If you are browsing this site, you are probably looking to invest in the stock market to achieve financial independence in Switzerland.

And if you want to invest in the stock market, you will have to choose which trading platform you are going to use.

I went through this back in 2013…

Does trading in Switzerland mean you must use a Swiss broker? (Nope!)

I made the same mistake as many beginner investors in Switzerland: I chose the online trading platform Swissquote because it was the Swiss broker that everyone around me was talking about.

“Swissquote or BCV? Oh, let’s use Swissquote because they are cheaper.”

“Swissquote or UBS? Nah, I heard from my cousin that Swissquote is cheaper.”

After conducting my own research, I also came to the conclusion that Swissquote was the best solution for a Swiss investor.

Because for me, it was impossible to choose another trading platform instead of a Swiss company to invest in the stock market in Switzerland… (and yes, I was that naive!)

Me in 2013 who thought the best trading platform in Switzerland was Swissquote (and that you only had access to the SIX Swiss Exchange)

Then I learned that you can actually buy any stock on the stock market through different brokers. As long as that online broker allows customers who are Swiss residents.

And that opened up a new realm of possibilities for me.

Almost too many possibilities even… because any trading platform in the world can be a potential candidate… knowing that there are more than twenty online trading platforms in Switzerland with trading fees ranging from CHF 100/year to CHF 2'000/year!

Therefore, I wrote this article to introduce you to the best trading platform for a Mustachian Swiss investor.

What type of investor is this article written for?

Before I start with my trading platform comparison, we need to clarify the aim of this article.

You may read on if you are going to invest like a Swiss Mustachian:

- Investment strategy “Buy and hold”

- Investment portfolio consisting of 3 ETFs using the Bogleheads method

- Investing your savings once per quarter, every time in a single ETF to avoid additional transaction costs

Mustachian investment strategy: invest passively within 15 minutes per quarter, and hike in the Franches-Montagnes the rest of the time :)

If this doesn’t fit your investment strategy (e.g., if you are a day trader or you invest in other asset classes), then don’t waste your time reading further, since this article won’t fit your case.

For the rest of us, let’s look at the relevant criteria I use to establish my comparison of the best trading platform in Switzerland - and I’ll also present you with the other, more futile criteria.

What are the important criteria for choosing the best trading platform?

There are four important criteria for choosing the best online broker: the lowest fees, access to the best ETFs, the solidity (financial and governance) behind the trading platform, and finally, the availability of an IBAN in CHF.

Criterion 1: Trading costs

Online brokerage account maintenance fees, inactivity fees, custody fees, and forex trading/currency exchange fees are administrative fees.

Since the digitalisation of trading, these account fees are “fictitious” and actually represent “easy” money for financial institutions.

Swiss online brokers (including our dear banks…) like to take advantage of such fees.

Except that for an investor, with 1% deducted here and 1% there, your fortune is likely to melt like snow in the sun as time goes by.

But luckily for us, competition is starting to show in Helvetia, and it’s to our benefit.

Transaction fees, as the name suggests, are the fees you pay when you buy or sell a stock.

The “real” online brokers do their business mainly via these fees.

They offer you brilliant service and know that by being the best on the market, they will attract a lot of capital.

And so they will start making substantial money for that reason, vs. charging you fees to generate cash in the short term, thus losing you in the long term because it’s not in line with your frugal style.

To speak with concrete numbers, here is what I am aiming for in terms of fees:

- Account maintenance fee: CHF 0

- Inactivity fee: CHF 0

- Custody fee: CHF 0

- Transaction fees: less than CHF 1 per transaction

- ETF transaction fees: ideally free of charge via a list with the best ETFs in the market

- Currency exchange fees: lowest possible

- Minimum amount to open an online trading platform: none

Any Swiss investor who buys securities on the stock market is charged an additional tax called "stamp duty" (between 0.075% and 0.15% of your transaction amount). Well, that's not entirely true: it's any Swiss investor using a Swiss broker must pay stamp duty. But if you use a foreign (i.e., non-Swiss) broker, then you are excluded from this stamp duty. This stamp duty optimisation technique allows you to save even more on your brokerage fees. Here you can find all the detailed information on this subject in this dedicated article.

Criterion 2: Financial and governance strength of your broker

As you venture down the FIRE path to financial independence, you’ll start saving and investing money.

A lot of money.

Several hundred thousand CHF.

And the last thing you want is for those savings to vanish.

Fortunately, there are deposit protections in every country, but if you don’t mind having your money frozen while you wait for bankruptcy proceedings, that’s just as bad!

That’s why one of the 4 important criteria to look for when choosing an online trading platform is to make sure that the company behind it is rock solid, both financially and in terms of governance.

One of the most important signals is to look at how long the company has been in business and to search the web for any bad reviews or ratings.

Criterion 3: Trading platform with an IBAN securities account in CHF

At first, the small percentage fees may seem minimal when you are investing with “only” 1'000 Swiss francs.

Like: “Yeah, well MP, don’t exaggerate, we’re talking about 1.5% currency conversion fees… on CHF 1'000, that’s only CHF 15”

Except that, as I often tell you on the blog, CHF 1,000 in savings is just the beginning.

Because with the frugalist strategy you’re going to use, you’ll soon find yourself with 5-figure sums to invest in the stock market.

So for CHF 10'000, you’ll have to waste CHF 150 in fees.

And personally, I don’t know about you, but I have other things to do with 150 Swiss francs than give them to an online broker voluntarily!

So the criterion for this chapter: choose an online broker that offers you an IBAN account in CHF so that you can send your savings directly from your Swiss bank account.

This way, you can transfer your savings without having to spend money on currency exchange fees. Afterward, if you decide to buy an ETF in USD, you can do the conversion (with the lowest fees, as mentioned in point 1 above).

Criterion 4: access to the best ETFs

Still, in this “buy-and-hold” long-term investment perspective, the second important criterion is to have access to the best ETFs.

What is a “best ETF”?

It is an ETF with low fees (the famous TER for “Total Expense Ratio”) and is well diversified to mitigate the risks of loss linked to a particular industry or country.

We’ll talk about this below, but some ETFs are only available through certain online brokers due to financial regulations.

What criteria are NOT AT ALL or NOT very important when choosing your trading platform?

There are certainly more than the two below.

But these two criteria I mentioned are often why some people decide between this or that broker.

It often involves extra costs with many online brokers, which you could avoid if you wanted to.

Because you will only use your online broker once a quarter to buy an ETF!

Pointless criterion 1: complex set of analysis tools

I remember those movies from the 90s where the active traders were speculating on their five big screens side by side.

They appeared so smart and classy in their Wall Street suits.

They were looking at dashboards full of complex charts using stock picking algorithms to buy and sell stocks at the speed of light.

Fortunately, you don’t need these fancy tools to make your money work for you.

What’s “smart and classy” these days is an investment strategy that keeps you away from your online trading platform as much as possible.

Four times a year, you’ll spend thirty minutes buying new ETFs.

And once a year, you’ll rebalance your portfolio.

That’s it.

You have better things to do with your time.

And your investment portfolio will thank you for it when you don’t sell everything because of a panic attack during a sudden market downturn.

So, no, there is no need for complex stock market analysis tools.

Pointless criterion 2: an ultra mega easy-to-use user interface

As much as I like well-designed user interfaces and free demo accounts for the services I often use, I don’t take this criterion into account when evaluating an online broker.

Why?

Because I will only use it for 15 minutes per quarter!

So the only thing I need is for the broker should be as cheap as possible.

And to be functional. Four times a year :)

Plus, even if it’s not on our list of needs, we’re lucky these days that all these platforms have a good website and a mobile application most of the time.

Trading platform usage scenarios: from beginner to veteran

I wanted my broker comparison to apply to beginners as well as to veterans who have been investing for decades.

Therefore, my brokerage fee simulations to find the best broker are based on the 6 scenarios below.

First, let me introduce you to the two protagonists: Adrian and Melanie.

Adrian, Swiss, 22 years old, works in IT

Adrian is a 22 year old frugalist. He has completed his IT apprenticeship and is looking to move up the ladder to properly increase his salary.

Luckily, he came across a cool blog about financial independence and how to retire early at 40 :D

During the first few years of his career, Adrian will go through the following scenarios:

| Adrian’s scenarios | Starting amount | 1x investment per quarter |

|---|---|---|

| 1 | CHF 10'000 | CHF 1'000 |

| 2 | CHF 30'000 | CHF 3'000 |

| 3 | CHF 60'000 | CHF 6'000 |

Melanie, Swiss, 35 years old, product development manager in a pharmaceutical company

Melanie, meanwhile, is already well on her way to financial independence. She plans to be FIRE around her 43rd birthday.

Her biggest dream is to spend 6 months in Japan, in a small town she visited (where she could only stay a few days on holiday because… well, she had to go back to work in Switzerland…)

Here are her investment scenarios:

| Melanie’s scenarios | Starting amount | 1x investment per quarter |

|---|---|---|

| 1 | CHF 110'000 | CHF 10'000 |

| 2 | CHF 200'000 | CHF 15'000 |

| 3 | CHF 300'000 | CHF 20'000 |

We will use these 6 scenarios later to compare brokerage fees.

Candidates for the Best Online Broker in 2026 (for Swiss investors)

After hours of research and compilation of brokerage fees, here are the candidates for my ranking of the best online brokers:

- Interactive Brokers

- DEGIRO

- Saxo Bank

- Cornèrtrader

- Charles Schwab

- Swissquote

The logos of these trading platforms look like this:

If you don’t see the trading platform you are looking for, take a look at the FAQ. You should find your answer there. And if you don’t, email me because maybe I’m the one who overlooked the broker.

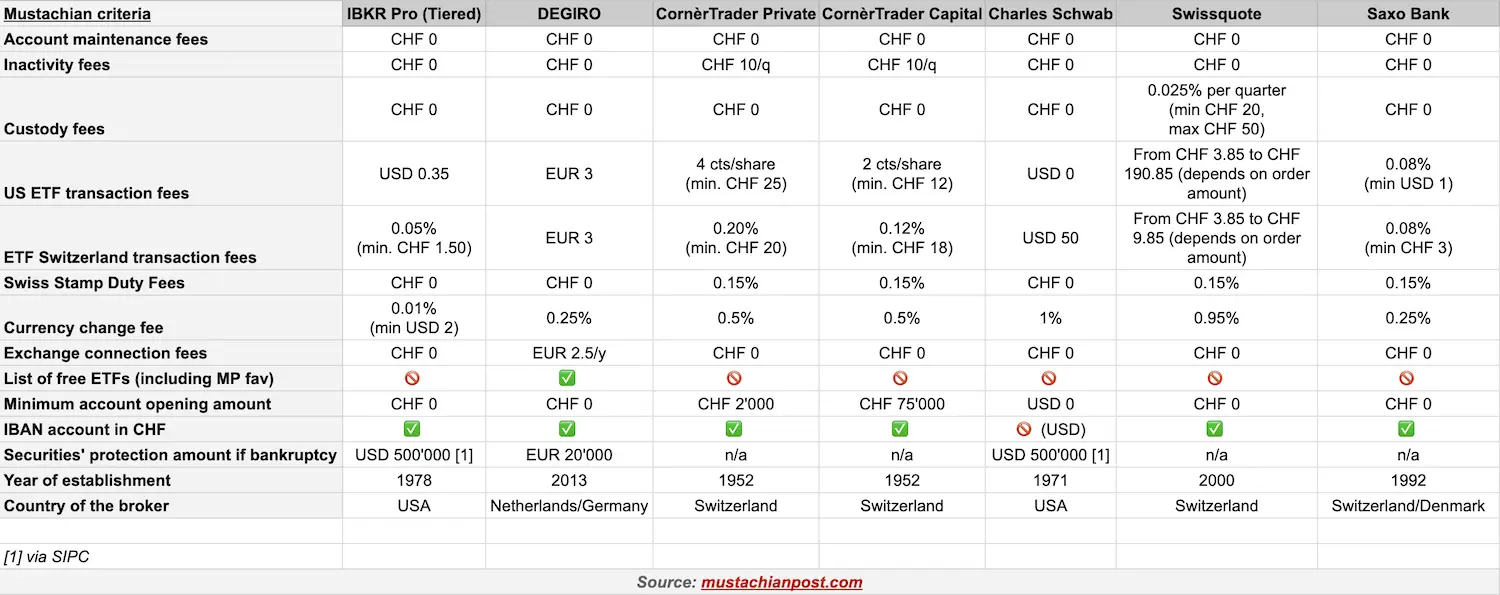

Brokerage fees comparison of the best trading platforms (+ broker financial strength + IBAN account in CHF)

I spent several hours researching the following information for all trading platforms:

- What are the account maintenance fees?

- What are the inactivity fees?

- What are the custody fees?

- What are the transaction fees to buy a US ETF?

- What are the transaction fees to buy a Swiss ETF?

- What are the stamp duty charges?

- What are the currency change fees?

- What are the exchange connection fees?

- Does the broker offer a list of free ETFs (i.e., free of transaction fees)?

- What is the minimum amount required to open a trading account?

- Does the trading platform offer a securities account with an IBAN in CHF?

- What is the amount of protection for my assets in case of bankruptcy of the broker?

- What year was the company behind the trading platform founded?

- In which country is the company behind the trading platform located?

And I’ve consolidated and summarised all this for you in this useful table:

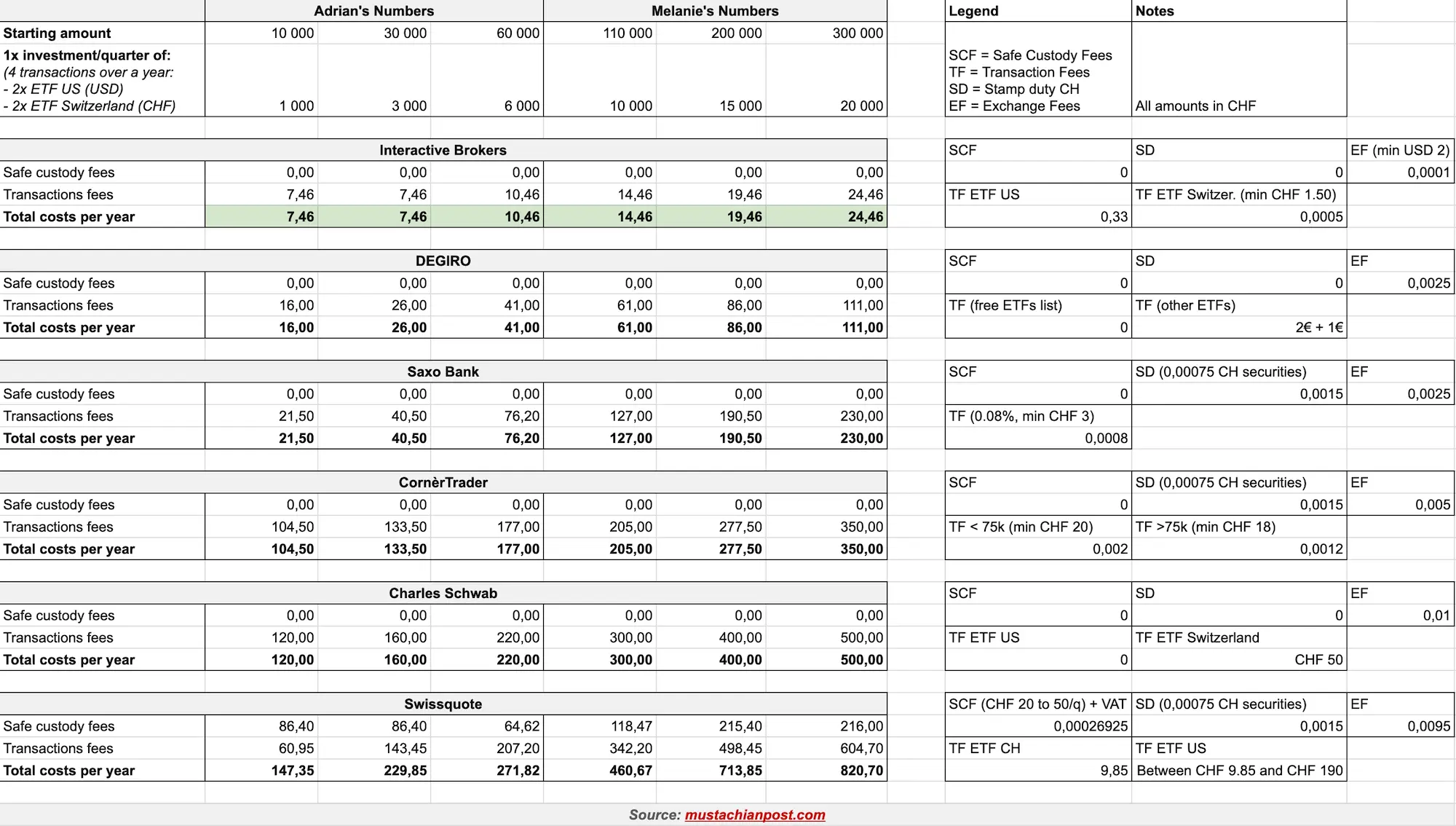

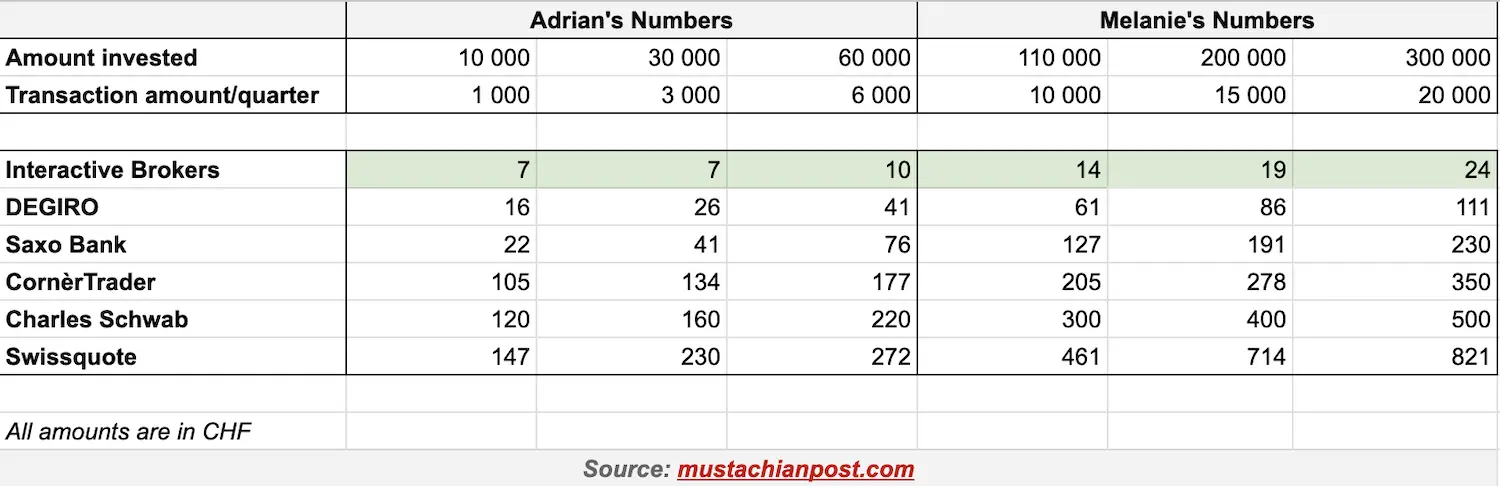

Now, let’s run the simulation with each of Adrian’s and Melanie’s 3 stock market investment scenarios.

Here is the result of their brokerage fees in great detail:

And to make it easier for you to read (for me too ^^), here’s what it looks like in a summary table of trading platform fees:

Comparison of the available ETFs for each trading platform

My selection of ETFs to achieve financial independence in Switzerland is simple; it follows a 3-fund Bogleheads strategy: 1 global stock ETF, 1 Swiss stock ETF, and 1 Swiss bond ETF.

Until this day, I never had to choose a Swiss bond ETF, since my 2nd pillar money covers this role with a slightly safer investment than bonds.

For the other two ETFs, here are my choices:

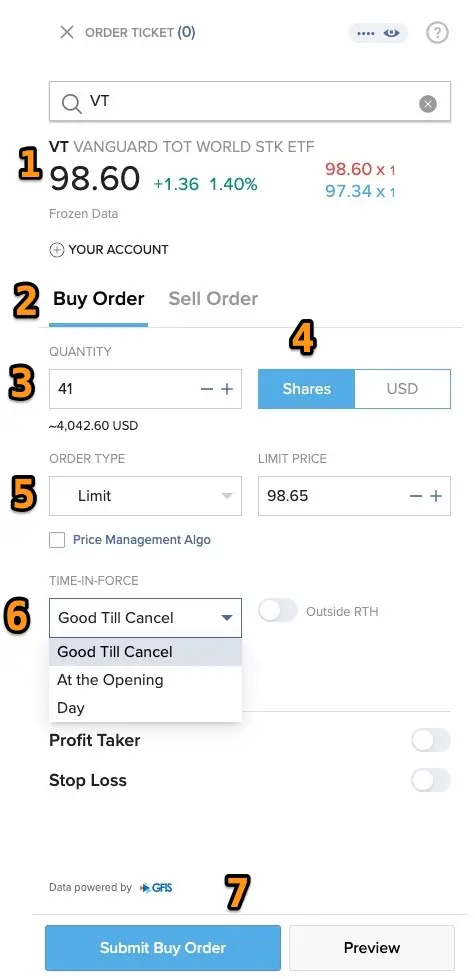

- The VT ETF for global stocks (ISIN = US9220427424)

- UBS SMIM ETF for Swiss stocks (ISIN = CH0111762537)

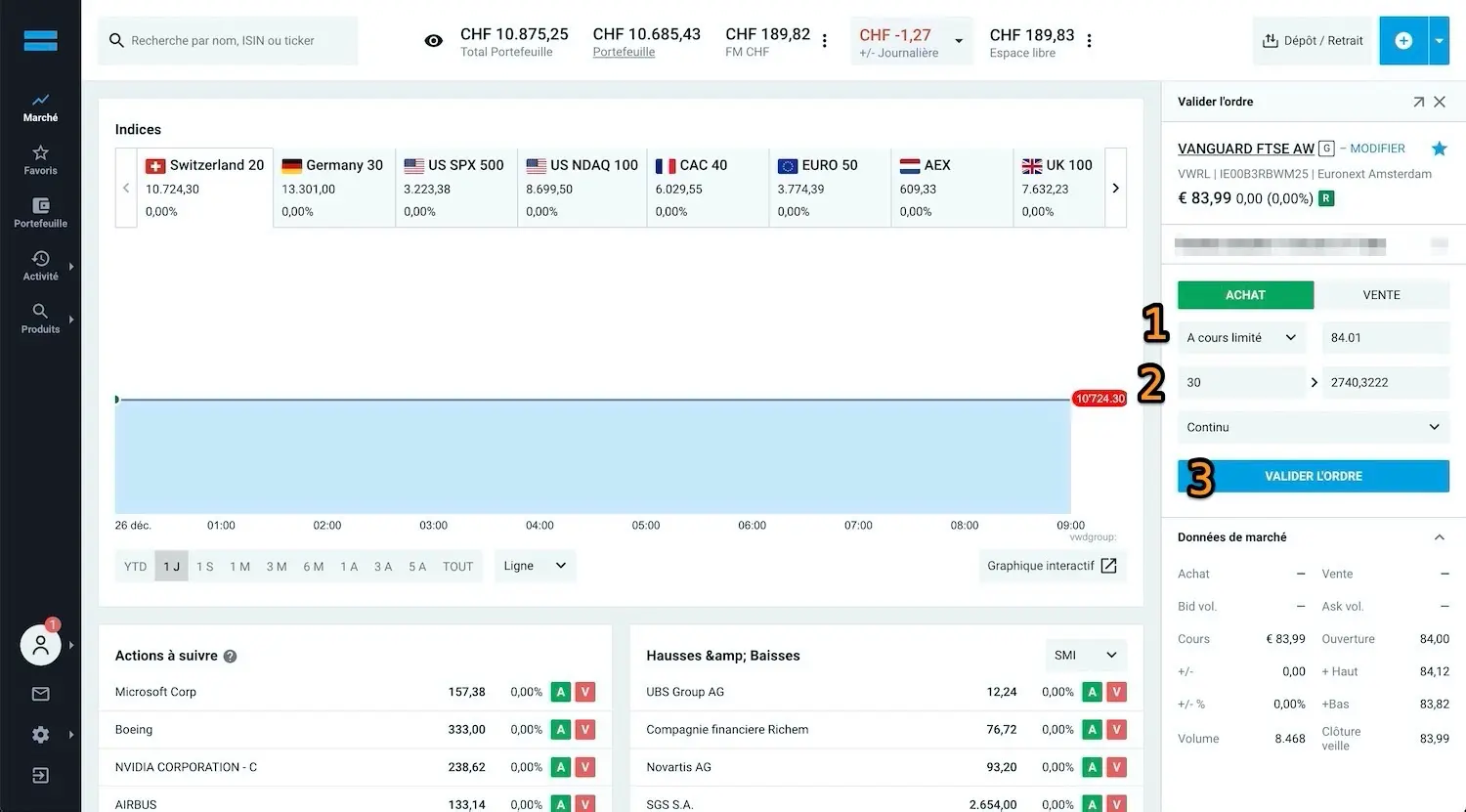

Some brokers no longer offer the VT ETF due to financial regulation history reasons. The second-best global equity ETF in this case is the VWRL ETF (ISIN = IE00B3RBWM25).

You can find all the contents of my ETF investment portfolio on this dedicated page.

The VT ETF is therefore only available via the following trading platforms: Interactive Brokers (*), Charles Schwab, Saxo Bank, and Swissquote.

These are the four best ETF-selection trading platforms - Interactive Brokers, Charles Schwab, Saxo Bank, and Swissquote - They are the best due to the wide selection of ETFs they offer.

And so: Cornèrtrader and DEGIRO (**) are less interesting for us Swiss Mustachian investors since these platforms do not offer US ETFs.

Which trading platform should you use in Switzerland: My Top 3 in 2026

The result is obvious: Interactive Brokers remains THE most advantageous online broker in all aspects for a Swiss Mustachian investor.

And the runner ups are DEGIRO (ranked second, if you want a European broker), and then there is Saxo Bank (ranked third, if you absolutely want a broker based in Switzerland).

Ranks of the three top brokers for a Swiss investor

N.B. if you choose to open an account with Saxo Bank via this link, you will be entitled to a refund of CHF 200 of brokerage fees during your first 3 months with them, applied within 24 hours of the initial funding (Saxo Bank offer conditions are detailed here, and the blog will get a bonus too — thanks to you for that).

Interactive Brokers Tutorial (for Swiss investors)

Starting to invest in the stock market is a challenge.

I went through it myself in 2013, just when I started my FIRE adventure in Switzerland.

That’s why I created a complete tutorial (account creation, ETF purchase, currency conversion, etc) for my favorite online broker, Interactive Brokers:

Complete Guide for Interactive Brokers 2026 >

DEGIRO tutorial (for Swiss investors)

Of course, I also created a detailed guide for DEGIRO just for you.

I’ve been using this trading platform for a long time to buy the ETFs that make up the investment portfolio for our two MP children (we have now switched to IBKR for them too).

Complete guide for DEGIRO 2026 >

Saxo Bank tutorial (for Swiss investors)

Saxo Bank completely overhauled its strategy in 2024 and 2025 and permanently lowered its trading fees. So I’ve taken the time to do a proper guide:

Complete guide for Saxo Bank 2026 >

Conclusion

To the question “What is the best trading platform?”, I always respond without hesitation that Interactive Brokers (*) is the best online brokerage account for a Swiss investor. I have been using this online trading broker since 2016, and I continue to recommend it to everyone I know (including you, who is reading this blog).

If you have a major issue with having a US-based broker, then the next best broker for Swiss investors would be DEGIRO (*) (**), which is based in Europe.

Finally, if you absolutely need a Swiss trading platform, then I recommend using Saxo Bank (*) (<= CHF 200 brokerage fee will be refunded to you by using this link, applied within 24 hours of the initial funding).

And you, do you invest in the stock market? If yes, which brokerage platform do you use?

FAQ trading platform in Switzerland

How can you start online stock trading in Switzerland?

I don’t really like the word trading because it implies constant daily transactions. I prefer to call it “investing for the long term” or Bogleheads investing or even investing like a Mustachian.

For the sake of completeness, I recommend these two links if you want to get into the Swiss stock market:

- How would I invest CHF 10'000 in the stock market if I were to start today (stock market crash or not!)

- How to invest in the Swiss stock market as a beginner (paid program, 100% Swiss)

What type of trading is the most profitable?

If you don’t want to go crazy and have to spend every minute of your life in front of a screen, then the long-term “buy and hold” method is the most profitable in my opinion.

I would recommend reading this article in detail on how I invest in the stock market in just 30 minutes per quarter (and sleep soundly!!)

What is the most reliable trading platform?

According to my research, Interactive Brokers is the most reliable online brokerage platform to date. On the one hand because the parent company has been around since 1978 (!), and has therefore successfully survived several decades of stock market crashes and various other crises. And on the other hand because they go all out in terms of security (mobile app with double authentication and via their due diligence process imposed by the American financial regulations).

Finally, one of the other elements that speaks for the reliability of a broker: Thomas Peterffy, the founder of Interactive Brokers (cf. my video interview with him in person!), is still the CEO and visionary who has been leading the company for over 45 years!

What is the best trading platform for beginners in Switzerland?

If I can convince you that DIY investing is much simpler than it sounds, then Interactive Brokers is the best broker to start investing in the Swiss stock market.

Even simpler with their GlobalTrader mobile app, specifically developed for beginners.

If, on the other hand, you are too scared of the stock market, then I would recommend you check out a Swiss robo-advisor such as finpension Invest, which guides you step by step and uses good quality ETFs to start investing.

Neon Invest or Interactive Brokers, which is better?

Neon Invest is not suited for us, the target audience of the MP blog, who want to optimize our brokerage fees with our tens or even hundreds of thousands of USD invested in the stock market. Indeed, buying CHF 2'000 of US ETFs costs USD 0.35 on IBKR, whereas it costs CHF 10 with neon invest (= 0.5% of the transaction amount).

And then there’s the stamp duty (on each transaction) to which Neon Invest is subject as a Swiss investment platform, whereas you don’t have to pay it when you use Interactive Brokers.

Also, Neon Invest does not offer Vanguard’s fantastic global diversified ETF: the VT ETF.

Nevertheless, neon invest is a reassuring solution (because people are already familiar with the neon mobile application environment) that can be a very good springboard for daring to take the plunge and begin serenely with stock market investing.

But above 10k-50kCHF, I strongly recommend you switch to an optimal online broker such as Interactive Brokers.

Is Yuh a good choice for investing in the stock market?

Yuh is the banking and investment solution created by the alliance of PostFinance and Swissquote (and wholly owned by Swissquote since July 2025). Their brokerage fees of 0.50% may seem interesting for small investors (<CHF 1'000 per transaction). What worsens it is that there are currency conversion fees of 0.95%.

Finally, what makes me reject Yuh for investing in the stock market is its list of ETFs, which is far too small. Moreover, this list does not contain any US-based global ETFs (such as the Vanguard VT ETF) or my favorite Swiss ETF (the UBS SMIM ETF).

In conclusion, Yuh is not one of the Swiss online brokers of choice for a Swiss Mustachian investor (but on the other hand, it’s a very good secondary Swiss bank account).

DEGIRO or Interactive Brokers?

I have received this question so many times that I have created a dedicated article. You will find the answer by following this link.

Does Interactive Brokers offer margin loans (Lombard loan)?

Yes, Interactive Brokers (IBKR) offers margin loans on unbeatable terms.

You can see the Interactive Brokers interest rates for the different currencies here.

I use their Lombard loan myself, sparingly. You’ll find more info here: “How to open a margin account on IBKR (Interactive Brokers) in 2026”.

Does Saxo Bank offer margin loans (Lombard loan)?

Yes, since July 2025, Saxo offers margin loans in Switzerland in various currencies.

Their terms are quite attractive too; you’ll find all the details of the Saxo Bank Lombard loan here.

What do you think of VZ for investing?

VZ offers a “Save and invest with ETFs” solution with low fees compared to the big Swiss banks. They charge a flat annual fee of 0.55% on the total amount of your portfolio (note: these 0.55% exclude ETF TER fees, which are additional). This is certainly cheaper than a traditional bank, but it’s far too expensive compared to a broker like Interactive Brokers.

For example, if you have a stock market portfolio of CHF 70'000, you’ll pay a fee of (even if you don’t make any transactions):

- CHF 350 with VZ

- CHF 0 with IBKR

So over the long term, and especially with a stock portfolio that’s set to grow, VZ is less attractive than Interactive Brokers or DEGIRO.

What is your opinion on Selma.io?

I see the Swiss broker Selma.io as the launching pad for a very new investor who prefers an automated trading solution, rather than investing on your own.

The only good thing about Selma.io is its autopilot function, but then it quickly becomes limiting for a Mustachian investor because:

- The fees are too high (~0.9%) compared to other brokers like Interactive Brokers or DEGIRO

- You can’t choose the ETFs you want, because Selma.io creates an investment strategy for you in an automated way (even if it’s tailor-made, you can’t choose which ETFs to invest in)

Is TrueWealth a cheap trading platform?

TrueWealth is a robo-advisor rather than a trading platform where you can buy and sell your ETFs and other stocks. This means, like Selma.io, it’s a good starting point for a beginner investor.

But after you pass this beginner’s phase, TrueWealth is still too expensive compared to the competition. TrueWealth has a total fee of 0.65% (= 0.5% global fee including transaction fees + 0.15% TER fee and of the ETFs that they use).

Furthermore, their robo-advisor solution does not allow you to select exactly the ETFs you want.

Is Inyova a suitable solution to invest in the stock market?

Inyova is a Swiss broker specializing in stock and ETF trades, focusing on investments in high-impact companies. From a purely theoretical point of view, I would not recommend them for a beginner investor due to a lack of diversification and high fees.

Indeed, Inyova has a universe of 300 companies, and depending on your impact themes, Inyova creates an investment portfolio of only about 30-40 companies.

Inyova’s fees are high: between 0.6 and 1.2% per year. However, if I were to choose Inyova, I would be more OK to pay these fees, as Inyova actually does something in return, vs. traditional banks and brokerage firms that earn money for Porsches for their bankers via their useless fees and mutual funds.

Finally, I recommend that you read my article about impact investing and my opinion on who really has the power to change our world.

Do I have access to Trade Republic as a Swiss resident?

I often hear great things about this German trading platform, Trade Republic. Unfortunately, currently, you can’t create a trading account on Trade Republic as a Swiss resident.

If this changes, I will update this comparison of trading platforms.

What about Comdirect (Commerzbank) as a broker for a Swiss trader?

Comdirect is a German trading platform (so only in German…). It is accessible to Swiss residents. But its fees are too high compared to the competition with 7.90€ + 0.25% transaction fee, as well as a monthly inactivity fee of 5.85€ (and you need at least 2 transactions!)

All this is enough to not include this broker in my comparison above. And we haven’t even touched on their variable rate exchange fees ;)

What is your opinion on Lynx?

Lynx is a German-based online broker, but active and available for Swiss residents. Their transaction fees are too high for a Mustachian investor, therefore, this broker is not included.

We are talking about a small percentage of 0.15%, but they charge a minimum of CHF 15 for Swiss ETFs and 5 USD for American ETFs.

Any opinion on Maxblue (Deutsche Bank) for a Swiss investor?

The trading platform Maxblue (Deutsche Bank) is way too expensive for a Swiss “buy and hold” investor. Their transaction fees are respectively 29€ + 0.25% for Swiss ETFs and 15€ + 0.25% for American ETFs.

No, thank you :)

Can I open a trading account with the US broker Fidelity?

No, unfortunately, an investor residing in Switzerland cannot open a trading account with the American online broker Fidelity.

Can I open a trading account with the US broker TD Ameritrade?

Yes, an investor living in Switzerland can open a trading account with the American trading platform TD Ameritrade. But you should know that Charles Schwab has announced the acquisition of TD Ameritrade. And this merger will end in 2023.

So, if you are looking for an American alternative to Interactive Brokers, I advise you to go directly to Charles Schwab.

Can I open a trading account with the US broker E-Trade?

No, an investor residing in Switzerland cannot currently open a securities account with the American online broker E-Trade.

Can I open a trading account with the US broker Merrill Edge?

Also negative. An investor living in Switzerland does not have access to the American online broker Merrill Edge.

(*) This symbol indicates where my article contains affiliate links. If you click one or more of them, you won’t see any difference compared to a standard link, but the blog will earn an affiliate commission. Thank you for this. As usual, I only write about and review things that I use in my daily life or that I trust.

(**) Investing involves risk of loss.

Photo credits Pexels Mélanie (Tim Douglas)