of overall life philosophy, I guess I don’t really think of it that way. I’ve always just gone through life, putting 1 foot in front of the other.

And as I’ve done and accomplished things that, new opportunities seem to present themselves and, some I pursue and some I don’t, and it’s just a matter of staying the course and putting one foot in front of the other.

And here we are :)

26. Do you think all FI seekers are actually refrained and fearful entrepreneurs?

My friends Christy and Bryce write the blog Millennial Revolution, and they wrote the book “Quit like a millionaire”. And they’re a couple who quit in their early thirties.

They were engineers, and they saved an invested. And when they got to their FI number, they quit, and they’ve been world travelers ever since. They just had a baby last year.

So while they quit their engineering jobs, which they really didn’t enjoy all that much, they always wanted to be writers, and that’s what they’ve done since.

And they’ve written this very successful, and I highly recommend their book “Quit like a millionaire”. They’re at work on their second book. Their publishers asked them to write another book.

So I have gotten to know, especially younger people in this financial independence community, I’ve met a lot of them, like Christian Bryce, who have quit their corporate jobs, so to speak.

But I’ve yet to meet anybody [who reached FI] who just sits on a beach for the rest of their life.

But I’ve yet to meet anybody who just sits on a beach for the rest of their life, especially if they quit at such a young age.

They all go on to doing other kinds of things. And you mentioned Mr. Money Mustache, who he hasn’t had a corporate job in probably a couple of decades now, but he still does a lot of active things, and he likes physical construction and some of these things. When you do it, you wind up making money again, which is a good thing.

And Mr. Money Mustache coined the term of the “Internet Retirement Police” because people would yell at him and say: “You’re not retired because you’re doing things that earn you money!”

And so that’s the reason, by the way, I don’t use the FIRE acronym, which means “Financial Independence, Retire Early”.

Because, number one, I never retired early, never wanted to. And number two is that this word “retirement” seems to be so triggering for so many people.

So, is Mr. Money Mustache retired?

Well, he thinks he is.

And, I don’t care ^^ he’s financially independent, which simply means he doesn’t have to work for money. He can do whatever he wants. He chooses to do some things that make him money.

Are Christy and Bryce retired? Well, they are from their corporate career, but they’re still doing things that are creative, and those things are earning them money.

And so I suppose if that’s your definition, they’re not retired, but who cares?

They’re financially independent, and that’s the important thing, which means they can do whatever they want, and they can also choose to do nothing at all.

Human beings tend to get a lot of satisfaction out of work and productivity and accomplishing things, and that’s why the world has gotten better and better because humans have done that all along.

And now we have an economic system that better than any other before. It encourages that, rewards that, and then plays to that wonderful characteristic of human nature.

27. Can you tell the story of the day you realized your money was still growing, while you didn’t have any income anymore?

I loved working, but I didn’t want to have to do it all the time. And so in 1989, I quit my job and wound up taking the longest sabbatical that I had ever taken.

That was for five years.

So I didn’t go back to work until 1995.

And during that period of time, my wife also quit her job and went back to school.

Our daughter was born in 1992.

So a lot of things happened in that period of time, and we didn’t have any income, but we did have investments, and I knew we had enough investments to carry us forward, so we didn’t really change our lifestyle at all.

And, in fact, there were some elements like our baby, who probably added some extra expense to it.

And this was before the days of computers being in common use. And so I used to do everything out of the pencil and a piece of paper. And once a year, I’d always sit down, and I’d go through all the investments, and see where we stood, and what our net worth was, and I’d look at how much we spent. And one day, when I was doing this, probably about three years into this five-year period, I finished the numbers, and I noticed that, you know, we paid all our bills, we led the same lifestyle we’d always been leading, and at the end of the year, we had more money than we started with.

We led the same lifestyle we’d always been leading, and at the end of the year, we had more money than we started with.

Again, I didn’t have any concept of financial independence.

This was not a goal that I was looking for.

So I thought, well, that’s kind of interesting, but it wasn’t a big deal. But I said to myself: “Oh, that’s pretty interesting.”

And then I thought, well, I’m going to look at the year before. And the year before was the same thing.

I hadn’t even noticed it the year before when I was doing the numbers.

It gives you an idea of how little I was looking for this.

And I think, if I remember correctly, even the year before that, it was the same thing.

So I remember thinking, well, this is pretty remarkable. And then, I put my papers away, and I didn’t think about it anymore.

It just that the implication that I never had to actually work again just never crossed my mind.

That’s a little embarrassing to admit. But, well, that’s the story.

Sometimes I wonder, as people are today, if I’d been aware of the concept of financial independence, if I’d been aware of what the 4% rule formula suggests, would I have retired at that point?

Again, it was in 1989, and I would have been 39 years old. So I was in my early forties when I was noticing this.

Would I have retired then? I don’t know.

Maybe I would have, but it just never crossed my mind.

28. When you reached FI, were you restricted in traveling abroad or such due to Jessica still being around with school duties and all?

I left my last corporate job in 2011. So I guess you would call that retirement.

And I really didn’t have any particular plans on what I was going to do at that point. And I left the job because it was a pretty terrible company.

I had gone to work for a friend of mine who had actually worked for me back in the eighties, and he kept asking me to come to work for him, and I liked him a lot. We were good friends, he was great.

Best boss I ever had.

I liked the customers.

I liked the team that he put together, but the company itself had just become a terrible place, and they had all kinds of policies that just got in the way of doing good, productive things.

And I finally got to the point where I just didn’t want to deal with it anymore.

And I remember telling Joe that I just can’t deal with this anymore. I just don’t want to.

And it was hard because, again, I liked him.

And there were a lot of things I liked.

So I didn’t retire because of my age, when I would have been 61 at the time.

Because I was anxious to be retired.

But I just didn’t want to have this job anymore, and I didn’t want to bother looking for another one. And then, coincidentally, that was the same timeframe where I had begun writing these letters to my daughter, which then became the blog.

And I never dreamed that the blog would become a big thing. When I started, it was just a way to archive this information for her and maybe just share it with family and friends. And of course, family and friends didn’t care about it at all.

But once the blog was out there, it started to develop a readership from other people, people I didn’t know.

And then Mr. Money Mustache discovered it, and I started making comments on his blog, and he asked me to do a guest post.

And so, suddenly, I had this audience that started to grow, and they started asking questions that gave me other ideas: “Oh, yeah, I should write about that.” I was telling myself.

And that ultimately became the “Stock series”.

When I started it, the first five posts were the only ones that I had planned.

There’s now, I think, 35 posts in it.

Those all came from people saying: “What about this?” And so, yeah, my audience kind of guided me and what they wanted to know.

And then, as we talked about earlier, that that’s where the books came out of and what have you.

In fact, my daughter likes to tease me about that.

She says: “Dad, if I’d listened to you when I was young, there’d be no blog, there’d be no books, there’d be no Chautauqua and Mark wouldn’t want to interview you.”

So, yeah, that’s sort of where it came from.

So I guess I’m still not retired, hehe.

29. What activity still releases dopamine in your brain nowadays?

Well, I am getting older, and I am slowing down.

So, I suppose it takes fewer activities to keep me occupied during the day than it might have at one point because my energy isn’t what it used to be.

But, yeah, the blog and the book; I have just had Pathfinders, my last book published last fall. I’ve been doing a lot of interviews like this one, so that’s got me kind of busy.

I’m actually at a stage now where I don’t have any projects planned in the future. There are a couple things I’m thinking about maybe doing, but I’m kind of a little burned out after writing the last book, and then going through the process of the book tour and promoting it.

So I think for the next few months, anyway, I’m going to just be kicking back and relaxing, and then I’ll get bored, and I’ll figure out something to do again. As we said, one foot after the other :)

30. Do you plan to visit Switzerland anytime soon? (I’d love to invite you for a fondue or raclette then :))

No, I’m afraid I don’t.

I have been to Switzerland, but it was back in the eighties, so it has been a long time.

I think we were in Geneva. It was sort of a stopover. We had been in India and Nepal with some friends of ours who at the time were living in Geneva if I’m not mistaken.

This friend of mine worked for Pan Am and in those days, Pan Am was still an airline and I think she headed up their airport activities. And so when we were flying back, we routed through Switzerland. They were living there at the time. We spent, I want to say, four or five days hanging out with them.

And I think it was Geneva, maybe Zurich. But, you know, my memory is getting older :) anyway, we had a good time and we liked it.

I would love to get back.

31. Where can we find and contact you?

The easiest thing is the blog, which is jlcollinsnh.com/, as we discussed, why it’s called that.

And then, from there you can find me on Twitter and Facebook and of course, you can also find my three books from the blog. They’re all available on Amazon. And Pathfinders is the only one that I’ve done through a traditional publisher, is available in bookstores, and so that should be even easier to find. But also on Amazon.

My reflections from my interview with JL Collins

Given the length of the transcript (and my notes ahah!), I put my notes in a dedicated article :)

Lastly, I’d especially like to thank Jessica Collins for not having listened to her father! Without her, this article and this interview would never have happened!

Last updated: June 14, 2024