Last updated: July 13, 2024

2024 Finpension 3a Promo Code

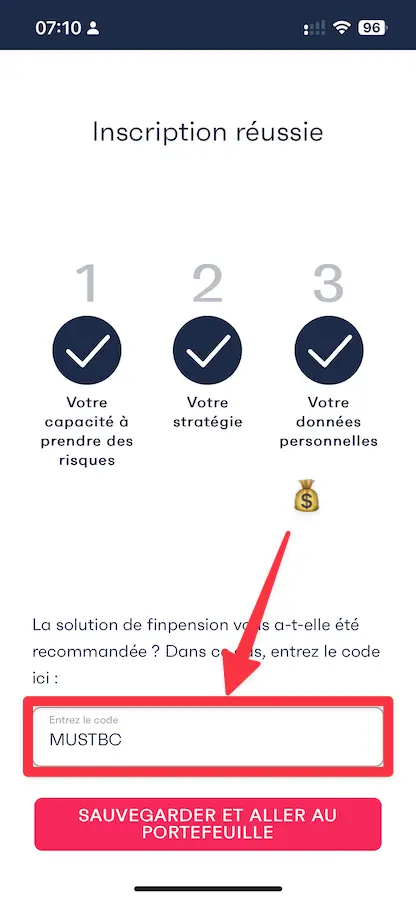

Use the promo code "MUSTBC" when registering on the finpension app.

You will receive a fee credit of CHF 25 as a welcome bonus, if you transfer or deposit at least CHF 1'000 within the first 12 months after creating your finpension account (and you'll help support the blog in the process, thanks!)

- finpension 3a in short

- What is finpension 3a concretely?

- Why is finpension 3a one of the best 3rd pillar solutions for Mustachians?

- User reviews about finpension 3a

- Alternative solutions to finpension 3a - and their comparison

- How to open a finpension account within 10 minutes

- My exclusive interview with the CEO of finpension

- FAQ about finpension 3a

- Conclusion

You can pat yourself on the back if you’ve just joined the FIRE movement (“Financial Independence, Retire Early”).

In fact, when I started my career as a Swiss Mustachian in 2013, there weren’t any fintechs available like the ones we have today.

And especially in the 3rd pillar sector…

The only option I had at the time to optimize my investment was to open a 3a pillar in the canton of Lucerne!

Luckily, today, many 3rd pillar fintech solutions have emerged, to our benefit as small private investors. These enable us to invest our private pensions in index funds and other ETFs optimized for maximum diversification and returns while keeping costs to a minimum.

finpension 3a in short

Briefly, here’s my take on the finpension 3a 3rd pillar, starting with the advantages of finpension 3a:

What I like about finpension’s 3a services

- Tax optimization when you withdraw from your 3rd pillar if you move abroad (your withdrawn capital is then taxed in the canton of your 3a provider), because the foundation behind finpension is headquartered in the canton of Schwyz (which has the lowest withholding tax rate on pension capital benefits in Switzerland at 4.8% — compared to the 10.3% which VIAC has in the canton of Basel, but I’ll explain a solution to get the best of both worlds below)

- Diversification in the event of bankruptcy for fraudulent management that would cause you to lose everything at VIAC - which I firmly believe won’t happen anytime soon, as we saw when the bonds issued by Crédit Suisse vanished in a weekend…

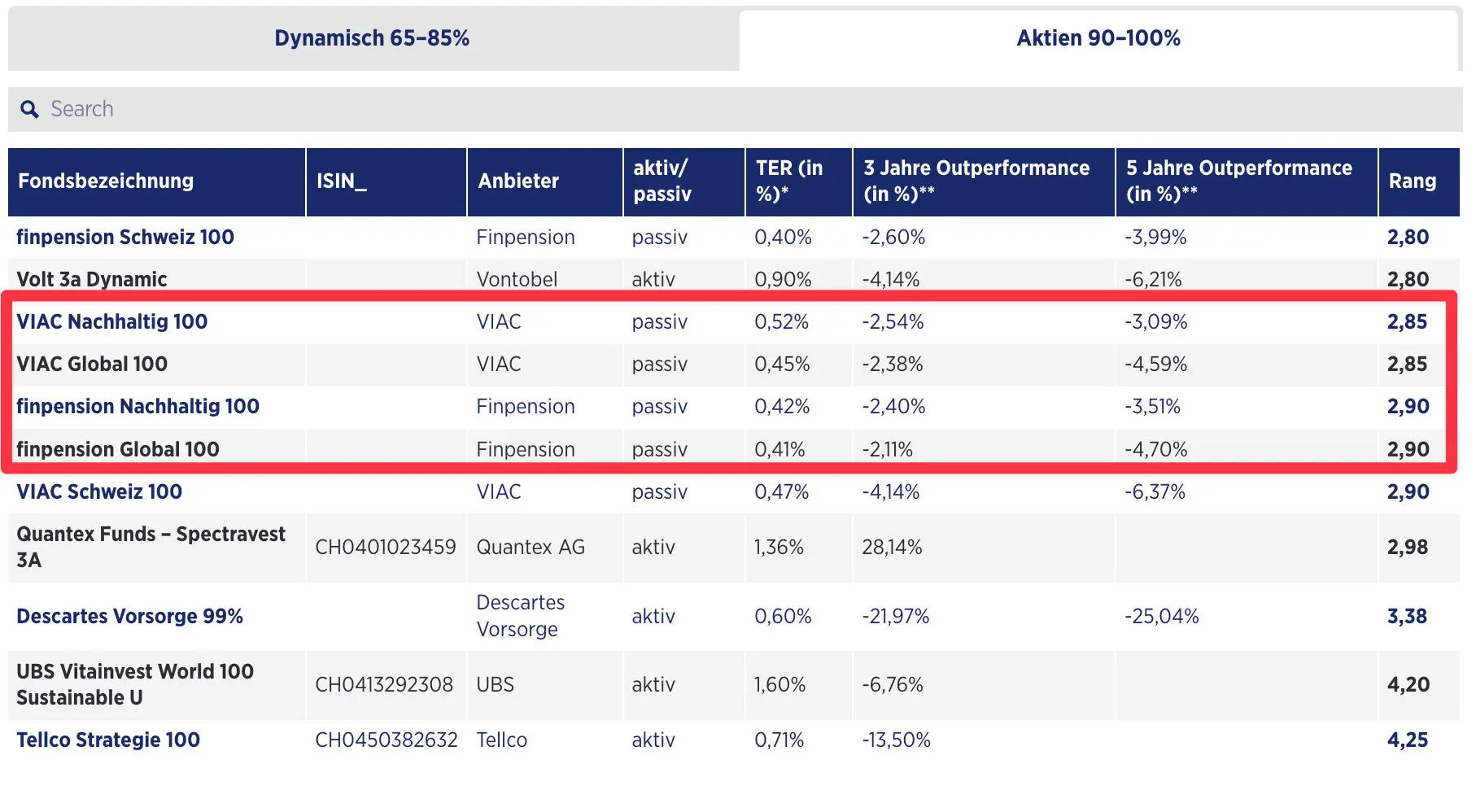

- Nearly equal with VIAC, the best 3rd pillar in Switzerland. Indeed, finpension is just 0.05 points behind VIAC (Handelszeitung score). That’s almost non-existent!

What could finpension do better in the future?

- Exceed VIACs Handelszeitung score for our 3rd pillar 100% stock strategy. And then, frankly, it would be number #1

- Offer a mortgage solution at a really great rate (especially in SARON) like VIAC does with the WIR bank. And above all, you’d need to do the same thing with a mortgage that accepts your Pillar 3a funds as collateral!

And honestly, that’s all I can find at the moment, so finpension 3a is one of the best private pension solutions.

MP’s Recommendation

I recommend that all Swiss Mustachians follow a strategy of opening multiple 3rd pillar accounts to maximize your tax savings upon your withdrawal.

Here’s what I mean:

- Open 3x 3a pillars with VIAC

- Open 2x 3a pillars with finpension

Then you allocate 3/5 of your maximum annual 3rd pillar amount to VIAC and send the other 2/5 to finpension.

This is the investment strategy that Mrs MP and I have been following since the beginning of this year (i.e. since we were finally able to close that damned mixed 3rd pillar linked to life insurance!)

What is finpension 3a concretely?

finpension 3a is a 3rd pillar solution.

You must be new to the blog if you’re wondering: “What’s a 3rd pillar again?”

Basically, a 3rd pillar is like a smart piggy bank for your retirement. It’s a tax-advantaged way of putting money aside every year. The money you pay into your 3rd pillar is deducted from your taxable income, which means you pay less tax.

But as a Swiss Mustachian, you don’t just want to pay less tax with your private pension piggy bank.

You also want the money in that piggy bank to multiply, just like all of your other stock market investments.

And you want to do it with a Swiss fintech that offers you the lowest fees on the market. In other words, not one of those big old Swiss banks that seriously abuse their fees to finance their Porsche via their end-of-year bonuses!

And that’s exactly what finpension 3a offers you.

With finpension 3a, you can select one of many different investment profiles, from the most cautious to the most daring (just like Mustachians, you’ll certainly be on the “more daring” side!), according to your personal preferences. Your money is invested in index funds to grow over time.

The aim is to build up a nice nest egg for your retirement while benefiting from tax advantages.

But suddenly, you ask yourself: why is the finpension 3a so special compared to other competitor solutions?

Why is finpension 3a one of the best 3rd pillars for a Mustachian?

The 3rd pillar of finpension 3a is the second best (almost equivalent to the first) for all Swiss Mustachians. From the finpension application for opening your account and tracking the performance of your 3a to the maximized returns of your investment portfolios, finpension rocks.

Mustachian criteria for selecting your Swiss 3rd pillar plan

Let’s be clear, we Mustachians are a special breed ;)

So concretely, here are the criteria I use to judge whether a 3a pillar is the best or not:

Criteria 1 - “100% global stock” strategy

You want to be able to invest the maximum amount of your 3rd pillar in 100% global equities (via index funds) And, in order to cover the whole world for optimum risk/return ratio through diversification of the companies in which your money is invested.

Criteria 2 - The best return (including fees)

For the past few years, I compared all types of 3rd pillar fees in detail to choose the best one.

But since 2023, I’ve been using nothing except for the Handelszeitung score published at the end of each year to make my choice.

In fact, the Handelszeitung score not only takes the best return into account but also all of the fees :)

So what I want from now on, as a Mustachian, is THE pillar 3a with the best return all fees included.

Criteria 3 - A secure 3rd pillar via formal identification

I want a secure 3a pillar where my identity is verified when I open my account, and not just when I withdraw my assets.

This is exactly what finpension did until 2023. And it was totally legal. Except that I didn’t really like the idea of being able to create a finpenion 3a account with the name “Donald Duck” and still receive an account… or even worse, but imagine typing a typo in your first name… you wouldn’t see the problems until many years later, just when you wanted to start withdrawing from your 3rd pillar!

So, for me, formal identification is very important when opening a 3a account.

FYI: finpension 3a corrected the situation in April of 2023, and now offers formal identification when you open your 3rd pillar account. It’s an option when you register, and I highly recommend it.

✅ The finpension 3a solution fulfills all three criteria. With a damper on the Handelszeitung score, which ranks finpension 3a second behind VIAC, only a slight difference.

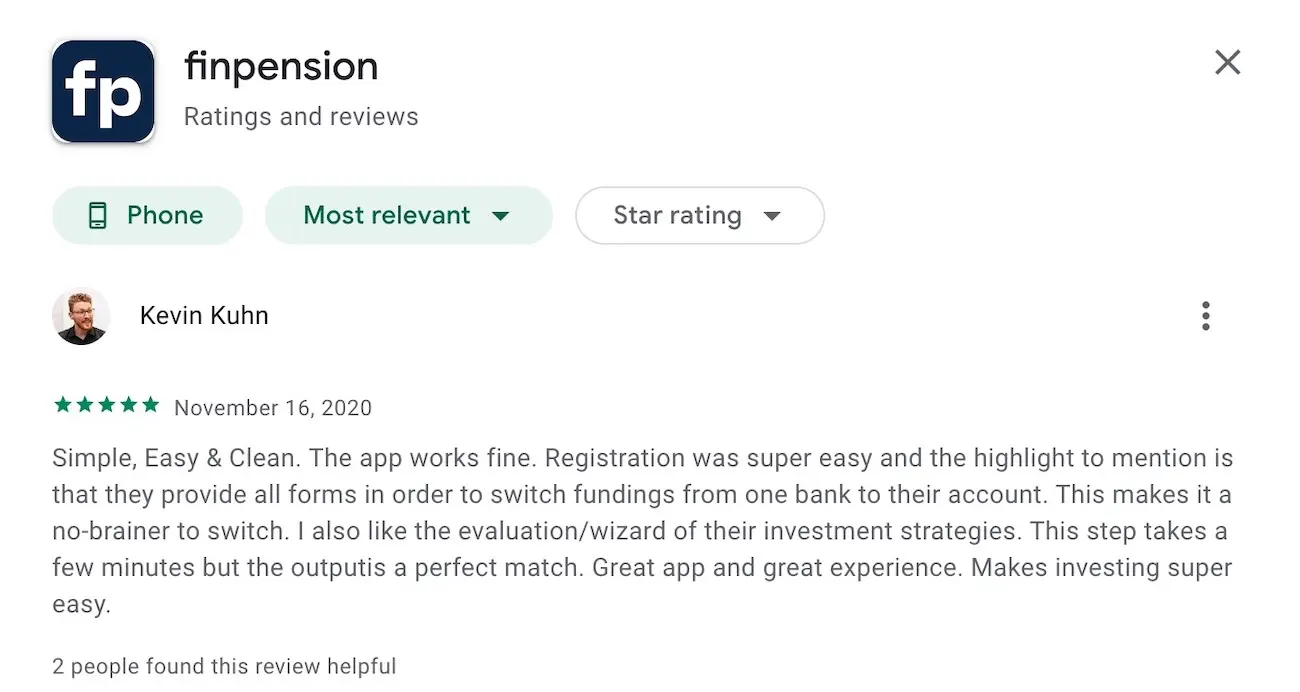

User reviews about finpension 3a

I like to go and look at app store ratings when a service I use has a mobile app.

After all, when customers are unhappy, one of the first things they do is make their negative review as visible as possible :)

Personally, when I see a mobile app exceeding 4/5 stars on the app stores and there are more than 20-40 reviews, then I feel reassured.

Here are the average ratings for the finpension app on the iOS and Android app stores:

Everything looks fabulous :)

And here are some comments in general about finpension 3a:

You can also use these links to check out the most recent reviews of the finpension iOS app and the finpension Android app depending on your smartphone OS.

Alternative solutions to finpension 3a — and their comparison

finpension 3a vs VIAC

finpension 3a is mathematically the second-best 3rd pillar (for a 100% equities strategy). It ranks behind VIAC with 0.05 less in the Handelszeitung score. This ranking takes everything into account from the highest returns to the lowest fees. finpension 3a nevertheless remains one of the leaders in the 3a market.

As mentioned above, I myself use an investment strategy combining both VIAC and finpension 3a to diversify my risk of depending entirely on one or another platform.

So I didn’t have to choose so much: I opted for 3 out of 5 portfolios with VIAC, and opened my other two 3a portfolios with finpension :)

finpension 3a vs frankly

The result is undisputed in the Handelszeitung ranking list: finpension 3a outperforms frankly. The simple reason is: that finpension 3a allows you to hold up to 99% of shares in stock market investments, whereas with frankly you can only hold 95%. Fewer shares = less performance.

finpension 3a vs True Wealth

True Wealth is one of the latest stock-market-invested 3rd pillar solutions to hit the market. It has caused quite a stir, as True Wealth offers a 3rd pillar without any management fees.

A first in Switzerland!

Nevertheless, there are two factors that make me prefer finpension 3a than True Wealth:

- The cost of regulations of True Wealth’s 3a Pension Foundation state that the foundation council may introduce a management fee of up to 0.225% per annum on the equities portion - a point which is reassessed each year…

- The finpension 3a solution remains the best in terms of its Handelszeitungs score :)

finpension 3a vs Descartes Vorsorge

The Descartes Vorsorge 3rd pillar solution (also known as Descartes Vorsorge 99%) is not as good as finpension 3a. This could be due to its active management, which involves higher costs than passive management (such as finpension). In any case, its Handelszeitung score is lower than finpension’s.

finpension 3a vs Selma

finpensions 3rd pillar is better than Selma’s for a Mustachina investor wishing to invest 100% in equities. Indeed, finpension 3a allows you to invest up to 99% in equities (via index funds), compared with only 97% maximum for Selma’s 3rd pillar. Less equities means less return.

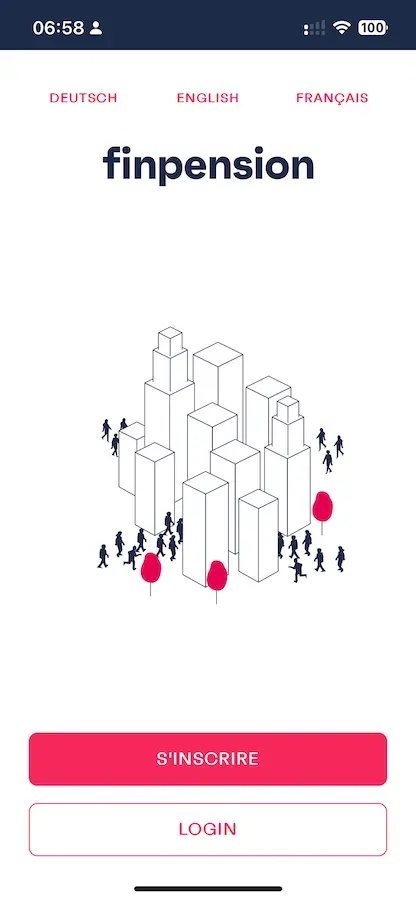

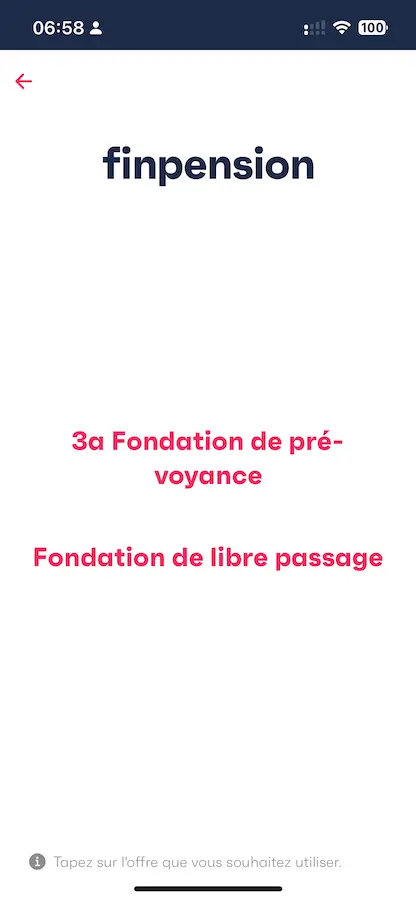

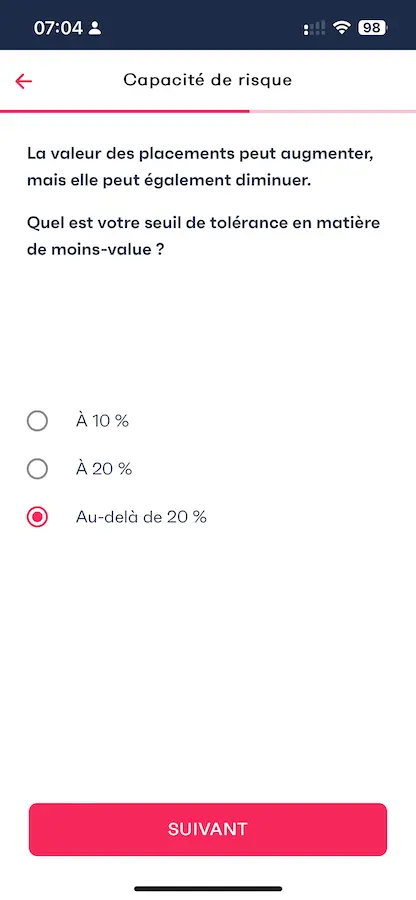

How to open a finpension account in 10 minutes

It’s pretty crazy how in 2024 you can open a 3rd pillar account in literally ten minutes!

And this, without any sneaky advisors trying to sell you their mixed 3rd pillar life insurance (REMINDER: NEVER SIGN UP FOR ONE!!!)

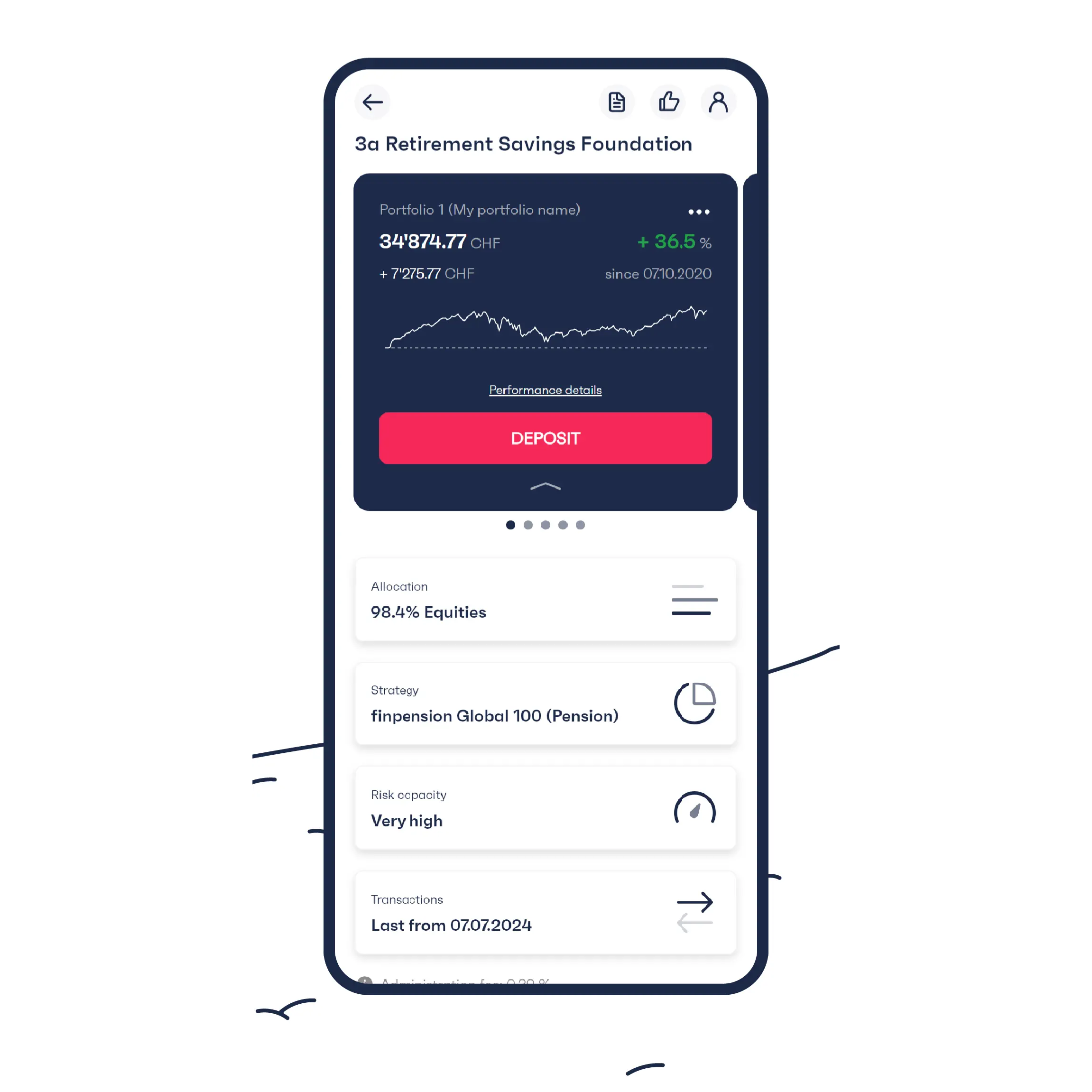

I’ve made a few screenshots below to give you an idea of what the finpension 3a registration process looks like.

The whole process is digitized via the finpension mobile app (or via their web app), and can be summarized in 4 main steps:

- Download the finpension app (iOS AppStore, Android Google Play Store) on your smartphone, or go to their application web

- Answer a few questions to define your risk profile

- Choose your 3a pillar investment strategy

- Enter your personal data

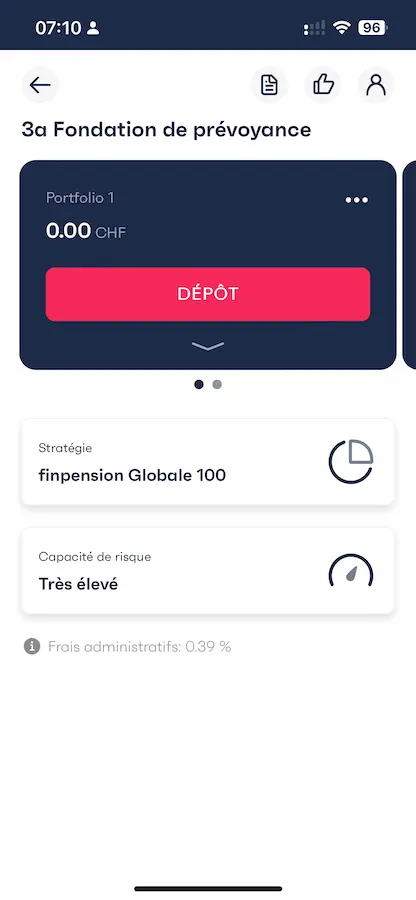

Choose the type of account you want to open in the finpension app (for us it's '3a Pension Creation')

Choose your investment portfolio type (in our case, it's 'Global' to maximize our risk/return ratio)

Choose your fund company (personally, I'm more comfortable with Swisscanto funds than Credit Suisse funds - especially as it makes no difference to you as an investor!)

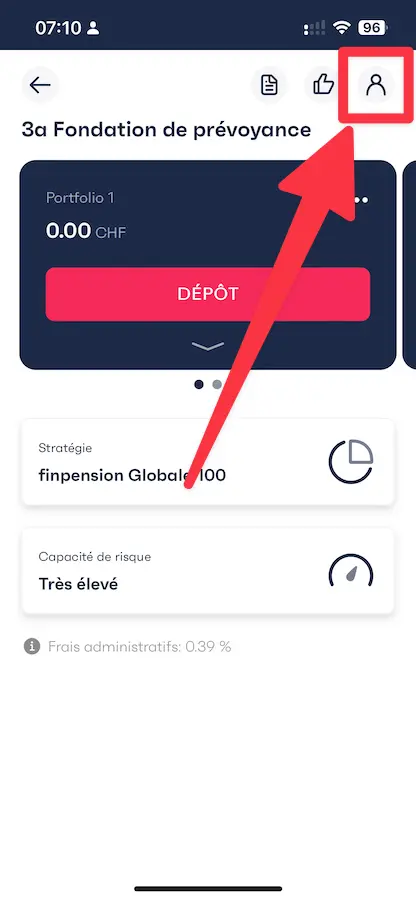

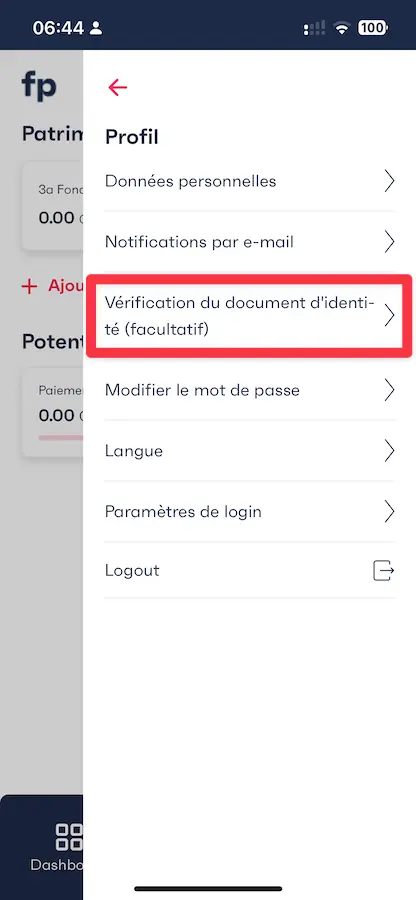

And as I was saying, don’t forget to carry out your formal identification so that you don’t have to worry about withdrawing your 3rd pillar assets.

To do that, you just need to go to the finpension app, click on the profile icon, and then on “identity document verification (optional)”:

And there you have it! Now all you need to do is make your first transfer to your finpension 3a pillar. Or even transfer all your existing 3a (especially if it’s a mixed 3rd pillar!!) in just a few clicks.

I think it’s never been easier to save for your (early) retirement ;).

My exclusive interview with the CEO of finpension

I was lucky enough to be able to interview Beat Bühlmann, CEO of finpension.

We were able to discuss a wide range of topics, including his story, career advice and the merger topic between finpension and VIAC.

You can find the full interview on this link.

FAQ about finpension 3a

Who founded finpension 3a?

finpension AG was founded by Beat Bühlmann. Beat Bühlmann had already worked in the financial sector. He was soon joined by Ivo Blättler, a former colleague from a Swiss private bank. They began by revolutionizing the 1st pillar, then the 2nd (vested benefits), and in 2020 the 3rd pillar.

Where is finpension AG headquartered?

The finpension AG headquarters are located in the beautiful city of Lucerne.

Why is only 99% and not 100% of my finpension 3a money invested in stocks?

All 3rd pillar providers invest a maximum of 99% of their savings in equities via index funds, as it must retain 1% in cash to debit its fees.

It’s as simple as that :)

Can I leave some cash lying around without investing it in finpension 3a?

Not really. But you can invest your money in a money market fund, which is almost the same as cash in liquid form.

How much money should I set aside each year in my 3rd pillar?

The answer for any self-respecting Mustachian: your aim is to fill your 3rd pillar to the maximum legal amount in 2024, i.e. CHF 7'056!

This is due to the fact that we want to take maximum advantage of tax deductions.

Once that’s done, you invest all the rest of your savings in the stock market.

Conclusion

finpension 3a is an excellent 3rd pillar solution. The second best, to be precise, for us Mustachians living in Switzerland.

Given the 0.05 point difference between finpension and VIAC in the Handelszeitung score, I’ve decided to diversify all our 3a assets between VIAC and finpension from 2023.

Basically, we have to put CHF 3'700 in VIAC for our mortgage with the WIR bank. This is a good thing since we wanted to put more money in VIAC than in finpension.

And knowing that the 2024 maximum 3rd pillar amount is CHF 7'056 (for a standard employee), this means we’ll be paying CHF 3'356 every year to finpension.**

The only way finpension could improve is by increasing the performance (Handelszeitung score) of its index fund investment strategies. And, secondarily, in the other services provided to its customers, such as a mortgage that’s better than all of the competitors.

While we wait, my recommendation for all MP blog readers is: to invest your savings in your 3rd pillar up to the maximum allowable amount (CHF 7'056), then split them 3/5 in VIAC and 2/5 in finpension.**

The finpension promo code below gives you a fee credit of 25 Swiss francs (if you transfer or deposit at least CHF 1'000 within the first 12 months of creating your finpension account).

===> MUSTBC <===