When the MP kids started getting pocket money, we did what every family does: cash and a little notebook. It was fun, educational, and it worked. Except I quickly realized that’s not their future reality. They’ll live with a banking app, a debit card, and TWINT.

So, well, better teach them to manage that now.

We opened them an account at BCV with the “Formule Juniors 7-14” package. And honestly, we’re still with them and happy. There’s TWINT, a card, an app, everything you need for daily life in Switzerland.

But during our last vacation in Italy, we had a small budget issue… Our oldest MP kid had received cash in Swiss francs for her birthday. So I told her to count how much she had, and that we’d advance her the euros (i.e. no rush to deposit that cash into her BCV account). Because our system is: we pay with our Banque WIR card to get the best exchange rate, and we settle up when we get home, then she transfers us the money.

Between the amount discrepancy (she messed up counting the bills and coins…) and the concept of the EUR/CHF exchange rate that she struggles to grasp, it was a bit of a drama… and I thought: “If only she had a multi-currency account…”

It’s not critical. But we’re the only ones in Europe living in CHF, and in her adult life, she’ll inevitably have online purchases in euros, subscriptions in USD, trips, etc. So I’d rather she understands these mechanics now than get burned on fees later.

And let me be honest: even though BCV is a good bank for young people, I’ve always had a bone to pick with some of their practices. Not to mention their fund management fees of 1-2% (gotta pay for the Porsche bonus, right). It makes me want to show my kids something different.

So I did what any good Mustachian would do: I compared all the teen account options available in Switzerland.

The best teen bank account in Switzerland in 2026 is Yuh 14+. It’s free, the exchange rates are at the interbank rate (0% markup up to CHF 5'000/month, more than enough for a teen), and most importantly: TWINT is fully integrated (not in prepaid mode!), which is really the most practical option for daily life in Switzerland.

For 12-13 year olds, it’s Zak or your cantonal bank that come out on top.

But before you jump in, let me explain why, and what alternatives to consider depending on your situation.

Which parent (or teen) is this comparison for?

This guide is for you if:

- You’re a Mustachian parent who wants to open a first bank account for your teen, without paying fees

- You want your teen to be able to pay with TWINT (it’s become indispensable among young people in Switzerland, from experience)

- You’re looking for a simple and secure solution, not a marketing product disguised as “financial education”

- Or you’re a Swiss teen looking for your first account on your own (kudos for reading my blog at your age, I’m jealous, you’ll be FI by 25!)

I've prepared this thorough comparison so you can enjoy your free time even more, for example with a hike on the Zueri Oberland-Hoehenweg trail :) (photo credit: myswitzerland.com)

By the way, if you’re looking for a bank account for adults, this isn’t the right article. Check out my comparison of the best bank in Switzerland instead.

How to choose a teen bank account in Switzerland?

The criteria for a teen aren’t exactly the same as for an adult. Your teen doesn’t receive a salary (unless they’re in an apprenticeship), doesn’t make SEPA transfers, and doesn’t need eBill. But there are things that matter a lot more to them.

Free teen account (zero base fees)

No way we’re paying monthly fees for a youth account. The good news: all teen accounts in Switzerland are free. That’s the bare minimum, and thankfully all banks have figured this out (they’re not dumb, they want to lock in young customers for later).

Integrated TWINT (not in Prepaid mode)

TWINT is THE payment method among teens in Switzerland. Splitting the bill for a kebab (oh wait, I’m told it’s now Tasty Crousty…), paying your share for the movies, buying on Ricardo or Tutti (no, not Temu please ^^)…

But be careful: there’s a big difference between full TWINT (linked directly to the bank account) and TWINT Prepaid (where you have to manually top up a balance). With prepaid mode, your teen will end up with a zero balance at the worst possible moment. This criterion alone eliminates some candidates for me.

Free debit card

To pay in stores and online. Ideally compatible with Apple Pay and Google Pay, because your teen will want to pay with their phone (and they’re right, it’s faster).

Minimum opening age

This is an important criterion depending on your teen’s age:

- From 7 years: BCV (Formule Juniors, then Formule Jeunes from 14)

- From 10 years: Raiffeisen

- From 12 years: UBS, PostFinance, Zak, Banque Migros, cantonal banks

- From 14 years: Yuh, ZKB

- From 15 years: neon

If your child is under 10, the accounts listed in this article aren’t accessible yet (or limited, without TWINT and/or without a debit card). In that case, check with your cantonal bank: most offer “children” or “junior” packages from age 7.

Parental authorization or not?

Several neobanks allow a teen to sign up without parental authorization. Traditional banks (UBS, PostFinance, Raiffeisen, Banque Migros) generally require a parental signature before age 18.

Zak has the lowest age for autonomous account opening (from 12), followed by Yuh (from 14) and neon (from 15). For a teen who wants to get started on their own, these three neobanks are the most accessible.

It’s up to you whether you prefer to keep control or empower your teen. Personally, I think it’s a good thing for a teen to manage their own account. That’s how they learn.

Intuitive mobile app

A teen uses their phone for everything (much to my dismay, but I’ll save that for another article). So you have a better chance of success with financial education if you put them on a banking app that’s clean, fast, and pleasant to use. The neobank apps (Yuh, neon, Zak) are generally much better than traditional banks on this front.

Foreign exchange fees for payments abroad

School trip to Berlin, online purchase on a euro website, Spotify subscription in USD (just kidding, they get the free tier, but you get the idea!)… Foreign exchange fees range from 0% (Yuh, up to CHF 5'000/month) to 2% (Zak, UBS debit card) depending on the bank, and some (BCV, Banque Migros) charge a flat fee per transaction rather than a percentage. Over a year, it can make a real difference.

Here’s what it looks like for a CHF 120 purchase abroad (e.g. a meal during a school trip):

| Bank | FX fees | Cost on CHF 120 |

|---|---|---|

| Yuh | 0% (interbank rate, up to CHF 5'000/month) | CHF 0.00 |

| neon | 0.35% | CHF 0.42 |

| UBS key4 (prepaid card) | 0.50% | CHF 0.60 |

| ZKB | 1.25% (capped at CHF 1.50/tx) | CHF 1.50 |

| Raiffeisen | 1.25% (min. CHF 1.50/tx) | CHF 1.50 |

| Banque Migros | CHF 1.50 flat/tx | CHF 1.50 |

| BCV | CHF 1-2 flat/tx + hidden markup | CHF 1-2+ |

| PostFinance | 1.5% | CHF 1.80 |

| Zak / UBS (debit card) | 2.0% | CHF 2.40 |

Note that ZKB caps its fees at CHF 1.50 per transaction, regardless of the amount. This cap becomes advantageous compared to percentage-based banks as the amount increases: above CHF 429, ZKB is cheaper than neon (0.35%). But for a teen, Yuh remains unbeatable with 0% exchange fees up to CHF 5'000/month (pure interbank rate).

Conversely, Raiffeisen has a minimum of CHF 1.50 per transaction (not a cap): on a small CHF 20 purchase, you still pay CHF 1.50 instead of the theoretical CHF 0.25 at 1.25%. That penalizes small amounts.

And as I said in the intro, this is what I want them to realize: added up, you quickly reach the price of a pair of Air Jordans after two or three years… and that, they understand ;)

Criteria that don’t matter much for a teen account

Savings interest rate

Rates change all the time, and with the SNB policy rate at 0%, they’re close to zero everywhere. Your teen isn’t going to get rich on savings interest.

As a Mustachian, we prefer investing rather than saving. If you’re still curious, you can read my guide to the best savings account in Switzerland.

Physical branch

Your teen isn’t going to walk into a bank (I haven’t set foot in one myself for… at least 5 years I think). They do everything on their phone. So it’s not an important criterion for me.

Investment tools

Investing at 14 is a great idea in theory. But that’s not the role of a basic bank account (because it’s not optimized, and it ends up costing a fortune).

Also, most teen accounts block access to investment products before age 18 anyway.

In the MP family, I explain in this article how we do it: How to Invest for Your Kids in 2026.

Candidates for best teen bank account in Switzerland 2026

After hours of research and comparing offers, here are the teen accounts I analyzed:

- Yuh 14+ (from 14 years)

- neon (from 15 years)

- Zak (from 12 years)

- UBS key4 banking Pure Young (from 12 years)

- PostFinance SmartYoung (from 12 years)

- ZKB Banking Young (from 14 years)

- Raiffeisen YoungMemberPlus (from 10 years)

- Banque Migros Free25 (from 12 years)

- BCV Formule Juniors / Jeunes (from 7 years, then Formule Jeunes from 14)

- Revolut Under 18 (from 6/13 years)

If you don’t see the account you’re looking for in this list, feel free to send me an email.

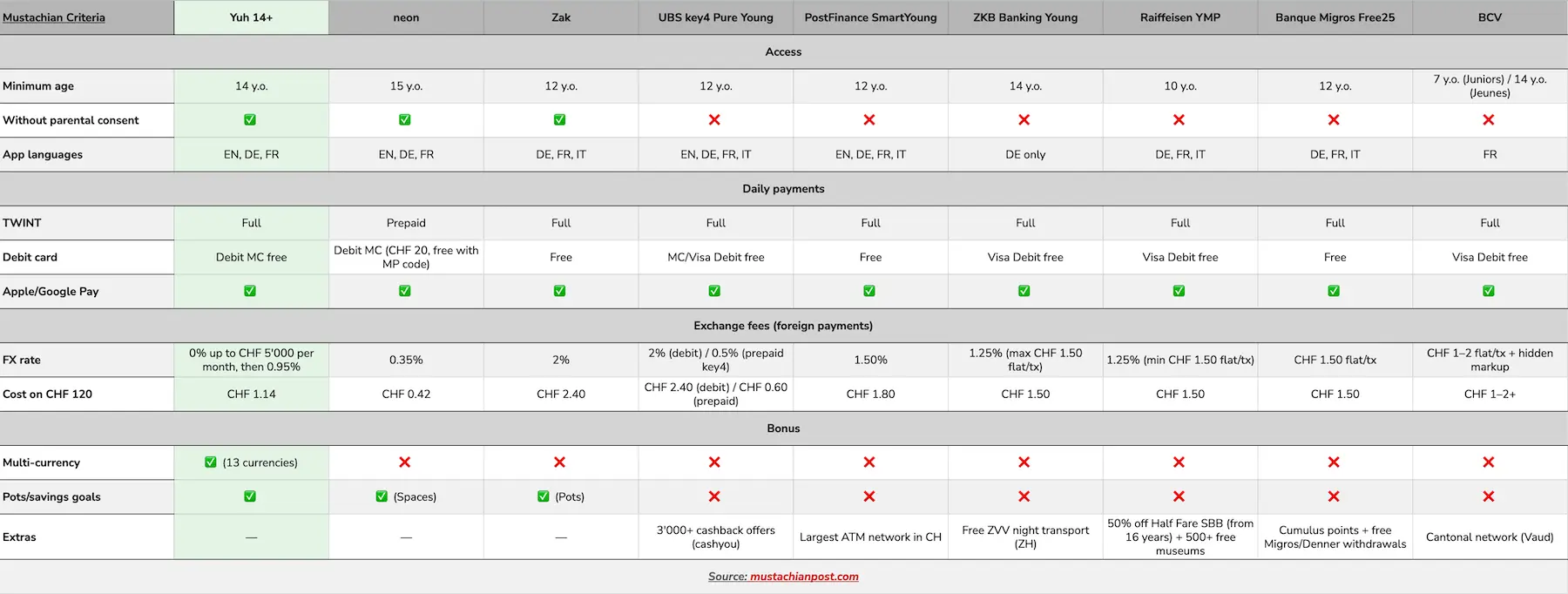

Comparison of the best teen bank accounts in Switzerland

Here’s the summary of my analysis of the best teen bank accounts in Switzerland:

Which teen bank account to choose in Switzerland: our pick for 2026

Yuh 14+: the best teen account in Switzerland

For teens aged 14 and above, Yuh 14+ is the best bank account in Switzerland. It’s the account I recommend to all the Mustachian parents around me.

This account checks every box:

- 100% free, no monthly fees whatsoever

- Free Debit Mastercard included

- Full TWINT linked directly to the account (not TWINT Prepaid)

- 0% exchange fees on 13 currencies up to CHF 5'000/month (pure interbank rate). Beyond that, 0.95%, but a teen will never (or very rarely) hit that ceiling

- Modern and intuitive app, well designed for young users

- Compatible with Apple Pay and Google Pay

You might wonder why Yuh and not neon? Because Yuh combines the best of both worlds: 0% exchange fees (interbank rate up to CHF 5'000/month) AND full TWINT. neon does have a low rate (0.35%), but its TWINT is in Prepaid mode only (you have to top it up manually), which is a real hassle for a teen who pays way more often in Switzerland than abroad.

With the free interbank rate up to CHF 5'000/month, Yuh really nails it with their Yuh 14+ product. Honestly, I can’t see a major reason to pick another bank for a teen aged 14 or above.

If your teen is 12-13 years old

For 12-13 year olds, Yuh isn’t available yet. My two main recommendations:

- Zak: the only neobank accessible from 12 (without parental authorization), with full TWINT and a modern app. But with 2% exchange fees (the worst of all candidates on this point, tied with the UBS debit card)

- Your cantonal bank (e.g. BCV Formule Juniors in the canton of Vaud): full TWINT and everything free, but also high exchange fees

And if you want to explore other options:

- Raiffeisen YoungMemberPlus: accessible from age 10 (and from 16, you get 50% off the SBB half-fare travel card = CHF 60/year in savings for a teen who takes the train)

- PostFinance SmartYoung: the largest ATM network in Switzerland

- UBS key4 Pure Young: large branch network + cashback deals (via cashyou)

- Banque Migros Free25: Cumulus points + free withdrawals at Migros/Denner

My pick for a 12-13 year old? It depends on your teen:

- If you want a modern app and autonomy for your teen, I recommend Zak (account opening without parental authorization from age 12)

- If you prefer sticking with your cantonal bank: go with BCV (or the equivalent in your canton)

- If you want the largest ATM network for whatever reason: PostFinance. And if you want a large branch network plus a nice cashback system: UBS

As I mentioned, we chose BCV at the time, because Zak wasn’t available for young people yet (availability came in 2025-2026 only).

If your teen is 14 or older

At 14, your teen gets access to Yuh 14+ which combines everything: full TWINT, 0% exchange fees (interbank rate up to CHF 5'000/month), and a multi-currency account. Hard to beat. From 15, neon is also an option with a low rate (0.35%), but its TWINT is in Prepaid mode only, which is a hassle in daily life. My pick:

- Yuh 14+: the obvious choice (full TWINT + 0% FX + multi-currency)

- neon 15+: if your teen doesn’t use TWINT (rare in Switzerland) and you want a different bank than Yuh

- Raiffeisen: if your teen takes the train regularly (from 16, 50% off the SBB half-fare travel card = CHF 60/year savings)

Detailed reviews of teen bank accounts in Switzerland

Yuh 14+ Review

Yuh was born from a project between Swissquote and PostFinance. For the banking side, it relies on Swissquote, regulated by FINMA (deposits protected up to CHF 100'000 via esisuisse). And since 2025, Swissquote is 100% owner of Yuh after buying out PostFinance’s shares.

The Yuh 14+ offer is identical to the adult account, but with investment features blocked until age 18.

In practice, your teen gets access to:

- A multi-currency account (CHF, EUR, USD and 10 others)

- A free Debit Mastercard

- Full TWINT (not Prepaid)

- 1 free ATM withdrawal per week in Switzerland (CHF 1.90 for subsequent ones)

- The interbank exchange rate on 13 currencies, with no markup up to CHF 5'000/month (0.95% beyond that, but what teen spends CHF 5'000/month in foreign currencies?)

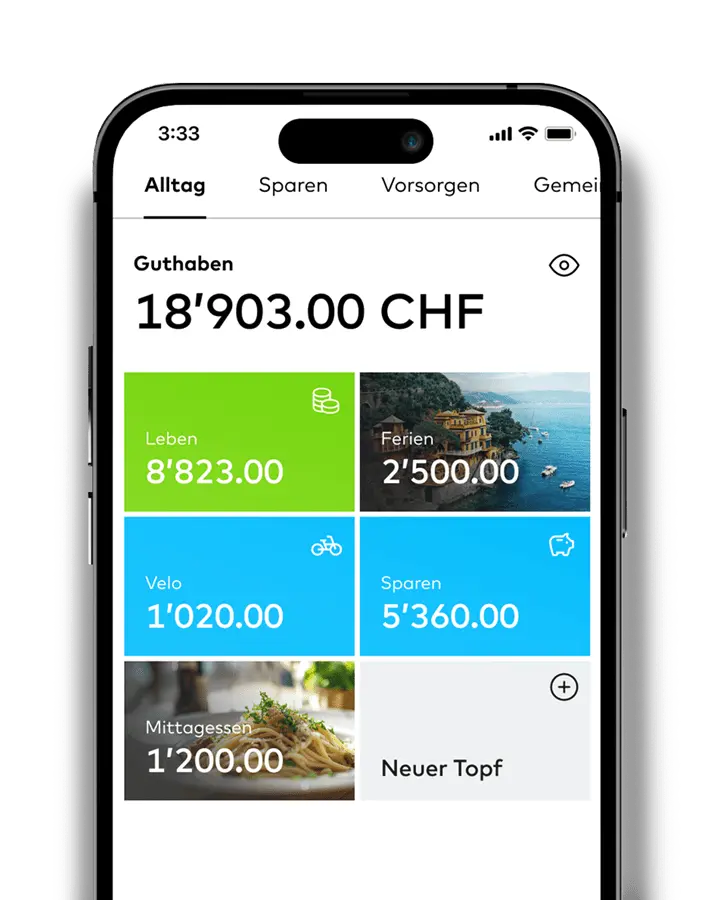

- Savings projects (similar to Zak/neon’s “Pots” or “Spaces”): your teen can create goals (new bike, trip, etc.) and transfer funds manually or via automatic savings (daily, weekly, or monthly transfer). Perfect for learning to save with a concrete goal.

The three strengths of Yuh 14+ for me are availability from age 14, 0% exchange fees (interbank rate), and the dedicated TWINT app. Zak also offers its youth account from 12, but Yuh keeps the edge with its unbeatable exchange rates and multi-currency account. These are the arguments that convinced me to choose Yuh 14+ over Zak.

If you want to learn more about Yuh, you’ll find all the details in my detailed Yuh review.

neon Review (from 15 years)

neon is one of the most popular Swiss neobanks, and it accepts customers from age 15 (without parental authorization).

The app is great, the “Spaces” (savings pots) are handy for a teen who wants to save for a specific goal. But there are two important drawbacks:

- TWINT only in Prepaid mode since fall 2025 (you have to manually top up the TWINT balance in the TWINT Prepaid app, and it’s really less convenient in practice)

- The debit card costs CHF 20 (unless you use the promo code below)

For a teen, TWINT Prepaid is really a hindrance in my opinion. You want your teen to be able to pay without the hassle of topping up their balance.

You’ll find all the details in my full neon review.

Zak Review (from 12 years)

Zak, the neobank from Bank Cler, accepts customers from age 12. The app is nice, the “Pots” system for separating savings by goal is well designed for a teen, and TWINT is fully integrated (via the separate Bank Cler TWINT app).

The weak points:

- 2% exchange fees on foreign currency payments (that’s a lot compared to Yuh’s 0% or neon’s 0.35%)

- No English app (only FR, DE, IT), in case you’re an expat

For a main account, Yuh is ahead. Zak can serve as a complement, but it’s rarely necessary for a young person.

UBS key4 banking Pure Young Review (from 12 years)

UBS offers its key4 banking Pure Young package from age 12 (in-branch opening required for 12-13 year olds, online from 14).

What’s good:

- Free debit card (Mastercard or Visa Debit)

- Free prepaid card on top (handy for payments abroad with only 0.5% surcharge, but that means managing multiple cards)

- Full TWINT

- 3'000+ cashback offers via the cashyou platform

The big flaw: 2% surcharge on foreign currency payments with the debit card. If your teen chooses this bank and travels, they’ll need to use the prepaid card abroad (only 0.5%)… not super convenient, and a coin flip whether they’ll remember…

Open a UBS key4 Pure Young account >

PostFinance SmartYoung Review (from 12 years)

PostFinance is the accessibility pick. With the largest Postomat network in Switzerland, your teen will always find an ATM nearby.

The advantages:

- Largest ATM network in Switzerland (Postomats + all other ATMs)

- Full TWINT linked to the account

- Free withdrawals at all ATMs in Switzerland (on top of Postomats)

- Free PostFinance card + free prepaid Mastercard

The main drawback:

- 1.5% surcharge on foreign currency payments

Open a PostFinance SmartYoung account >

ZKB Banking Young Review (from 14 years)

ZKB Banking Young is accessible to any Swiss resident (you don’t need to live in the canton of Zurich). The offer is free and includes a unique bonus for Zurich residents: free ZVV night transport on Friday and Saturday evenings (Nachtschwärmer). For a Zurich teen who goes out on weekends, it’s a nice bonus.

What’s included:

- Free Visa Debit card

- Full TWINT

The downsides:

- 1.25% exchange fees, capped at CHF 1.50 per transaction (you never pay more than CHF 1.50, regardless of the amount)

- The app and website are only available in German. For French-speaking or English-speaking families, that rules them out (unless you want to use it as German vocab practice for your teens :D)

- The Nachtschwärmer (ZVV night transport) is limited to the canton of Zurich (but the account itself is open to any Swiss resident)

Open a ZKB Banking Young account >

Raiffeisen YoungMemberPlus Review (from 10 years)

The 50% discount on the SBB half-fare travel card is Raiffeisen’s main selling point. For a teen who takes the train to school or on weekends, that’s CHF 60 in savings per year. That’s more than any savings interest rate could yield on a teen account.

The offer also includes:

- Free Visa debit card (1.25% FX, min. CHF 1.50)

- Full TWINT

- Free entry to over 500 museums in Switzerland (via the Raiffeisen membership card)

- Discounts on concert tickets

However, the 1.25% exchange fees (min. CHF 1.50/tx) are on the high side.

And be aware: Raiffeisen is a cooperative of 200+ local banks. The exact conditions vary from one Raiffeisen to another. Check with your local cooperative before opening the account.

Open a Raiffeisen YoungMemberPlus account >

Banque Migros Free25 Review (from 12 years)

If you shop at Migros, the Free25 account from Banque Migros has some nice perks:

- Cumulus points on debit card payments

- Free withdrawals at Migros and Denner checkouts (no ATM needed)

- Quarterly Free25 vouchers for discounts (restaurants, fitness, travel)

- Full TWINT from age 12

The weak points:

- The app is functional but not as modern as the neobanks

- CHF 1.50 flat fee per foreign payment with the Visa Debit (flat amount, not a percentage)

Open a Banque Migros Free25 account >

BCV Formule Jeunes Review (from 14 years)

This is the account my kids have been using from the start, with the Formule Juniors (7-14 years), then the automatic switch to Formule Jeunes (14-20 years). And I’ll be upfront: for daily life in Switzerland, it’s solid. There’s full TWINT, a Visa Debit card, and the app gets the job done.

But there are some limitations:

- No multi-currency. That’s precisely what pushed me to write this article. For a teen who travels or shops online in euros, it’s a gap.

- Flat exchange fees: CHF 2 per in-store payment abroad, CHF 1 per online payment in foreign currency. It’s a flat amount (not a percentage), which is advantageous on large amounts but expensive on small purchases. And watch out: BCV applies its own exchange rate (not the interbank rate), so there’s a hidden markup on top of the flat fees. No thanks!

It’s a decent regional option for people in the canton of Vaud, but with no particular advantage over Yuh or the national banks listed above.

Open a BCV Formule Jeunes account >

Notes on Revolut and N26

Revolut Under 18

Revolut offers a youth product (Kids from 6, Teens from 13), with good exchange rates and well-designed parental controls. But for a Swiss teen, there’s one dealbreaker:

- No TWINT. That’s a non-starter in Switzerland (at least from our experience with our kids)

Another downside: the parent must also have a Revolut account to create a Teens account, and the teen can’t receive regular bank transfers (no personal IBAN, only transfers between Revolut users and payment links are possible).

For all these reasons, I don’t recommend Revolut as a primary account for a teen in Switzerland. It could potentially serve as a supplementary travel card for exchange rates, but I prefer the simplicity of Yuh 14+.

N26

N26 is simply not suitable for a Swiss teen, for several reasons: the account is only accessible from 18, the IBAN is in euros (not CHF), there’s no TWINT, and the bank doesn’t have a Swiss license. Next please :)

FAQ

At what age can a teen open a bank account in Switzerland?

There is no legal minimum age to open a bank account in Switzerland. What matters is the teen’s capacity for discernment, meaning the point at which they’re deemed able to make financial decisions independently. Each bank assesses this on a case-by-case basis and sets its own age limits.

In practice: from 10 at Raiffeisen, from 12 at UBS, PostFinance, Zak, and Banque Migros, from 14 at Yuh, ZKB, and BCV, and from 15 at neon. Neobanks don’t require parental authorization. Traditional banks generally require a parental signature before age 18.

Does a teen need TWINT in Switzerland?

Yes. TWINT has become the go-to payment method among young people in Switzerland.

I wouldn’t have believed it would take off compared to Apple Pay or Google Pay several years ago, but I have to admit they’ve managed to conquer the Swiss market.

For a teen, according to our kids, it’s the simplest way to pay back a friend, pay at a youth canteen, or buy at the cafeteria. So in the MP family, a teen account without full TWINT (not Prepaid) is a genuine reason to pass on that banking option, from experience.

What’s the difference between “full” TWINT and “Prepaid” TWINT?

Full TWINT is directly linked to the bank account: payments are automatically debited from the balance. TWINT Prepaid requires manually topping up a balance before you can pay. It’s less convenient, especially for a teen who risks ending up with a zero balance at the worst possible moment.

Is my teen’s money safe in a youth account?

Yes, for all Swiss accounts listed in this comparison (Yuh, neon, Zak, UBS, PostFinance, ZKB, Raiffeisen, Banque Migros, BCV). They’re regulated by FINMA, and deposits are protected up to CHF 100'000 via esisuisse. The only exception is Revolut, which operates with a Lithuanian banking license (protection up to EUR 100'000 under the Lithuanian system).

Can a teen use Apple Pay or Google Pay with their account?

Yes, most listed accounts are compatible: Yuh, neon, Zak, UBS, PostFinance, ZKB, and Banque Migros all offer Apple Pay and/or Google Pay. Check the specific compatibility with your teen’s phone when opening the account.

Should I get a separate teen account or a sub-account under the parent’s name?

I recommend a separate account in the teen’s name. It teaches them to manage their own money, it’s simpler for payments between friends (TWINT in their name), and it builds responsibility.

Do free teen bank accounts exist in Switzerland?

Yes, all teen accounts listed in this comparison are 100% free (zero account maintenance fees). That’s the case at Yuh, neon, Zak, UBS, PostFinance, ZKB, Raiffeisen, Banque Migros, and BCV. Banks offer free accounts to young people to lock them in as future adult customers. Just watch out for possible ancillary fees: exchange fees abroad, out-of-network ATM withdrawal fees, or card replacement fees in case of loss. These vary by bank and are detailed in my reviews above.

Conclusion: the best teen bank account in Switzerland

To the question “what’s the best youth account in Switzerland?”, my answer is clear:

- Teen aged 12-13: Zak or your cantonal bank.

Zak is the only neobank accessible from 12, with full TWINT and no parental authorization. Otherwise, your cantonal bank (or Raiffeisen from 10) can be a good pick too. - Teen aged 14 and above: Yuh 14+.

It’s free, full TWINT, 0% exchange fees (interbank rate up to CHF 5'000/month), multi-currency account, and your teen can open it on their own. Honestly, it’s the perfect teen account. - Teen aged 15 and above: still Yuh 14+

Yuh, which also dominates on exchange fees. neon (0.35% exchange fees) remains an alternative if your teen doesn’t use TWINT, but that’s rare in Switzerland. And if your teen takes the train, there’s also Raiffeisen from age 16 for the 50% discount on the SBB half-fare travel card (= CHF 60/year in savings).

The good news: all these teen accounts are free. So there’s no excuse not to open one as soon as your teen is old enough to manage their own money. It’s the best financial education gift you can give them, long before an ETF or a 3a pillar.