As a Swiss index investor, my ETF of choice for global exposure is the famous Vanguard VT ETF. The latter is registered in the US as a member of the Vanguard Group (source: ETF VT prospectus of Vanguard).

The question to which I still had no clear answer (until this article and the confirmation of an internationally renowned professional tax advisor) was: how does the US estate tax work in the event of death for a Swiss citizen?

Case study: MP family

Before exploring this topic, let’s lay the groundwork for our case study:

- I use a conversion rate of CHF 1 = 1 USD for simplicity reasons

- Mrs. MP and I (Mr. MP) are married

- Mrs. MP and I are both Swiss citizens

- Mrs. MP owns 1.2MCHF of assets in her name

- Mrs. MP has an Interactive Brokers account based in London

- Mrs. MP bought and owns 84kCHF of ETF VT (US based fund)

- That’s 7% of her total assets which are based in the U.S.

- Mrs. MP dies

- I am her sole and direct heir

Estate tax for US assets as non-US persons

By default, if you own US assets as a foreigner and then die, your heirs are charged 40% US estate tax on anything over USD 60'000.

By default, I would therefore inherit only CHF 74'400 of ETF VT. The reason for this is : CHF 60'000 tax-exempt by default + 60% of (84'000 - 60'000) = CHF 74'400.

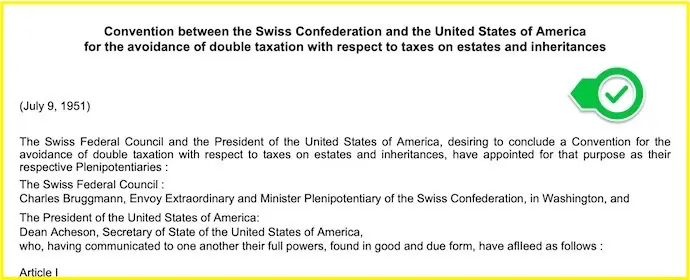

Estate tax treaty between the United States and Switzerland

Except that, the United States and Switzerland signed an estate tax treaty in 1951 to avoid double taxation. And that’s high-level legal talk :D

Following my analysis, my conclusion was that yes, our situation as presented above would allow me to not be taxed at 40% on anything over 60kUSD of US assets (but with another limit).

Instead, I would take advantage of the USA-CH estate tax treaty by being exempt from US estate tax up to 7% (i.e. my percentage of US assets out of my total assets) of USD 11.58 million (exemption allowed on estate tax for a US citizen in 2020).

Concretely, from my understanding, I will therefore be exempt from any inheritance tax on Mrs. MP’s US assets up to USD 810'600 (= 7% of USD 11.58 million).

I came to this conclusion by dissecting in detail each line of the Convention between the Swiss Confederation and the United States of America for the Avoidance of Double Taxation with Respect to Taxes on Estates and Inheritances:

“In imposing the tax in the case of a decedent who at the time of death was not a citizen of the United States and was not domiciled therein,”

That’s consistent with Mrs. MP, who is not a U.S. citizen, nor does she live there. We’re good.

“but who was at the time of his death a citizen of or domiciled in Switzerland,”

It’s okay, it still matches Mrs. MP.

“the United States shall”

First doubt: why “shall” allow? Why not “have to” or “must”, or simply “allow”?

“allow a specific exemption which would be allowable under its law if the decedent had been domiciled in the United States”

Reading this calmly on a Sunday afternoon, I understand that you get the same treatment as a US citizen with this sentence. That is, we’re taxed the same way he is when it comes to an estate.

in an amount not less than the proportion thereof which the value of the total property (both movable and immovable) subjected to its tax bears to the value of the total property (both movable and immovable) which would have been subjected to its tax if the decedent had been domiciled in the United States.

Seriously, would an example have been too much to ask?

So basically it says that you are exempt from inheritance tax just like a US citizen, but only up to the percentage of what you own in US property (the famous 7% calculation above).

Gosh, I would rather be at the Aubonne Arboretum walking around with the kids than having to read this legal jibber-jabber! ^^

Let’s continue the intellectual (not to be more vulgar) gymnastics:

“If a tax is imposed in Switzerland by reason of movable property being situated within the territorial jurisdiction of the tax authority (and not by reason of the decedent’s domicile therein or by reason of the decedent’s Swiss citizenship)”

Again, I had to take the time to read line by line.

I translate this sentence as “If you have some CH-based assets (we don’t care about your citizenship, we talk only about where are located your “movable assets”).”

“in the case of an estate of a decedent who at the time of his death was a citizen of or domiciled in the United States,”

It’s not our case. So we don’t care about that sentence, and the next one, for that matter.

“the tax authority in Switzerland shall allow a specific exemption which would be allowable under its law if the decedent had been domiciled within its territorial jurisdiction in an amount not less than the proportion thereof which the value of the total property (both movable and immovable) subjected to its tax bears to the value of the total property (both movable and immovable) which would have been subjected to its tax if the decedent had been domiciled within its territorial jurisdiction.”

So my conclusion as a non-specialist in international tax law is that I could let myself go by buying as many VT ETFs as I want. In any case much more than the default limit of 60'000 USD.

Except that until this article that you are reading, for fear of my incompetence in international taxation, I had always restricted myself to 60'000 USD of VT ETF maximum, and had fallen back on his European cousin VWRL for anything over that amount (see details here). Because a 40% tax rate, that hurts!

Marnin Michaels enters the stage!

While doing my Google searches on this subject of estate tax on US assets as a non-US person, I also came across this great article which summarizes the fact that the law should be revised because there are cases that are not covered because it’s no longer 1951…

We agree :) And if they could simplify the lawyer’s jargon by the way, that would be great!

The authors of this economic paper are Marnin Michaels and Jackie Hess. I contacted them to see if they would be willing to answer a few questions for an article and…they agreed! It’s with Marnin (cf. his LinkedIn profile) that the discussion continued.

First of all, I would like to thank him for his time that he made available to the Team MP for free, because it’s his job usually! So thank you Marnin.

MP: Marnin, do you confirm my case analysis above?

Marnin: Yes I confirm your analysis.

The US-Swiss Estate Tax Treaty is very old. It does not follow the new norm which is to exempt US shares from estate tax like the German and French treaty do. Rather, it’s the old formula system : US Assets/World Wide Assets * US exemption.

In the old days, the US was the only country to take this position. We now see more and more countries, like the UK trying to take similar positions.

MP: Thanks a lot Marnin for your confirmation. In the event Mrs. MP died, then I (aka Mr. MP) would need to claim this exemption by filling a 706NA US form. And that’s it. Is that correct?

Marnin: Yes, the US form 706-NA and a US form 8833 would be required to take the position.

MP: It seems very clear to me. One last question: many members of Team MP have the situation where they are not Swiss but expat. Does that change a lot?

Marin: The answers you gave concern Swiss residents, irrespective as to nationality.

MP: Perfect! I think we finally have our answer confirmed by a professional. Thank you again for your time Marnin.

Marnin: With pleasure.

VT ETF, I’m back!

Following this discussion with Marnin, I’ve decided to go all the way again with the VT ETF :)

I’m going to keep our VWRL positions to see how they evolve in comparison.

If you’re at DEGIRO (rather than Interactive Brokers aka IB), then you only have access to the VWRL ETF because of the latest regulations. On the other hand at IB you still have access to the ETF VT to this day.

What if you’re not a Swiss resident?

If you are not a Swiss resident, then you need to see if your country has a treaty with the United States.

While doing my tax peregrinations, I came across this fantastic table from bogleheads.org (one of my favorites websites) which lists its ETF domiciliation recommendations by country of residence. Just great!

Conclusion: thresholds to remember

To wrap up the key takeaways:

- Default rule for non-US persons: 40% US estate tax applies to anything over USD 60'000 of US assets.

- Thanks to the USA-Switzerland estate tax treaty (1951): Swiss residents (regardless of nationality) get a proportional exemption equal to (your US assets / your worldwide assets) × the US citizen exemption (USD 11.58 million in 2020, indexed yearly).

- Concrete example for the MP family: with 7% of total wealth in US ETFs, the exemption is USD 810'600 (= 7% × USD 11.58M). Well above the default 60k cap.

- Forms to file if needed: US form 706-NA + US form 8833 to claim the treaty position.

- For non-Swiss residents: check if your country has a similar treaty with the US (the bogleheads.org table linked above is a great starting point).

Bottom line: as a Swiss resident, the 60k default cap does not apply to you. You can hold VT ETF in proportion to your worldwide wealth — well beyond the default limit.

And you who read these lines, are you investing in US positions? Or only European positions? And why?

How to manage your budget: 4 simple and effective …

From poverty to a 50% savings rate: the FIRE story...

Last updated: May 17, 2020