Since we started to invest again on the stock market two years ago, our modus operandi is worthy of the auto-pilot of a Tesla (no, no, I still haven’t succumbed!): we save 40% of our monthly income, and every quarter we invest all of this in ETFs via Interactive Brokers in ETFs.

“But which ETFs do you choose in 2018, MP? “, I can already hear you asking.

My usual answer until then was to redirect you to the page of my ETF portfolio.

But which ETFs do you choose in 2018, MP?

Except that, as the assiduous people have pointed out to me, this page listing the ETFs in which I invest starts to be outdated. My last update being from…2016. So it was time to fix it.

My Mustachian portfolio of ETFs in 2018

Just a reminder for new readers: I’ve a certain obsession with simplifying my task when it comes to our investments. That is, the less time I spend on my e-banking and my online brokerage platform, the better I am.

The best way I’ve found so far to satisfy this need for efficiency is to build a Bogleheads’ portfolio, composed of only 3 ETFs.

If you want to know more, go read this article which is still valid today.

To make it short, this is my allocation as of today:

- 68% of ETFs in shares, of which :

- 55% are international equity ETFs

- 13% are Swiss equities ETFs

- 32% of ETFs in bonds

Concerning the ETFs themselves, here is where I’m at with my choices:

ETF in international equities

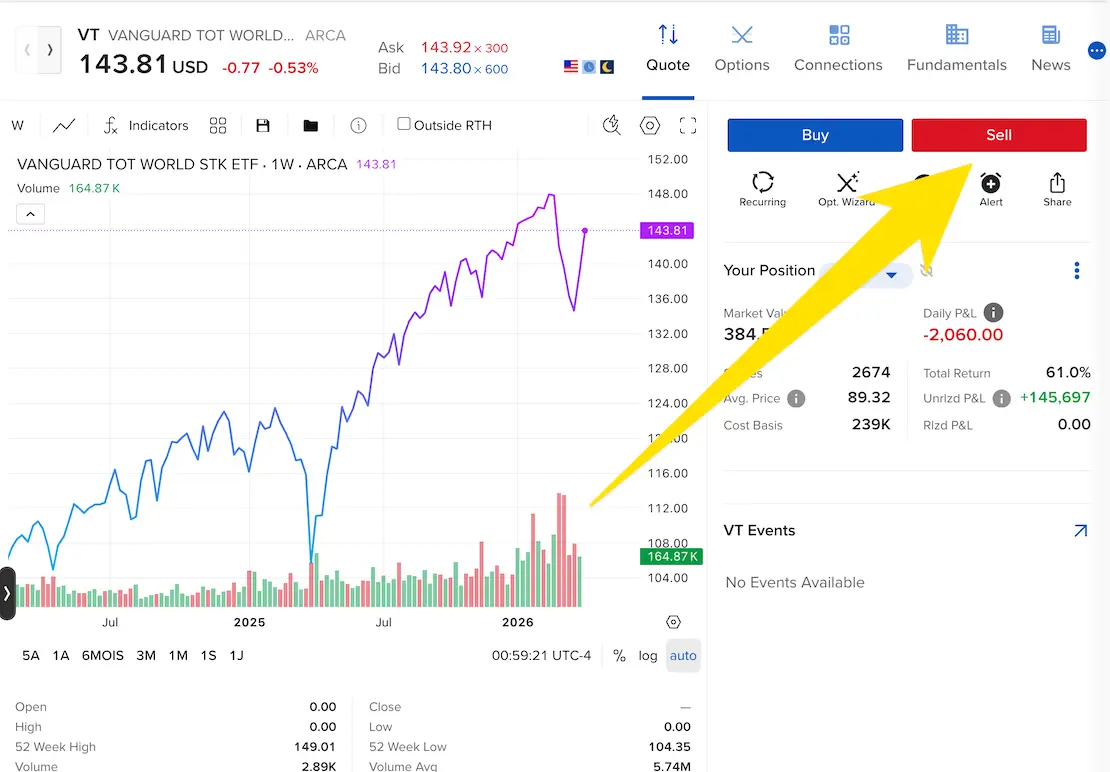

I have invested up to 60kCHF in the famous VT ETF from Vanguard.

Why 60kCHF? Quite simply because I still haven’t managed to get a 100% official answer regarding the estate law in the US which potentially taxes you at a 40% rate at your death on assets exceeding 60kCHF invested in this country. There is a US-Switzerland treaty which, after several (re)readings, is still incomprehensible (if you, dear reader, are a lawyer, don’t hesitate to enlighten us!). Even the tax department of the canton of Vaud couldn’t answer me (or maybe they didn’t understand the question…)

Since I passed this milestone, I now invest in the Vanguard FTSE All-World UCITS ETF (aka VWRL, as I buy the CHF version on the SIX market).

UPDATE 17.05.2020

It’s now clarified. The US-Swiss estate tax treaty covers our case. All information in this dedicated article.

ETF in Swiss shares

Until now, the allocation of my portfolio has always been too low in international equities, compared to the Swiss equities I own via our 3rd pillars, my international VT ETF (which contains its share of Swissness), and shares of my company.

As a result, we never bought this UBS ETF (CH) SMIM (CHF) A-dis. But to date, it remains my Swiss ETF of choice when compared to the competition with this research on JustETF.com (read my article on building a Bogleheads portfolio to find out how I got to these filters), as well as this performance comparison over the last years. When I see its yield history, I look forward to buying it by the end of the year/beginning of next year.

ETF in Swiss bonds

My most changing recommendation (compared to 2016) is the one about bonds.

As a reminder, the purpose of bonds in a Bogleheads portfolio with 3 funds is above all to reduce the volatility of it, i.e. to provide security for your investments in the event of major disruptions on the equity market. It’s therefore not the yield that interests us here (although we’ll never refuse it either:)).

As a result, I did focused my research on JustETF.com on the CHF currency at the time, again to not add volatility by taking a bond ETF in another currency (because who says another currency, says increased volatility due to the exchange rates).

I therefore told you that I had chosen the iShares Swiss Domestic Government Bond 3-7 (CH) ETF for my portfolio.

Two considerations have evolved in my thinking process since this announcement:

- 1/ Until now, I’ve never had to buy this ETF because my bond allocation takes into account my 2nd and 3rd pillars, as well as my emergency cash cushion. Looking at the evolution of my overall allocation, I realized that I wasn’t going to invest in such a bond ETF any time soon.

- 2/ For several years, bond ETFs denominated in CHF have had negative interest rates, which means that you pay/lose money by investing in them. Nevertheless, since the goal is security vs. performance with this type of fund, this point could be ignored. Except that there is an alternative: cash. Equally secure for your portfolio, since it belongs to you and is unlikely to fluctuate - unless you spend it of course…. But cash isn’t protected against inflation. Nevertheless, it is always better than seeing your savings decrease in a bond ETF with negative interest rates.

My recommendation is therefore as follows nowadays: if, like me, your allocation in bonds (including your 2nd and 3rd pillars, and excluding what is invested in equities with platforms such as VIAC.ch, as well as your safety cushion) is already too important compared to your ideal allocation, then don’t waste your time looking for a bond ETF in CHF, because you’re not going to buy it in the end.

On the other hand, if today I’d need to buy bonds, what I’d do would be to keep my cash in the bank wisely until the interest rates on bonds start to rise above 0% again. And only once this course would’ve passed, then I’d spend time choosing my bond ETF.

Summary

My Bogleheads portfolio for 2018 therefore looks like:

- International equities ETFs:

- Swiss equities ETFs:

- I take into account all the Swiss equities that we have via the VT ETF and the VWRL one

- There are also the Swiss shares we own through our 3a pillars

- The shares of my company

- As soon as I’ll be able to (i.e. compared to my ideal allocation), I’ll buy the UBS ETF (CH) SMIM (CHF) A-dis

- Bonds ETFs:

- I consider the money of my 2nd and 3rd pillars as bonds

- The day I’ll need to buy back some for my allocation to be perfect, I’ll keep cash if interest rates are negative, or else I’ll start looking for a Swiss bonds ETF (as this will happen only in several years, I didn’t bother to check it today)

In any case, I’d like to thank our reader Max for reminding me that I’d’nt updated my ETF portfolio page for a long time. This has now been done :)

So I’m going back to auto-pilot mode until the next big change, which I’ll certainly share with you.

What’s your ETF portfolio in 2018? What about the allocation?

Joint budget for couples: managing money at the …

Shared budget for couples: how to get your partner...

Last updated: September 9, 2018