UPDATE 06.12.2024: we adapted our investment strategy and choice of broker for our children. You’ll find all the details in this article.

I often get this question of how we invest money in our children’s names in the stock market:

- How should I be starting a stock portfolio for a child?

- How did you open a brokerage account in their name?

- Is it possible to open a brokerage account for each child? Or do you have only one?

- Which online broker did you choose for your children anyway?

- And do you have a special stock portfolio for kids?

Before I explain our method in detail (simple and efficient as possible), I have to tell you where we come from in terms of saving for our children.

Some background story

When our children were born, Mrs. MP and I wanted to do the right thing as responsible new parents. So we opened a special “kids” bank account in a local bank. When I say special “kids” one, it’s because this kind of account is usually opened from the birth of the child until he/she turns 18, so the bank generously offers you a huge 0.10% extra in interest… really, thanks for that!

And so, on each of these children’s bank accounts, Mrs. MP and I agreed to put CHF 50 per month 1. And we would also store any money they received from relatives for birthdays or Christmas or whatever.

And then I fell into the FIRE (Financial Independence, Retire Early) movement.

When I realized that we could grow our kids’ savings at 6-8% return instead of 0.25%, you can imagine what happened…

I called the bank and explained that I wanted to close our kids’ bank accounts :)

Except that, it wasn’t that easy. Because the banker answered me something like: “Ah, but Mr. MP, it’s not possible. The accounts are in the name of your children, and in order to protect them from some not-so-correct parents who use their money without their consent, well you can’t touch that money except under certain conditions!”

Me: “Excuse me!?! Is it April 1st or what?”

Me after ten seconds: “Uh, all right. And what are the special conditions to be able to withdraw this cash and close these accounts anyway? (thinking deep inside: do you really think I’m going to let a bank block my money, and believe that there is a law that really allows you to do that!)”

The banker explained to me: Then we need a valid written explanation that you are going to use your children’s money to buy something that is for them (with proof of purchase ideally)."

And I thought inwardly: “Yeah, sure! So I store cash in your bank, and then I have to explain to you why I want to withdraw it… “

If I’m constructive and less of a complainer, I can actually understand why the bank does this, because it’s true that some parents act anything but in the best interest of their children. But still, it’s too much interference for my taste.

Anyway, we had by chance a room rearrangement planned at IKEA, so we could take out the few hundred (a thousand at the most) francs. And we closed the accounts right away.

I’m telling you all this so that you can understand our choice of brokerage account system for our kids.

Our kids’ investment account configuration

Following this banking episode, we decided that whatever type of account and institution we chose to invest our kids’ money in, we would do so in the following manner:

- The account would be in one of our two names (Mrs. MP or me or both of us) — so as not to have the money blocked by any condition

- Their account would be separate from our own investment account so as not to mix our money with theirs (and also to use by myself in real conditions one of the other online brokers I recommend you :D)

- We would deposit all of our children’s money into it for simplicity of management (one account only)

- We’d track the entries in our favorite YNAB budgeting tool to see which child has which amount

- We’d share the stock market gains (dividends and capital increase) pro rata when we decide to transfer that money to them

The idea behind this system being simple: that we keep total control over our kids’ money until they reach the age of majority — vs. the banks or whatever financial law that may come down.

Our choice of broker and ETF for our kids

Then followed the famous questions that every Swiss investor asks himself (no matter how old he is ^^):

- Which online broker to choose as a Swiss?

- And which ETF(s) to buy?

My kids’ case corresponds to the same criteria of my own Swiss investor situation, namely: investing for at least 10-15 years, able to bear a risk of 7-10 (10 being the most risky), maximum 15-30 minutes of management per quarter, and no need for this money (aka it wouldn’t be cool if we lost it all, but it wouldn’t be a big deal either because we don’t depend on it).

As a result, I have not changed anything and apply the same investment strategy to them as to our own situation with Mrs. MP:

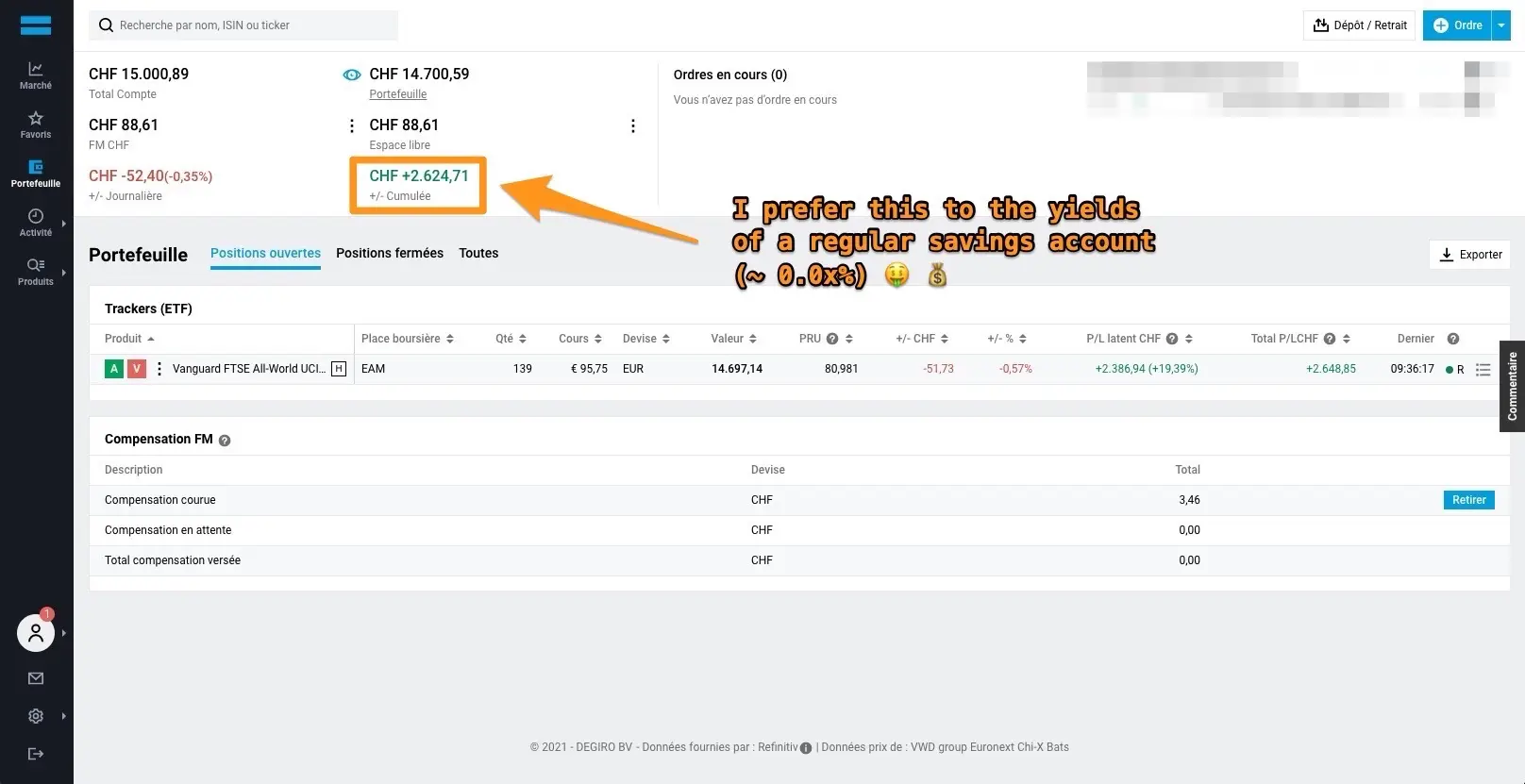

- Online broker for kids: we chose DEGIRO (you’ll find on this link my complete DEGIRO tutorial for opening an account) because we are not going to exceed CHF 100'000 invested over the next 15-20 years, and therefore DEGIRO allows us to limit brokerage fees to a minimum 2

- ETF for kids: knowing that the investment horizon is really long (minimum 18 years), I decided to put it all in my favorite global equity ETF: Vanguard’s VWRL ETF (which is exempt from transaction fees at DEGIRO if you buy it via the Amsterdam stock exchange with the shortened name of EAM for Euronext Amsterdam) to favor performance compared to “safety”

As I said in the introduction: simple, and efficient.

If you’re saving money for your kids, I’m interested to know:

- Do you invest it in the stock market or not?

- Which online broker did you choose?

- Which ETF portfolio did you choose?

We still need to clarify the strategy we’ll adopt to offer/give/transfer them this cash so that our kids make the best use of it. We agree that it won’t be to buy the latest smartphone or anything useless. But we still need to define precisely at what age they will be able to touch it, do we allow them to withdraw only the dividends to teach them what an investment is, or do we let them screw up by withdrawing everything, etc. We still have time to see what happens so it’s fine :) ↩︎

So that the full history is presented: I initially invested the money for our children in the stock market via my 3rd favorite broker Cornèrtrader (broker based in Switzerland). But after they introduced an inactivity fee, I decided to transfer the kids’ investments to DEGIRO (step that I described in detail in this article)

However, if today you ask me which Swiss broker to choose (because you are not ready to use one abroad for whatever reason), then I recommend Saxo Bank (<= CHF 200 brokerage fee refunded using this link, applied within 24 hours of the initial funding) ↩︎

Last updated: May 18, 2021