VIAC 3a 2026 referral code

Use promo code "3aMust" when you register on the VIAC app.

You will get free management of your first CHF 2'000 of pension balance in your 3a pension account – and this is valid for life! (And you will also help to support the blog, thanks!)

At the beginning of my FIRE adventure in Switzerland in 2013, there were none of the many fintechs that we see today.

Back then, I even had to go to the canton of Lucerne in order to open a 3rd pillar in the cantonal bank (it was the optimal 3a at that time).

But things have changed a lot since then, fortunately for us Mustachians!

We now have a plethora of fully digital 3rd pillar offerings. And above all, these fintechs offer good private pension products, with the opportunity to invest in index funds and other ETFs, as well as the lowest fees in the market.

Summary: Viac-3a-Review

In summary, here’s my take on whether VIAC’s 3a pillar is worth it, based on my experience—starting with the advantages:

VIAC feedback: What I like about VIAC 3a’s services

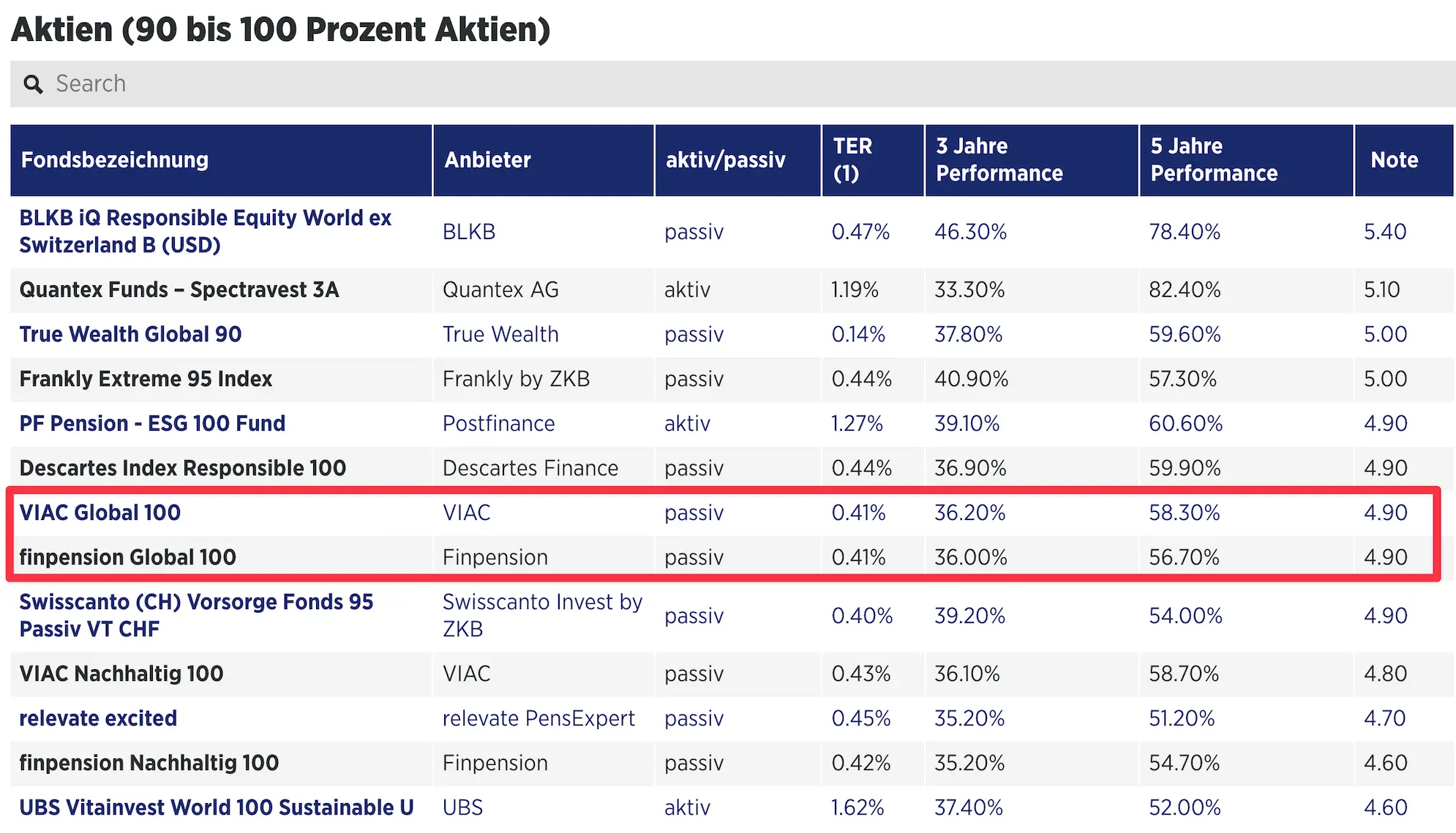

- 1st place ex-aequo (with finpension) with the best return in the Handelszeitung ranking for VIAC (and its “Global 100” strategy). It has held this position for several years in a row. Fees are important (and VIAC is one of the best in this area as well), but what counts in the end is how much you have in your portfolio at the end of the year. And VIAC has so far been unbeatable at this game 💪

- It offers a mortgage solution at a really low rate (in SARON), and above all, which allows you to use your 3a pillar invested in a 100% equities strategy as collateral! This is the Holy Grail (compared to the mixed 3a pillars linked to life assurance, which you are often forced to take out through a traditional bank — and this is a huge rip-off!)

- UPDATE 02.04.2026: due to current market volatility, VIAC currently only takes into account 60% of the valuation of your pledged pillar 3a (compared to 100% previously).

What could VIAC improve in the future?

- Relocate their head office to the canton of Schwyz to be the best in terms of taxation for those who withdraw their 3rd pillar when moving abroad. Because when you draw down from your 3rd pillar in this case, it’s the location of your 3a company’s head office that determines the taxation level on the pension capital vested benefits. As VIAC is in the canton of Basel, this tax is currently a maximum of 10.3%. Whereas if VIAC were to move its head office to the canton of Schwyz (as is the case for finpension), they could benefit from the lowest tax rate in Switzerland at a maximum of 4.8% :)

And… that’s it… VIAC 3a is just THE best private pension funds solution ex-aequo.

MP Recommendation

The 3rd pillar is one of the solutions available for paying less tax in Switzerland.

But Swiss Mustachians go further in terms of tax optimization by following a strategy of opening multiple 3rd pillar accounts to maximize tax savings when drawing down from the 3rd pillar.

This is why I recommend that you open:

- 3x 3a pillars with VIAC

- 2x 3a pillars with finpension

or:

- 3x 3a pillars with finpension

- 2x 3a pillars with VIAC

And every year, transfer 3/5 of the annual maximum 3rd pillar amount to VIAC, and the other 2/5 to finpension (or vice versa).

This is the exact strategy that Mrs. MP and I follow.

Oh, and if you’re new to the blog, I’ll repeat this here: NEVER take out a mixed 3rd pillar linked to (VIAC) life assurance (and if you have made this mistake, like we did once, here is how we managed to cancel it).

As for investment strategy, I recommend VIAC’s “Global 100”. It provides me with optimum diversification (to measure risk as much as possible) for maximum return.

What actually is VIAC 3a?

VIAC 3a is a 3rd-pillar solution.

Are you new to the world of personal finance and asking yourself: “what is a 3rd-pillar?”

In short, a 3rd pillar is like an intelligent piggy bank for your retirement. It enables you to save money each month by benefiting from tax advantages. The money paid into your 3rd pillar is deducted from your taxable income, which means you pay less tax.

But as you are a Mustachian, you don’t want to just pay less tax with your private pension piggy bank.

You also want the money in this piggy bank to grow, like all your other stock market investments.

And to achieve this, you want to choose THE best Swiss fintech that offers the lowest fees in the market. And certainly not one of those big traditional banks that take advantage of you with their fees to pay for Porsches (with their end of-year bonuses!)

That is what VIAC 3a offers you.

Thanks to VIAC 3a, you can choose different investment profiles (and their associated strategies), from the most cautious to the riskiest (as a Mustachian, you will generally be on the “riskiest” side ;)). And through them, your private savings will be invested into ETFs to make them grow over the years.

The aim is to create a nice pot of money for your retirement, by benefiting from tax advantages.

Generally, the next question that comes up is: is viac good and why is the VIAC 3a solution so special compared to competitor solutions?

Why is VIAC 3a THE best 3rd pillar ex-aequo for Mustachians?

Is VIAC good? Yes, my feedback on VIAC would be that it is THE best 3a ex-aequo for any self-respecting Swiss Mustachian. From the VIAC mobile app for opening your account in only 8 minutes and monitoring the performance of your 3a, to the best returns in the market for your investment platform portfolios, VIAC is simply THE best (with finpension).

The Mustachian criteria for choosing your Swiss 3rd pillar

Let’s clarify one thing first: we Mustachians are a special breed ;)

Such a special breed has special selection criteria.

So here is how to judge whether a 3a pillar is the best one or not:

Criteria 1 - “100% global equities” strategy available

We want to be able to invest the maximum 3rd pillar amount in 100% global equities (via ETFs or index funds). Why? To cover the whole world in order to have an optimum risk/return ratio through diversification of the companies in which our money is invested.

That’s why I’m investing my 3a assets in VIAC’s “Global 100” strategy.

Criteria 2 - The best return (fees included)

Over a number of years, I have meticulously compared all fee types under the 3rd pillar in order to choose the best.

But from 2023 onwards, I now only use the Handelszeitung score published at the end of every year to decide my ranking.

Because the cool thing is that the Handelszeitung score considers the final return, including all the fees!

This therefore makes my Mustachian choice much easier. In other words: I want THE 3a pillar with the best return including all fees.

Side note: if you’re wondering why I prefer VIAC and finpension, even though there are other pillar 3a providers ahead of them in the Handelszeitung ranking, take a look at my comparison of the best third pillar in Switzerland for my detailed answer.

Criteria 3 - A 3rd pillar with the security of formal identification

I want to have a secure 3a pillar.

And when I say “secure”, I am thinking specifically about identity verification when I open my account, and not only when I withdraw my funds.

Until 2023, finpension (VIAC’s main competitor) did not offer this option. And I didn’t really like the idea of being able to create a third pillar (invested or as interest bearing accounts) with the name “Donald Duck” and have them approved. Or imagine you make a typo in your first name… then you wouldn’t know there’s a problem until a lot later, when you come to draw down from your 3rd pillar!

So in summary, for me, it means formal identification when opening a 3a account.

Anyway, VIAC Invest has provided this security since the beginning (and finpension corrected this in April 2023).

✅ The VIAC 3a solution fulfills these three criteria. With congratulations from the MP jury for the Handelszeitung score, which rates VIAC 3a in first place ex-aequo, with finpension.

3a VIAC reviews from users

When a financial service that I use has a mobile app, I like to go and check the ratings of their current users.

Because while satisfied customers don’t always comment, unhappy VIAC customers will be the first to post their negative opinion in the most visible manner :)

For me, if a mobile app scores more than 4/5 in the app stores (AND the app has more than 20-40 ratings), that reassures me quite a lot.

So here are the average VIAC app reviews in the iOS and Android app stores:

Not bad at all!

And you can see below a snapshot of some of the VIAC feedback about its 3a:

You can also get an idea yourself through these links to the most recent reviews of the VIAC iOS app and the Android VIAC app depending on your smartphone type.

Alternative solutions to VIAC pillar 3a — and their comparison

VIAC 3a vs finpension

VIAC 3a and finpension 3a are THE best 3rd pillars for a 100% equities strategy, according to the Handelszeitung rating. This ranking is based on end performance, which means after fees have been deducted.

As I explained above, I, personally use an investment strategy that combines VIAC products and finpension 3a. That enables me to diversify my 3a platforms rather than depending totally on one or the other.

To recap, I have chosen to open 3 portfolios with VIAC 3a, and another 2 portfolios with finpension 3a.

VIAC 3a vs neon 3a

VIAC’s third pillar offering is mathematically better than that of neon 3a, when comparing fees, performance, and taxation.

Compared to neon 3a, VIAC’s third pillar offers the following advantages:

- Use of IDF index funds, which are more tax-efficient

- Even more competitive fees from the very first Swiss franc deposited

- Option of a personalized strategy

VIAC 3a vs frankly

The result for frankly 3a is good (this year for the first time), but I prefer to have a fund invested as much as possible in equities (99%) over the long term for my pillar 3a. I therefore prefer VIAC 3a and its 99% equities (stock market investments), because fewer equities = lower performance.

VIAC 3a vs True Wealth

True Wealth was the last to arrive on the market of 3rd pillar solutions that are invested in the stock market. It made quite an entrance as True Wealth decided to offer a 3a without any management fees. A first in Switzerland!

However, I prefer the VIAC 3a offer, which I believe is better in the long term, because despite True Wealth’s good score, only 90% of your cash is invested in stocks (and the remaining 10% is in REITs, which is too much real estate for me), and I require a minimum of 99%.

Also, True Wealth’s 3a pension foundation states in its cost regulations that the foundation’s board of trustees reevaluates every year whether to reintroduce management fees of 0.225% per year on the securities portion. This is another reason why I prefer VIAC 3a (or finpension 3a), which has a more permanent fees strategy.

VIAC 3a vs Descartes (formerly Descartes Vorsorge or Descartes Prévoyance)

No. VIAC 3a is generally better.

Even though Descartes scores well in Handelszeitung, this score mainly relates to the “Descartes Index Responsible 100” strategy. When comparing the factsheets, VIAC 3a offers greater diversification, while Descartes 3rd pillar remains more concentrated (due to ESG exclusion criteria). For a long-term third pillar, I therefore prefer VIAC 3a for its superior diversification.

finpension 3a vs Selma

The VIAC 3rd pillar performs better than Selma for a Swiss investor who wants to invest their money 100% in equities. Basically, VIAC allows you to invest 99% in equities, while Selma only allows a maximum of 97% with its 3a pillar. Fewer equities mean lower returns.

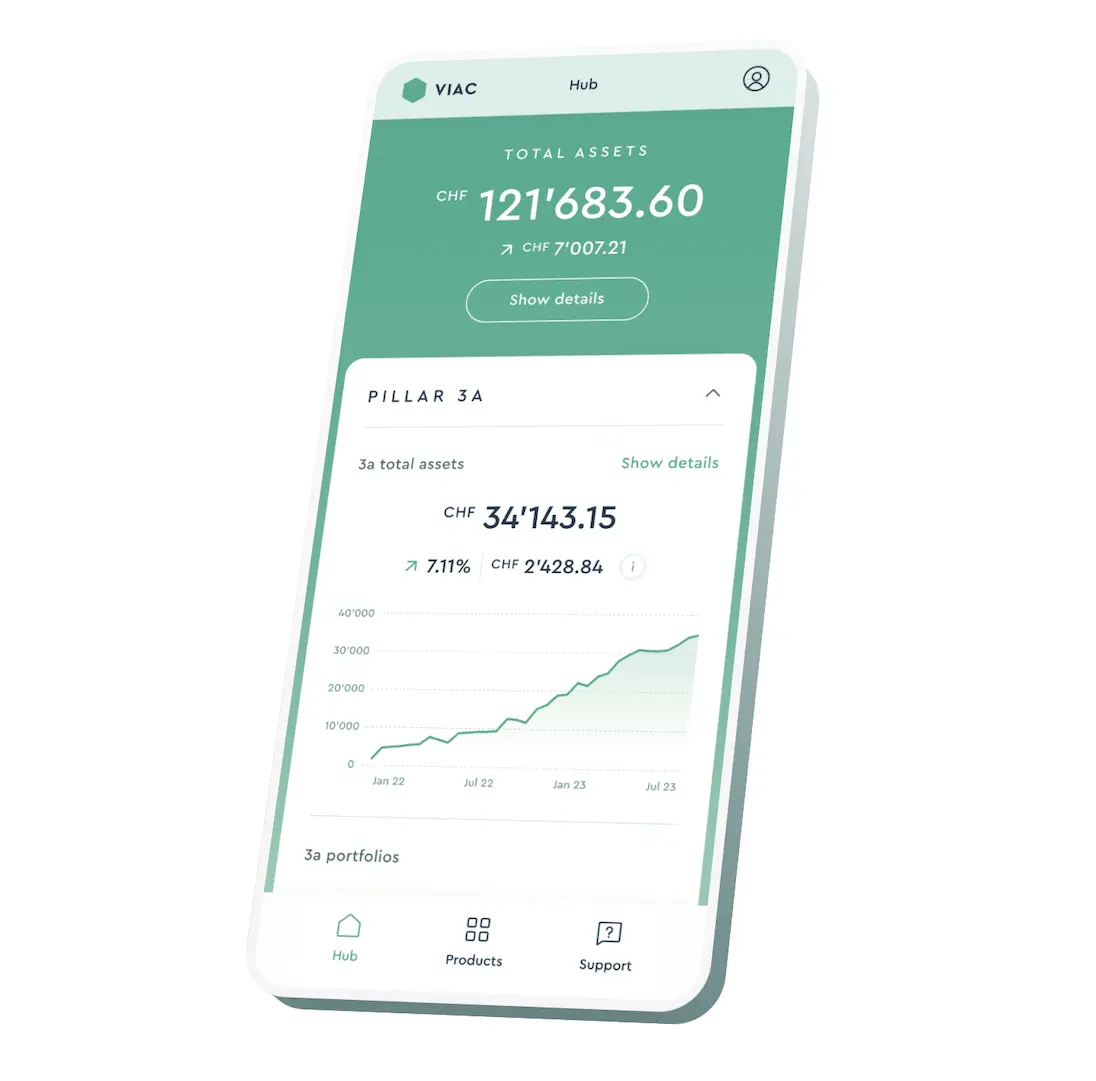

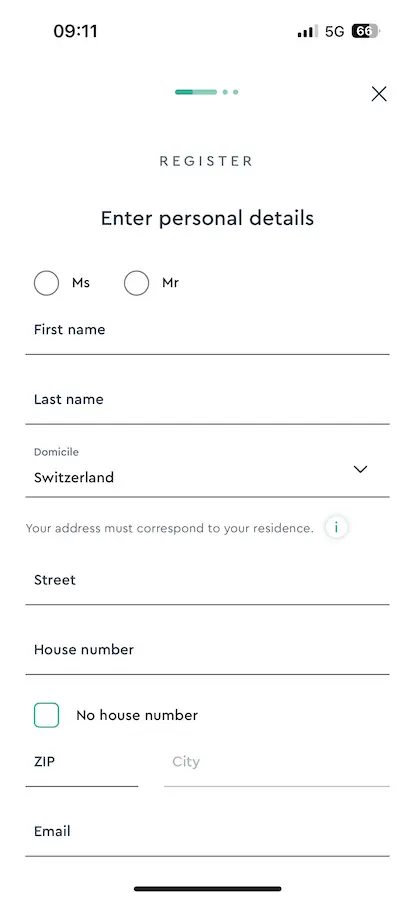

How to open a VIAC account in 8 minutes

I was blown away by the speed of opening an account when I registered on VIAC for the first time and it took just a few minutes.

After an opening process of literally 8 minutes (VIAC used to promote this), I had a new 3rd pillar.

Whereas back then, I remember that you had to schedule an appointment at the bank and spend ages there signing I don’t know how many forms…

Or worse, you could get conned by a fraudulent adviser trying to flog you their 3rd pillar linked to a life assurance policy (REMEMBER: NEVER SIGN UP TO SUCH A SOLUTION!!!)

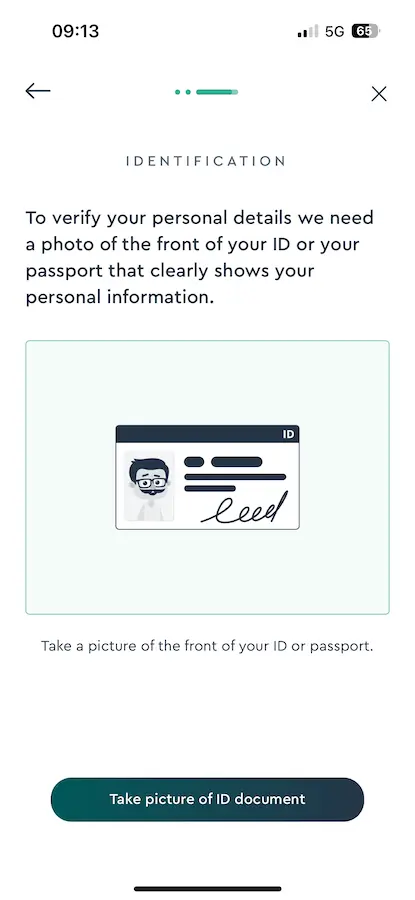

Below, you will find screenshots of the registration process for the VIAC 3rd pillar. You can do this through the VIAC mobile app or web app.

There are 4 main steps to follow for you to open your VIAC account:

- Download the VIAC app (iOS AppStore, Android Google Play Store) on your smartphone, or go onto their web app

- Create your profile by answering 6 simple questions to define your risk profile, and get the investment strategy that is appropriate for you

- Open your VIAC 3a pillar

- Confirm your identity to formally verify who you are

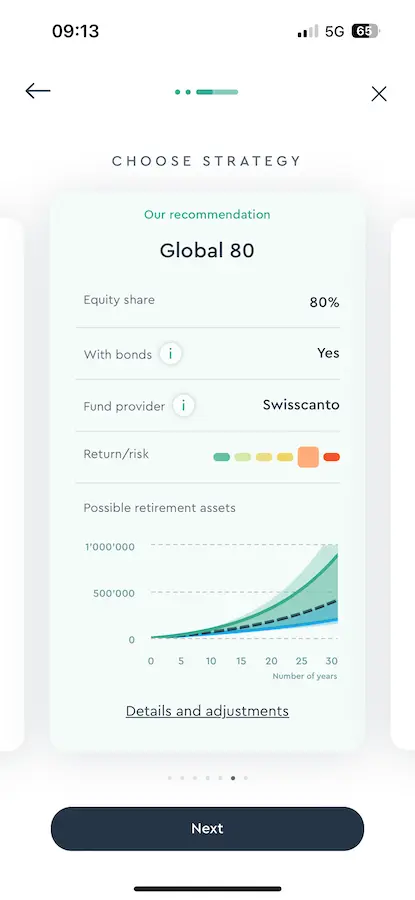

VIAC proposes an investment strategy based on your answers to the previous questions (for myself, I choose 'Global 100' to be 100% in equities and maximize my returns)

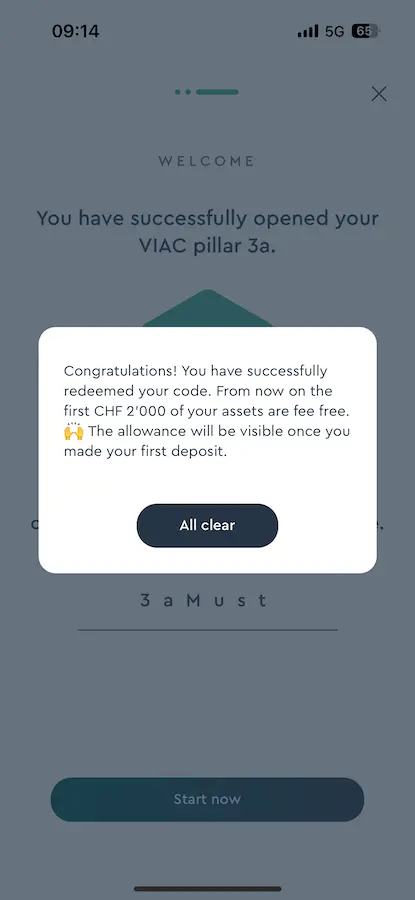

Once you’ve created your 3a VIAC account, simply enter my VIAC 2026 referral code (’3aMust’) to get free management of your first CHF 2'000 of private pension assets (valid for life):

Use the Mustachian Post promo code ('3aMust') to get free management of your first CHF 2'000 in pension assets

And that’s all :)

All that remains is to make your first payment into your VIAC 3a account to make tax savings!

FAQ about VIAC 3a

Who created the VIAC company?

The company VIAC AG was established in September 2017 by Daniel Peter, Jonas Gusset and Christian Mathis. The three co-founders all come from the banking sector. I like the fact that they started from their own challenge: having a 3a pillar they could trust and which they could recommend to their friends.

Where is VIAC AG’s head office located?

VIAC AG is registered in the Basel Companies Register.

Why only 99% and not 100% equities with VIAC 3a?

I asked myself the same question as you when I first came across VIAC… the answer is simple: VIAC has to keep 1% of your investments in cash in order to take their fees. Even though they are very low, they can’t take their fees from your money, which is invested in ETFs.

Can I leave cash sitting in VIAC 3a without investing it?

Yes. You just need to open a VIAC 3a pillar and choose the “Compte 3a” investment strategy. See it as a 3a savings account where your money will not be invested in the stock market.

How much should I put aside each year into my 3rd pillar?

As a Swiss Mustachian, your objective is to fill your 3rd pillar to the maximum legal amount in 2026: this is CHF 7'258 per year.

The goal is to take full advantage of all available tax deductions.

Then, once these savings have been invested in your VIAC 3rd pillar, you invest all your remaining money in the stock market.

Do you recommend Swisscanto or UBS as a fund provider (for the Global 100 strategy)?

I chose Swisscanto funds for two reasons:

- Swisscanto is 0.01% cheaper than UBS

- I prefer the philosophy of ZKB (behind Swisscanto) to that of UBS

But overall, Swisscanto and UBS funds are almost identical for VIAC’s Global 100 strategy.

VIAC Review Conclusion

VIAC is THE best 3rd pillar ex-aequo (with finpension). For us Swiss Mustachians in any case.

To diversify (and also test for you, dear reader!) my 3a funds, I decided to split my private pension provision investments 3/5 with VIAC (VIAC is not just good, but the best), and 2/5 with finpension (the second best 3a pillar).

At both VIAC and finpension, I have chosen an investment in the strategy with the maximum number of equities. These are “Global 100” at VIAC, and “Equity 100” at finpension.

Knowing that Mrs. MP and I need to put CHF 3'700 each into our VIAC 3a account for our mortgage (VIAC as well!), that makes a good split.

And my recommendation is the same for you, dear reader: invest your savings in your 3rd pillar at an amount of CHF 7'258 (maximum 3rd pillar amount in 2026), by putting CHF 4'233.60 into VIAC (= 3/5), and CHF 2'822.40 into finpension (= 2/5) — or vice versa.

The VIAC promo code below entitles you to free management of your first CHF 2'000 of pension balance in your VIAC 3a pension account – and it's valid for life!

===> 3aMust <===