At the start of my journey to financial independence, I didn’t have a credit card. My parents had always taught me that you don’t live on credit. So… no credit cards, period.

Then, as I sought to increase our income to accelerate our path to FIRE, I realized that a credit card could also be used intelligently.

Not to spend more, but to earn cashback on spending I was doing anyway, and thus increase my savings rate.

There is, however, one absolute rule: pay off your credit card in full every month.

If you’re able to stick to this discipline, this article is for you.

If not, close this page right now, because a credit card will only bring you unnecessary financial worries.

What’s the best credit card in Switzerland and abroad in 2026?

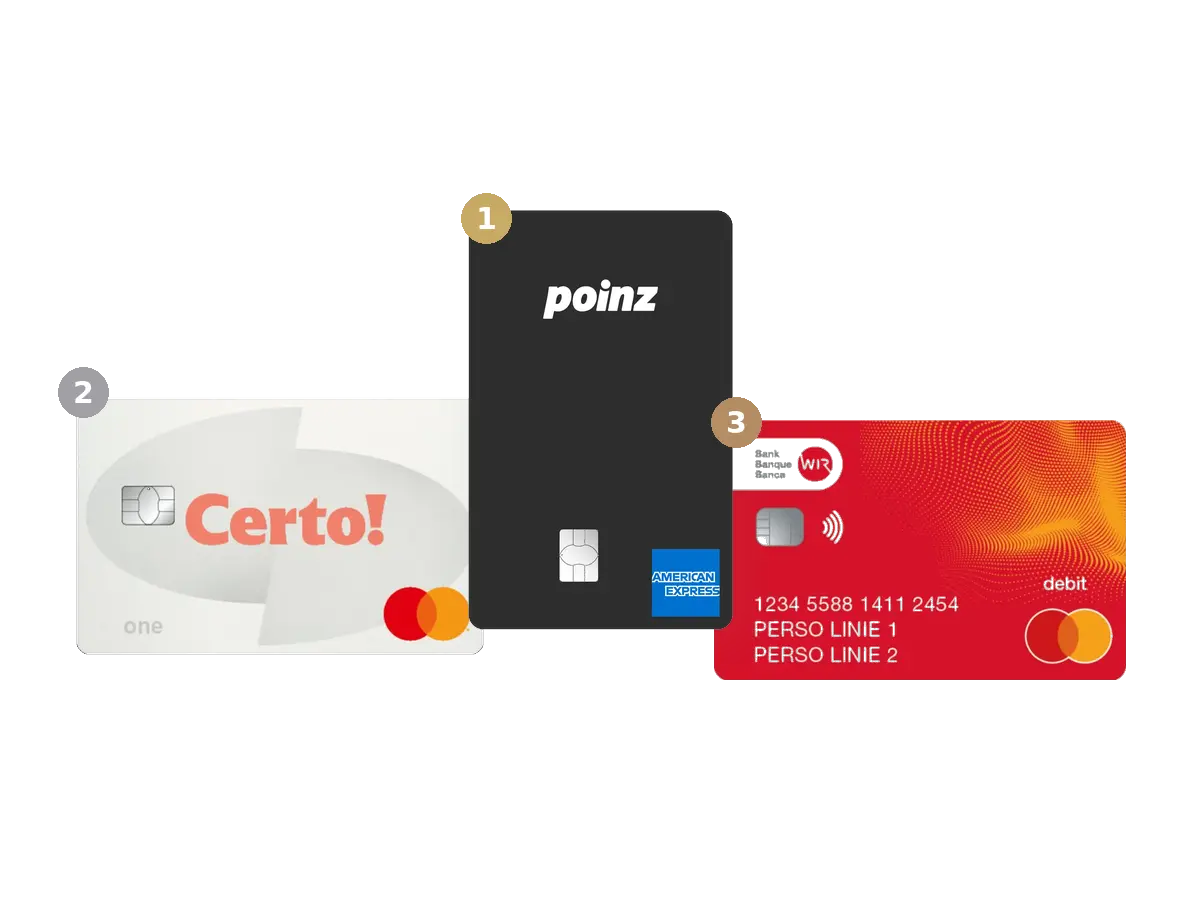

As a Mustachian, I want a credit card strategy that allows me to pay by credit card in Switzerland and abroad with as few transaction fees as possible, while earning as much cashback as possible. To do this, I need to use a system with three credit cards (not just one).

With this Swiss credit card strategy, you can earn around CHF 300 to CHF 400 in cashback per year, without doing anything (apart from making sure you pay your credit card bills on time).

Here are the credit cards I recommend:

| Main use case | Card | Cashback / fees | Why this is optimal |

|---|---|---|---|

| Switzerland (CHF), online and in-store | Poinz or Swisscard Cashback (Amex) | 1% cashback, zero fees | Best return in CHF everywhere Amex is accepted |

| Switzerland (CHF) when Amex is not accepted | Certo! One Mastercard | 1% at 3 favorite merchants, zero fees | Ideal complement to Amex to keep earning cashback |

| Abroad, foreign currency, CHF cash withdrawals, and when credit cards are not accepted | WIR Mastercard | Zero FX fees, 24 free withdrawals/year worldwide | Foreign currency payments at the best exchange rate, free withdrawals in Switzerland via Bancomat or Sonect |

All these cards are free, with no annual fee, and can be applied for easily online. Optimization doesn’t come from a single “premium” card, but from the right tool at the right time, depending on usage.

And if you only want one card for everything, then I recommend the WIR Mastercard.

Below, I’ll share with you my promo codes for additional welcome bonuses.

The optimal Swiss credit card strategy

I thought I could find one and only one best Swiss credit card to maximize my cashback. But there’s no such thing.

If you really want to pay zero monthly or annual fees, AND maximize your cashback, then you need more credit cards than one: a combination of three in total.

After a lot of research (and regular updating of this article), here are the free credit cards to use.

Card payments in Switzerland (CHF), online and in-store, when Amex is accepted

When a merchant accepts American Express, that’s when the cashback is most interesting, thanks to my favorite Amex credit card: the Poinz credit card.

Here are the detailed criteria behind this choice between Poinz and Cashback (the two best Amex credit cards among 70 analyses in my comparison):

| Criterion | Poinz | Swisscard Cashback |

|---|---|---|

| Annual fees | CHF 0 | CHF 0 |

| Amex cashback | 1% | 1% |

| Visa / Mastercard cashback | 0.25% (Visa) | 0.25% (Visa or Mastercard) |

| Cashback format | Real cash, transferable to your account from CHF 100 | Credit applied to a future statement |

| Payout timing | Immediately after each purchase | Once per year |

| Interest rate in case of late payment | 13% | 13% |

| Card types | Amex + Visa | Amex + Visa or Mastercard |

| Issuer | Swisscard | Swisscard |

Swisscard Cashback or Poinz credit card: which to choose? Both cards are free and offer exactly the same cashback rate. The difference lies elsewhere.

Here are the advantages of Poinz over Swisscard Cashback:

- With Poinz, cashback is real cash. You can request a bank transfer to your account as soon as you’ve reached CHF 100, and use it as you wish. With Swisscard Cashback, cashback can only be used as a credit on a future invoice.

- Poinz cashback is available immediately after purchase, which clearly improves flexibility. You don’t have to wait for an annual statement to take advantage of it (as is the case with the Swisscard Cashback credit card).

- You can also use your Poinz cashback in the form of special offers, deals or digital vouchers available in the Poinz app, if you find what you’re looking for.

- Poinz has directly integrated the logic of cashback platforms such as RabattCorner into the credit card itself. In concrete terms, if you make online purchases at partner merchants such as MediaMarkt or IKEA, you can earn even more cashback, on top of the standard 1%.

In practice, Poinz and Swisscard Cashback are very similar. But as soon as you look at the freedom of use and the timing of the cashback, Poinz is more advantageous.

Card payments in Switzerland (CHF) when Amex is not accepted

When Amex is not accepted, my strategy is to use the Certo! One Mastercard World.

I arrived at this choice after doing a comparison of about 70 Mastercard and Visa credit cards:

| Criterion | Certo! One Mastercard World |

|---|---|

| Annual fees | CHF 0 |

| Cashback | 1% at 3 favorite merchants [1], 0.25% elsewhere |

| Cashback format | Credit deducted from the credit card statement |

| Payout timing | Quarterly |

| Interest rate in case of late payment | 12% |

| Card type | Mastercard |

| Issuer | Cembra |

[1] The complete list of partner merchants (editable 1x per month) for the Certo! One Mastercard World is: Migros, Coop, CFF, Zalando, SWISS, Manor, Lidl, Decathlon, Aldi, H&M, Netflix, Spotify, Airbnb, Booking.com, Microspot, Digitec Galaxus, Ochsner Sport & Shoes, Interdiscount, Denner.

My verdict on the best card when Amex is not accepted by a merchant: the Certo! One Mastercard World card is the best complement. It allows you to keep cashback in Switzerland, with no annual fees, where Amex is not accepted.

Cashback is slightly less flexible than with Poinz, as it is deducted from your bill (rather than paid in cash) and credited quarterly. But for “fallback” use when Amex is not accepted, the simplicity/return ratio remains very good.

To optimize our credit card strategy in Switzerland as much as possible, we decided to select these three merchants to get 1% cashback with our Certo! One Mastercard:

- Lidl

- Aldi

- Denner

By combining a Poinz Amex card for maximum cashback and the Certo! One card when Amex is not accepted, I can already cover most of my payments in Switzerland, without fees or unnecessary complexity.

Foreign currency card payments and CHF withdrawals

The WIR Mastercard debit card is the best choice for payments in foreign currencies, whether from Switzerland (online payments) or abroad.

| Criterion | WIR Mastercard |

|---|---|

| Annual fees | CHF 0 |

| Foreign currency payments | 0% foreign transaction fees, interbank exchange rate |

| Weekend markup | None |

| Cashback | None |

| CHF withdrawals in Switzerland | 24 free withdrawals per year (no monthly limit) |

| Withdrawals abroad | 24 free withdrawals per year |

| Interest rate | None (debit card) |

| Card type | Mastercard |

| Issuer | Bank WIR |

My verdict for the best card for abroad, for foreign currency payments (including online shopping at foreign merchants) and cash in Switzerland: the WIR Mastercard is by far the simplest and cheapest solution.

Zero fees, interbank rate applied without any surcharge, and no exchange rate surcharge on weekends. So you avoid the 1.5% to 2.5% fees typical of Swiss credit cards.

This is also my card for cash withdrawals in Switzerland. The 24 free withdrawals per year more than cover normal use (cool bonus: these withdrawals are also free abroad, so there’s no withdrawal fee at all!)

And if I need extra cash, I simply use Sonect, which also offers free withdrawals in many shops.

With this combination of Amex Poinz Certo! One Mastercard in Switzerland, and Mastercard WIR for foreign countries and cash, I’ve got all my cashless payments covered, with no fees and no unnecessary high-end cards.

Real credit card fees in Switzerland (what really counts)

Annual credit card fees often get all the attention. In practice, they rarely cost the most. The real pitfalls lie in the invisible fees.

Most Swiss credit cards charge exchange fees on payments in foreign currencies. On your next trip or purchase abroad, these fees quickly exceed what the cashback can earn over a year.

Then there’s the notorious Dynamic Currency Conversion (DCC), when a terminal offers to pay in CHF abroad. The payment seems reassuring, but the exchange rate applied is almost always unfavorable.

This is why the word “free” does not mean “without cost”. A card with no annual fee can remain very expensive if misused.

I recommend that you read my article in which I explain in detail how exchange fees, the DCC and their real impact on your wallet work: “Save CHF 353.50 on your card fees abroad this summer!”.

Best credit cards by usage

For payments in Switzerland (in CHF)

- Verdict: if you pay mainly in Switzerland, the Amex (Poinz) + Certo! One is the best solution between maximum cashback and zero fees

- For whom: regular spending in Switzerland, monthly discipline

- Less suitable if: Amex is almost never accepted around your home (in the countryside, for example)

For online purchases (in CHF)

- Verdict: the Amex Poinz credit card with cashback is often the most profitable, especially if you can accumulate cashback via partners (Poinz “Online Cashback” function)

- For whom: CHF purchases, Swiss e-commerce

- Less suitable if: you make payments in foreign currencies, as exchange fees become exorbitant with these credit cards

For worldwide travel (payments in foreign currency)

- Verdict: abroad, the priority is not cashback, but exchange rate charges (surcharge, DCC, etc.): Mastercard WIR is the best option, with zero fees and an interbank exchange rate with no surcharges

- For whom: travel, foreign currencies

- Less suitable if: you’re hunting for cashback, but it’s not worth it, as the fees eat into your cashback in this case…

N.B. for pre-authorizations (hotel, car rental), I sometimes use my Certo! One credit card, as some establishments don’t accept debit cards. Then I ask to pay the final bill with my WIR Mastercard debit card (they don’t accept it all the time unfortunately, but it’s worth asking!). That way, I keep the credit card only for the booking, and avoid the huge exchange charges of a Swiss credit card when paying.

Backup card

- Verdict: a free Mastercard remains indispensable as Plan B (such as the Certo! One Mastercard), especially if you use Amex on a daily basis

- For whom: Amex users

- Less suitable if: you only want to use one card

Note: a classic debit card such as the Mastercard WIR can also play this role, especially for small amounts or in more rural shops where they don’t accept credit cards.

Credit cards with cashback in Switzerland: what’s the real payoff?

Cashback is often presented as an easy way to earn money. Yes, it’s true, it’s not complicated, but its impact remains modest and depends heavily on the conditions of use.

First of all: a 1% cashback only makes sense if you pay no annual fees, no interest and no exchange charges. As soon as one of these elements comes into play, the cashback quickly melts away, or even disappears altogether.

So, in practice, the order of priorities is simple:

- reduce your costs first

- and only then look for cashback

Because cashback is still a nice bonus, but it can never compensate for a poor cost structure.

Now that we’ve covered the necessary precautions, here’s the answer in pictures to the question of how much cashback you can really get from credit card cashback in Switzerland:

When optimizing your credit cards makes sense… and when it doesn’t

At the start of my professional career, I had a rather modest salary.

Every franc counted, and optimizing my spending was a simple lever to increase my savings rate, without changing my standard of living.

That’s when I started using cashback credit cards. For a few minutes’ effort, I could receive several hundred francs a year. The return on investment, both in terms of money and motivation, was excellent.

Then my situation changed.

As of 2023, between my family, my job and my entrepreneurial adventure, my time has become a much rarer resource than money. And reconciling several credit cards each month in my YNAB budget, even with a well-oiled system, took time for a gain that became marginal on the scale of my finances.

So I stopped actively optimizing cashback. Not because the method no longer worked, but because the return on the time invested was no longer aligned with my situation. You’ll find more details in my two articles: I’m blocking my credit cards for 1 year and My life without credit cards, 1 year later.

As said above, I now use the WIR Mastercard for my everyday use.

On the other hand, if I were to start again today at the very beginning of my FIRE path, with more time than money, I would do exactly the same thing.

Welcome promo codes

The blog offers you the following welcome promo codes for each card:

Poinz credit card promo code

You can use the following promo code to get a welcome bonus of CHF 100 in the form of a Migros gift card:

Poinz promo code: follow this Poinz link >

Swisscard Cashback American Express coupon code

Click on the link below to order your cards, and you’ll be entitled to a welcome cashback of 5% (for the first three months following card issue, on payments made with your American Express, up to a cumulative cashback total of CHF 100):

Swisscard Cashback promo code: follow this Swisscard link >

Certo! One Mastercard World promo code

Click on the link below to receive a CHF 50 welcome bonus when you order your Certo! One Mastercard World card:

Certo! One Mastercard promo code: follow this Cembra link >

Bank WIR promo code

Bank WIR does not offer promo codes as such. However, if you would like to support the blog, you can use my Bank WIR affiliate link below to open your account and start saving a lot of money with the Bankpaket top:

MP link for open your WIR account and order your WIR Mastercard debit card >

FAQ credit cards Switzerland

Are mobile contactless payment methods (Apple Pay / Google Pay / Samsung Pay) available with the cards you recommend?

Yes, Poinz, Swisscard Cashback, Certo! One and WIR cards all support smartphone payment services like Apple Pay, Google Pay and Samsung Pay.

Does Poinz have an app to track my spending during the current month?

Yes, Poinz offers a mobile app that lets you track your spending. However, the amount shown reflects what you’ve spent since your last invoice (not since the 1st of the month). Each invoice is issued on the anniversary of your sign-up date. So if you want the billing cycle to match the calendar month, sign up at the very end or very beginning of the month.

Why does Cembra offer two Certo credit cards?

If you’re wondering why Cembra has released two cards (“Certo! One” and just “Certo!”), my guess is that there’s been a contract termination agreement with Migros, and that the “Certo!” will disappear soon.

This seems to be confirmed by their FAQ: “To minimize changes for Cumulus-Mastercard customers, you can simply switch to the Certo! Mastercard. The Certo! Mastercard offers all kinds of advantages. Your credit card contract remains unchanged “.

Certo! One Mastercard World”, “Certo! Mastercard World”, or the new “Migros Cumulus Visa”?

Years ago, Migros’ Cumulus credit card was the best. But when their partnership with Cembra came to an end, it became a mess.

Overnight, we found ourselves with three new choices:

- Certo! One Mastercard World (Cembra)

- Certo! Mastercard World (Cembra)

- Migros Cumulus Visa (Migros Bank)

To cut a long story short, you have to choose the Certo! One Mastercard World from Cembra.

Indeed:

- The “Certo! Mastercard World (Cembra)” only offers 1% cashback at Migros, Coop and SBB. And you can’t change this list. Also, the insurance included is less attractive with this card (compared to the Certo! One)

- The “Migros Cumulus Visa (Migros Bank)” card only allows you to collect Cumulus points, which you can only use at Migros and not elsewhere

Certo! One Mastercard” or “Certo! One Mastercard World”?

These two names are used to designate the same card. Thank you very much for the simplicity dear Cembra…

What about credit cards with cashback in miles for free travel?

I had the same question several years ago, and, unfortunately, travel hacking doesn’t work in Switzerland…

I recommend you read my in-depth article: Travel hacking in Switzerland: why it doesn’t work (actual calculations).

What about Revolut compared to WIR?

The WIR Mastercard is cheaper. It applies the interbank exchange rate with no surcharge whatsoever, 7 days a week, with no amount limit. With Revolut Standard (free), you pay at the Revolut rate (close to the interbank rate) up to CHF 1'250 in conversions per month. Beyond that, Revolut adds a 1% fee. And watch out: on weekends, it’s also 1% on all conversions, even if you haven’t reached the monthly limit. In practice, if you’re spending a weekend at Europapark in Germany, Revolut automatically adds 1% to every payment on Saturday or Sunday.

Why does my Swiss credit card charge fees on online purchases in CHF?

Because the criterion is not the displayed currency but the country of the company that processes the payment. Even on a “.ch” site with a price in CHF, if the merchant’s headquarters is abroad, it’s considered an international transaction and foreign exchange fees apply (often between 1.5% and 2.5% depending on your credit card). To check, look at the site’s terms and conditions. For example, Zalando’s state “your contract partner is Zalando SE, Valeska-Gert-Str. 5, 10243 Berlin”. German headquarters = international transaction = fees. If that’s the case, use a card with no foreign exchange fees for that purchase instead.

Is credit card cashback taxable in Switzerland?

To the best of my knowledge, amounts received via cashback on your cards are considered a price reduction or discount on your purchases, and do not constitute taxable income to be declared on your Swiss tax return.

The Swiss tax authorities only include genuine income in income tax, not price discounts (see the logic behind “rebates / preferential prices” in the ESTV/AFC guide to the salary certificate on the ESTV/AFC website).

Can I use an Amex credit card at Migros or Coop?

Yes, Amex credit cards are accepted at Migros and Coop.

Are travel, purchase and cyber insurance worthwhile with a credit card?

I treat these benefits as additional bonuses. Especially travel insurance. But in reality, the day we went to an unsafe country, we took out dedicated travel insurance for maximum security. So, in the end, we don’t take these insurances into account when choosing our Swiss credit card.

Do you have any tips for credit cards for businesses?

Yes! After getting stung with 4.4% FX fees on my personal Certo! One card used for my LLC, I compared all the options and found the best solution for a business in Switzerland.

You’ll find my full comparison in this dedicated article: Best business credit card in Switzerland 2026.

Do I need a credit card that charges fees in Switzerland?

To date, I’ve found no advantage in having a paid credit card (with annual fees, aka conventional credit cards). Whether it’s for the insurance included, or for the extra Miles you can earn, I’ve done the calculations and in each case, it’s not profitable in the end.

Oh, and no, you don’t need one of those bling-bling Platinum credit cards to show off. On the contrary, you’ll soon realize the inner fulfillment that comes from having an online trading account filled with several hundred thousand CHF (vs. the little ego-satisfying spike when you pull out your Gold card, which only lasts… 3 seconds…)

How many credit cards can I have in Switzerland?

As many as you want, as long as you pass the credit check, but watch out for the effect on your organization, because it takes time to reconcile all this with your budget!

Conclusion: the Mustachian credit card strategy

If you want to increase your income by several hundred Swiss francs a year via credit card rewards (cashback), I recommend these:

- Poinz (Amex), to pay in CHF wherever possible

- Certo! One Mastercard, to pay in CHF where Amex is not accepted

- WIR Mastercard for foreign currency payments and ATM withdrawals (in CHF and foreign currency, up to 24x free withdrawals per year)

This credit card strategy has enabled me to earn between CHF 300 and CHF 400 in cashback per year.

And you, which credit cards do you use in Switzerland (and for what purpose)?